DEEP RESEARCH · Iljin Power (094820)

Iljin Power (094820) Deep Dive: Strategic Pivot in the Era of Energy Security and the SMR Super-Cycle

SMR & fusion growth pillars built on a power-plant maintenance cash cow — the re-rating thesis for a hybrid model

0. Bottom line first

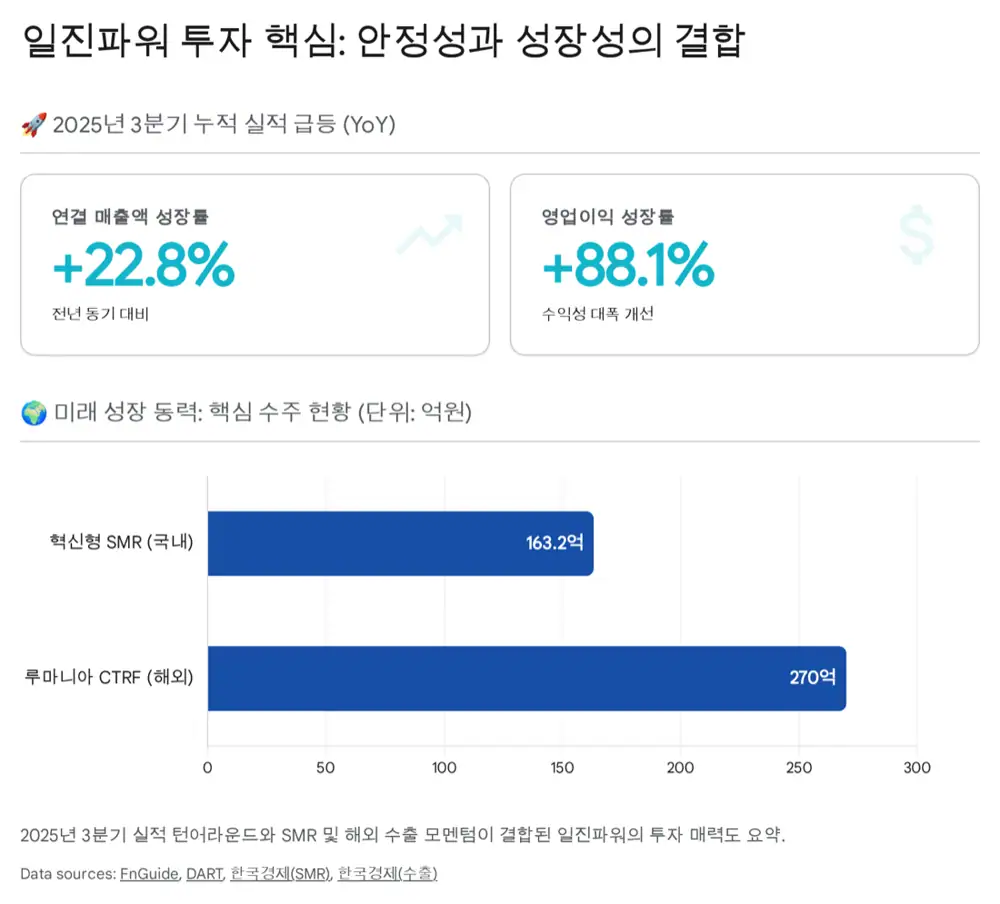

Iljin Power is a hybrid company that stacks SMR, fusion and nuclear equipment exports as growth pillars on top of a power-plant routine-maintenance cash cow. 3Q25 YTD revenue jumped to KRW 193.1B (+22.8% YoY) and operating profit to KRW 10.3B (+88.1% YoY) — a structural step-up. With Korea's 11th Electricity Plan, the Cernavoda contract and the i-SMR integrated-effects test facility win all materializing at once, there is ample room to re-rate from a plain maintenance multiple (~10x PER) to an SMR-owner multiple (15–20x).

Official fact: Market cap ~KRW 168.4B, controlling-shareholder stake 36.79%, FY2024 consolidated debt-to-equity 97.24%, parent-only 33.32%.

Interpretation: Far healthier than the typical heavy-equipment peer — Iljin retains both the firepower to fund new businesses and the cash to keep paying dividends, a rare combination.

1. Company overview and the three core pillars

Official fact: Founded as Iljin Precision in 1990, in-house R&D institute set up in 1998. In 2002 the company was selected as a designated private operator when Korea opened the power-plant maintenance market to competition. In 2014 it took an equity stake in newly founded Smart Power Inc.

The business has evolved beyond simple equipment fabrication into three core pillars spanning the full energy value chain.

Power-plant routine maintenance + OH

Real-time inspection during operation + scheduled overhauls. Covers nuclear, thermal and LNG combined-cycle. Oligopolistic alongside KEPCO KPS and Kumhwa PSC. ~52% of revenue.

Process equipment & EPC

Heat exchangers, pressure vessels, reactors — design and fabrication. Expanding into hydrogen extractors and storage vessels. Onsan National Industrial Complex (Ulsan) plant optimized for large-scale equipment.

New nuclear (R&D)

20+ years of cooperation with KAERI. Best-in-class SMR and tritium-handling capabilities among Korea's private players. An engineering/IP play, not just construction.

2. Macro: energy security and the nuclear renaissance

Post-Russia-Ukraine, global energy markets shifted from "economics-first" to "security-first". At the same time, net-zero became mandatory rather than optional. Nuclear is re-emerging as the only realistic answer to both at once.

2.1 The 11th Electricity Plan — Iljin Power's opportunity

Official fact: Korea's 11th Basic Plan for Electricity projects peak demand of 129.3 GW by 2038, lifts the nuclear share target from 31.8% (2030) to 35.6% (2038), and calls for 10.6 GW of new capacity — including three large reactors (4.2 GW) and one SMR (0.7 GW).

Interpretation: As critical as new builds is continued operation of aging reactors — maintenance work scales exponentially as plants age, which structurally underwrites Iljin Power's top line.

2.2 Global SMR market take-off

Official fact: The World Economic Forum projects the SMR market to grow at a ~22% CAGR through 2040. Korea's 11th Plan targets commercial SMR operation around 2035.

SMRs claim ~1,000x higher safety margins than large reactors, and modular factory fabrication with onsite assembly slashes both build time and cost. They are emerging as the core energy source for distributed generation and net-zero industrial clusters.

3. Segment deep dive

3.1 Power-plant routine maintenance — rediscovering the cash cow

Official fact: Domestically, the state-owned KEPCO KPS holds ~50–60% of the maintenance market, with the remainder oligopolized by six designated private operators including Iljin Power, Kumhwa PSC and Korea Plant Service. Disclosed on 2025-07-01: 'Hanbit Units 3 & 4 mechanical/electrical maintenance' contract worth KRW 19.98B (through June 2027).

Interpretation: The Hanbit deal matters because it was contracted directly from KHNP rather than as a subcontract — a recognition of Iljin's standalone technical capability. With Hyundai E&C's consortium taking the main works for Shin-Hanul Units 3 & 4, and Iljin's long-standing partnership with Hyundai E&C, the company is well placed for both commissioning maintenance and main-equipment routine maintenance follow-on wins.

3.2 New nuclear growth — the heart of the re-rating

3.2.1 Innovative SMR (i-SMR): from R&D partner to fabrication partner

Official fact: On 2025-03-07, Iljin won a KRW 16.32B contract from KAERI to fabricate and install the 'i-SMR integrated-effects test facility'.

The integrated-effects test facility is the must-have rig that proves the i-SMR design works safely under real high-temperature, high-pressure conditions — the last gate before commercialization. Without it, no licensing from the Nuclear Safety and Security Commission. In effect, Iljin Power is the "midwife" for the i-SMR's birth.

Interpretation: This proves Iljin is not a blueprint-follower but an engineering partner that validates and optimizes designs with the research institute — locking in a preferred position in the main-equipment and balance-of-plant (BOP) supply chain when i-SMR goes into mass production and export.

3.2.2 Fusion (ITER) & tritium — Korea's unique private-sector player

Official fact: Iljin Power is the only Korean firm to have commercialized a tritium storage & delivery system (SDS), via tech transfer from KAERI. In August 2025, together with Doosan Enerbility, Iljin signed a KRW 23.8B contract to supply equipment for the Tritium Removal Facility (TRF) at Romania's Cernavoda nuclear plant.

Interpretation: Lab-stage technology has now crossed into actual commercial-reactor equipment exports. Combined with life-extension projects for Europe's aging CANDU/heavy-water reactors, this opens further export pipeline.

3.2.3 Hydrogen — laying the groundwork

Hydrogen is currently ~4% of revenue — small. But when SMR high-temperature steam starts producing clean (pink) hydrogen, Iljin's combined nuclear + hydrogen capability becomes a real synergy.

4. Financials: growth proven in numbers

4.1 The 2025 quantum jump

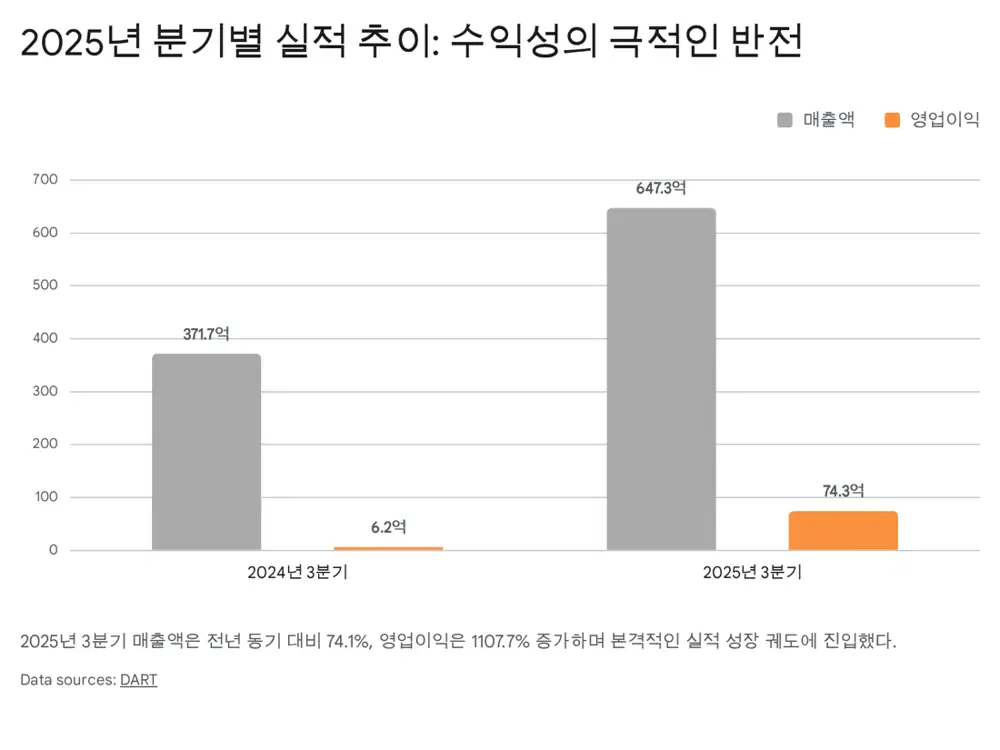

| Metric | 3Q25 YTD | YoY | 3Q25 standalone | YoY |

|---|---|---|---|---|

| Revenue | KRW 193.1B | +22.8% | KRW 64.73B | +74.1% |

| Operating profit | KRW 10.3B | +88.1% | KRW 7.43B | +1,107.7% |

Interpretation: Operating-profit growth far outstripping revenue growth — classic operating leverage. The mix shift away from low-margin simple construction toward higher-margin nuclear equipment and engineering is the main driver — a structural product-mix upgrade. With prior-year 3Q operating profit at just KRW 0.62B, this is more than a base effect — it's a step-change in earnings power.

4.2 Balance sheet — near-net-cash discipline

Official fact: FY2024 consolidated debt-to-equity 97.24%, parent-only 33.32%. Ample cash plus stable operating cash flow supports both new investment and a consistent dividend.

5. Valuation and peer comparison

5.1 Peer group

| Item | Iljin Power (094820) | KEPCO KPS (051600) | Kumhwa PSC (036190) |

|---|---|---|---|

| Core business | Nuclear/thermal maintenance, SMR, fusion | Power-facility maintenance (SOE) | Thermal/nuclear maintenance |

| Market cap | ~KRW 168.4B | ~KRW 1.8T | ~KRW 170B |

| PER (2025E) | 10.5x (est.) | 18.0x | 6.5x |

| PBR | 0.9x | 1.5x | 0.5x |

| Investment angle | Proprietary SMR/fusion tech, high growth | Stability, dominant market position | Cheap value, high dividend |

| Risk | High policy sensitivity | Stagnant growth | No new growth engine |

Source: company disclosures and brokerage reports, reconstructed.

- vs. KEPCO KPS: Dominant share but as a state enterprise, growth is muted and valuation already full. Iljin offers private-sector agility and new-business optionality — better growth potential.

- vs. Kumhwa PSC: Extremely cheap, but lacks SMR/fusion growth story. Iljin's valuation premium comes from this "technology moat".

5.2 Re-rating logic

Interpretation: ~10x PER is the multiple of a plain construction/maintenance player. But Iljin's mix is shifting to SMR R&D and nuclear equipment exports — applying a maintenance multiple is unfair. With loss-making global SMR peers (NuScale, Oklo) commanding premium valuations, a profitable SMR-capable Iljin has clear room to re-rate toward a Target PER of 15–20x.

5.3 Strategy

- Tactical (short term): Play the 3Q earnings surprise + 11th Plan confirmation momentum. Scaled buying below KRW 11,000 provides margin of safety.

- Strategic (long term): From 2026 onward, i-SMR development milestones become visible, Cernavoda revenue starts hitting the P&L, and Shin-Hanul 3 & 4 follow-on orders are likely. Buy-and-hold with add-on purchases on technical milestones. Initial price target: KRW 25,000 (previous high).

6. Risks

- Policy volatility: A change of government or sharp policy shift could hit the backlog. That said, AI-driven power demand and net-zero are global — the importance of nuclear is unlikely to evaporate.

- Raw-material costs: Special steel, nickel, titanium are heavily used. Spikes squeeze margins — watch for escalation clauses and hedging.

- SMR commercialization delay: i-SMR is still in development. Technical or regulatory delays could turn hype into disappointment. Track KAERI project milestones and global SMR licensing trends.

- Talent supply: The nuclear renaissance is sucking up experienced engineers. Retaining and hiring core nuclear talent will decide Iljin's long-term competitiveness.

7. Closing

Iljin Power has built a "growth" pillar on top of a "stability" foundation. The power-plant maintenance cash cow lets it withstand any downturn; SMR and fusion technology give it explosive growth potential. "From a company that fixed old power plants, to one that creates the energy of the future." Iljin Power's transformation is in motion.

Disclaimer: This report is based on public information and reasonable inference. All legal responsibility for investment outcomes rests with the investor. Past performance does not guarantee future results.

Sources

- Original Naver blog post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224116248540

- Iljin Power Snapshot — FnGuide: https://comp.fnguide.com/SVO2/ASP/SVD_Main.asp?gicode=A094820

- Iljin–Doosan Enerbility KRW 23.8B supply deal — Digital Today: https://www.digitaltoday.co.kr/aigongsi/2042/iljin-power-doosan-enerbility-supply-contract

- 11th Electricity Plan summary — KDI: https://eiec.kdi.re.kr/policy/callDownload.do?num=263534&filenum=2&dtime=20250225075221

- 11th Plan, aging reactor extensions, 4 new reactors — Nowon Carbon-Neutral Center: https://nwcarbonzero.tistory.com/22

- 2014 National Assembly audit on the maintenance market — People Power Party: https://www.peoplepowerparty.kr/news/lawmaker_inspection_view/76825?page=63&

- Iljin Power company analysis — YouTube: https://www.youtube.com/watch?v=U8A4UFfIhxI

- Iljin Power annual report — KRX disclosure: https://kind.krx.co.kr/common/disclsviewer.do?method=search&acptno=20250320001345&docno=&viewerhost=&

- Iljin Power / Iljin Energy nuclear business: https://ijeng.com/pwkor/page/nuclear2.html

- Iljin Power dividend history — Investing.com: https://kr.investing.com/equities/iljin-power-co-ltd-dividends

- MOTIE 11th Plan working draft — CTIS: https://ctis.re.kr/board.es?mid=a10101010000&bid=0001&tag=&act=view&list_no=43491

- 11th Plan main contents — KPX: https://www.kpx.or.kr/boardDownload.es?bid=0042&list_no=73380OOO202409121101256453&seq=3

- 2034 first i-SMR operation outlook — Today Energy: https://www.todayenergy.kr/news/articleView.html?idxno=288257

- Iljin Power Hanbit 3 & 4 maintenance KRW 19.98B — Hankyung: https://www.hankyung.com/article/202507011582L

- Hyundai E&C – KHNP Shin-Hanul 3 & 4 signing: https://www.hyundaimotorgroup.com/ko/news/CONT0000000000128283

- Shin-Hanul 3 & 4 KRW 3.1T contract — Goover: https://seo.goover.ai/report/202507/go-public-report-ko-68e8f921-57c5-4d46-b5f0-a8efcb2e58d4-0-0.html

- Iljin Power 2025 order backlog — Sankun: https://www.sankun.com/company-info/IBg2oxwfTI8CVhX2vwsLWA%3D%3D

- i-SMR integrated-effects test facility KRW 16.32B — Hankyung: https://www.hankyung.com/article/202503078893L

- Iljin Power Sep 2025 confirmed results — Toss Securities: https://www.tossinvest.com/stocks/A094820/news

- Kumhwa PSC investment analysis — Judal: https://www.judal.co.kr/?view=stockAI&shareToken=uUDvXbnc9ifmrVsu

- Iljin Power investment analysis — Judal: https://www.judal.co.kr/?view=stockAI&shareToken=Mr4SN1ph58R37Pl5