DEEP RESEARCH · TAEYOUNG E&C/WORKOUT

Taeyoung E&C: Survival Is Not Yet Recovery

A review of the workout, Ecobit sale, and 2026 construction-cycle setup

0. Bottom line first

Taeyoung E&C has passed the survival stage through trading resumption and the end of capital impairment. But with operating losses, a 654% debt ratio, and a weakened cash engine after Ecobit, I still view it as a restructuring company rather than a recovered company.

Official fact: The source highlights full capital impairment of negative KRW 561.7 billion at end-2023, first-half 2025 assets of KRW 2.7556 trillion and equity of KRW 404.8 billion, and trading resumption on October 31, 2025.

Interpretation: Trading resumption opens the possibility of rehabilitation, but it does not prove restored operating profit. The key variables are cost ratio and operating cash flow, not reported net profit.

1. Workout and trading resumption

Taeyoung E&C entered workout in late 2023 as real-estate PF liquidity froze. PF impairments and additional losses pushed it into full capital impairment. It then went through a 100:1 capital reduction for major shareholders, differential reductions for other shareholders, unsecured creditor debt-to-equity conversion, and perpetual bond issuance by TY Holdings.

Impairment resolved

Equity recovered to KRW 404.8 billion in first-half 2025.

Trading resumed

The Korea Exchange allowed trading to resume from October 31, 2025.

Speculative volatility

The source cites a December 2025 preferred-share price of KRW 11,190, up 348% from a three-year low, an investment-warning designation, and PBR of 6.29x.

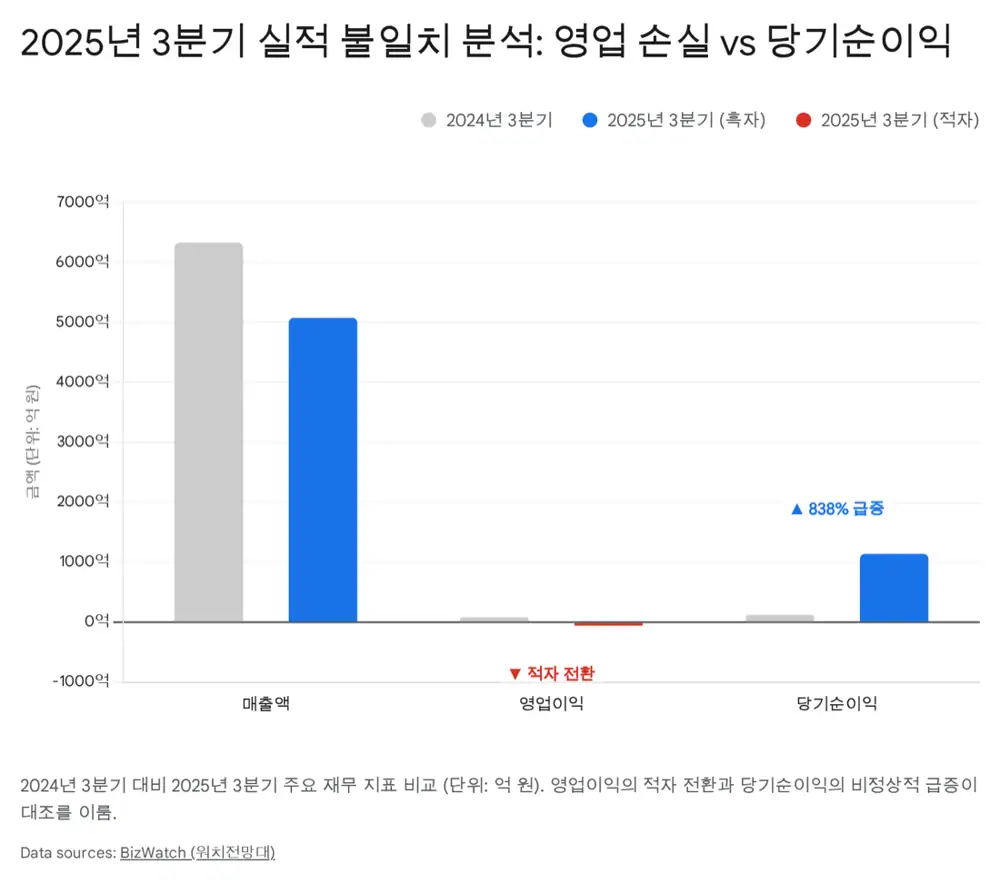

2. 3Q25: optics versus substance

| Metric | 3Q25 | Comparison | Meaning |

|---|---|---|---|

| Revenue | KRW 507.8 billion | Down 19.8% from KRW 633.0 billion | New private development halted and major sites completed |

| Operating profit | -KRW 5.8 billion | From KRW 8.6 billion profit to loss | Core operating weakness |

| Cost-to-sales ratio | 95.9% | +5.5 percentage points | KRW 96 of cost for KRW 100 of construction |

| Net income | KRW 113.9 billion | +838.3% from KRW 12.1 billion | Mainly accounting events such as debt forgiveness gains |

| Debt ratio | 654% | Down 264 percentage points from 2Q | Improved but still more than 3x a 200% industry-normal level |

Interpretation: The 838.3% net-profit surge largely reflects debt reduction booked as accounting income. The more important indicators are falling sales, operating loss, a 95.9% cost ratio, and KRW 33.7 billion of inventory-change-related costs.

3. Ecobit and the paradox of asset sales

The source treats the sale of environmental subsidiary Ecobit as the most painful part of Taeyoung’s self-rescue plan. The sale was needed for creditors, but much of the proceeds went to debt repayment, leaving a thinner liquidity buffer inside Taeyoung E&C.

Official fact: The references include reports that Taeyoung retained only about KRW 100 billion after selling Ecobit. The source connects that outcome to the loss of a growth engine and weaker internal cash generation.

4. Remaining contingent liabilities

| Risk | Description | Note |

|---|---|---|

| PF contingent liabilities | Funding support and conditional debt-assumption agreements for SOC and private developments | See note 39 |

| Completion guarantees | Completion obligations for major PF sites and debt assumption if unmet | Core workout monitoring item |

| Litigation liabilities | Defect repair claims, damages, and pending suits | See note 40 and XI-2 |

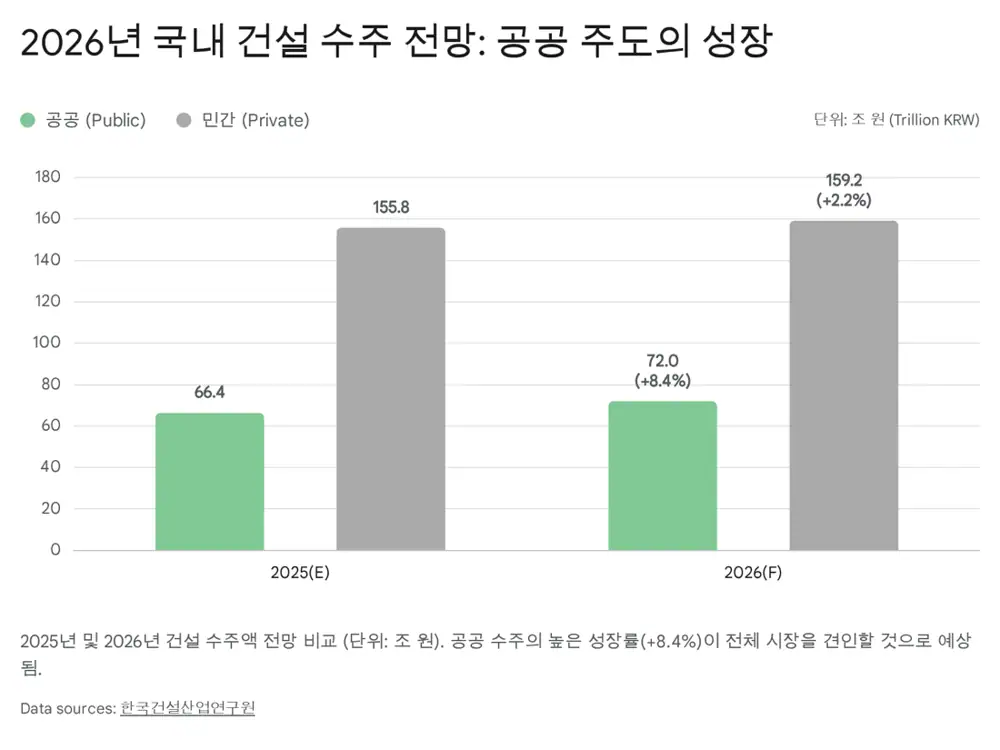

5. 2026 construction market: public and private decouple

The source expects 2026 domestic construction orders to rise about 4.0% from 2025 to KRW 231 trillion, but the public and private markets look very different.

+8.4% forecast

SOC budget is expected to rise 7.9% YoY to KRW 27.5 trillion, with GTX-B/C, aging infrastructure, and AI data-center power grids as opportunities.

+2.2% forecast

High rates, unsold regional housing, and stress-DSR rules pressure housing demand. The rise looks mostly base effect.

Sticky downside

Cement, aggregate, labor, and safety-management costs do not fall easily, so even public work may carry low margins.

6. My conclusion

Taeyoung has survived, but I would not call it recovered until operating profit turns positive, cost ratios stabilize, and public orders show acceptable margins. Public order growth is a real opportunity, but low-margin backlog can become another burden. For investors, operating data matters more than rehabilitation optimism.

Sources

- Original post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224115784018

- Reference 1: https://m.newsprime.co.kr/section_view.html?no=660752

- Reference 2: https://www.judal.co.kr/?view=stockAI&shareToken=lUqymWiVhPPEW77i

- Reference 3: http://news.bizwatch.co.kr/article/real_estate/2025/11/21/0030

- Reference 4: https://www.businesspost.co.kr/BP?command=article_view&num=420277

- Reference 5: https://seo.goover.ai/report/202511/go-public-report-ko-ccb7d509-9ec3-4b7d-ac21-2e3d992d4495-0-0.html

- Reference 6: https://v.daum.net/v/trXpb7rRvM

- Reference 7: https://www.hankyung.com/amp/202412134053r

- Reference 8: https://v.daum.net/v/G9ywylxpSV

- Reference 9: https://news.dealsitetv.com/articles/129328

- Reference 10: https://www.si-sec.com/board/newsDetail.do?content=4000190&news_gb=10&news_dt=20240926&news_seq_no=2024092619180100833

- Reference 11: https://at1.co.kr/news.asp?ID=2025-10-18/vfwfcd.html

- Reference 12: https://www.cerik.re.kr/uploads/report/3020/%EA%B1%B4%EC%84%A4%EB%8F%99%ED%96%A5%EB%B8%8C%EB%A6%AC%ED%95%91%201030%ED%98%B8.pdf

- Reference 13: https://www.bondweb.co.kr/_research/downloadPage.asp?number=877078&gn=1

- Reference 14: https://www.ceomagazine.co.kr/news/articleView.html?idxno=34514

- Reference 15: http://www.ikld.kr/news/articleView.html?idxno=324820

- Reference 16: https://www.sankun.com/blog/detail/1287_2026%EB%85%84__%EC%97%85%ED%99%A9_%EB%B0%98%EC%A0%84%EC%9D%98_%ED%95%B4%EA%B0%80_%EB%90%A0%EA%B9%8C____%EA%B1%B4%EC%84%A4_%EC%9E%90%EC%9E%AC_%EB%B6%80%EB%8F%99%EC%82%B0_%EA%B2%BD%EA%B8%B0_%EC%A0%84%EB%A7%9D_%EB%B0%9C%ED%91%9C

- Reference 17: https://marketin.edaily.co.kr/News/ReadE?newsId=03686726642395568

- Reference 18: https://www.g-enews.com/article/General-News/2025/12/2025120808200841335e857d010_1