DEEP RESEARCH · NEXEN/MOBILITY HOLDING COMPANY

Nexen: Tire Turnaround and Asset-Value Re-Rating

Re-reading a low-PBR holding company through tires, logistics, rubber, and real estate

0. Bottom line first

My read is that Nexen has moved past the 2022 freight and raw-material shock, but the market still mainly prices the holding-company discount and thin liquidity. Nexen Tire’s earnings recovery, the parent’s rubber and logistics businesses, and real-estate assets can all matter in a re-rating.

Official fact: The source gives 2024 consolidated revenue of KRW 3.2143 trillion, operating profit of KRW 209.6 billion, and operating margin of 6.5%. It also states a December 9, 2025 share price of KRW 6,310, market cap of about KRW 337.9 billion, net asset value of about KRW 2.5 trillion, and PBR around 0.2x.

Interpretation: This is less a high-growth stock than a value stock whose price looks depressed relative to assets and earnings power. The caveat is that tire demand, raw materials, freight rates, and FX all move consolidated earnings.

1. Industry setup: EVs, inputs, freight, FX

The source frames the global tire market as growing from about USD 147.4 billion in 2025 to USD 173.9 billion in 2030, a 3.4% CAGR. Replacement tires account for more than about 63% of the market and are relatively less cyclical.

Higher-value tires

EVs are 20-30% heavier than ICE vehicles and need tires that handle torque, wear, and noise, supporting higher unit prices and replacement demand.

Rubber volatility

Natural and synthetic rubber are described as more than about 30% of tire manufacturing cost. Oil and butadiene are 2025 cost variables.

SCFI stabilization

The 2021-2022 SCFI spike above 5,000 points drove losses, while 2025 vessel deliveries may limit freight-rate pressure.

Interpretation: EV and high-inch tires support ASP, while freight normalization works in the opposite direction of the 2022 loss shock. A weaker won helps translated export revenue but also raises imported input costs.

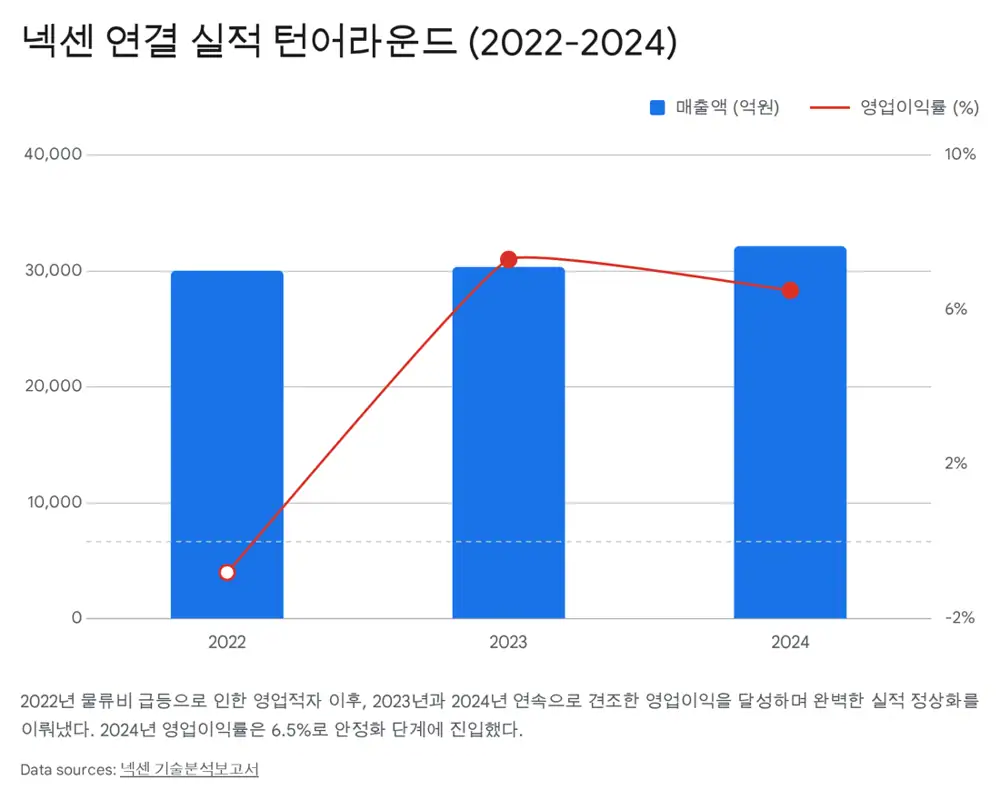

2. 2024 results: the turnaround is visible

| Metric | Source figure | How to read it |

|---|---|---|

| Revenue | KRW 3.2143 trillion | 5.9% YoY growth |

| Operating profit | KRW 209.6 billion | 6.5% operating margin |

| Product mix | Higher share of 18-inch-plus tires | ASP and margin support |

| Czech plant | Utilization stabilized | Expanded European supply |

The 2022 operating loss was a special period of freight disruption and raw-material inflation. After returning to profit in 2023 and delivering a strong 2024 turnaround, I care most about whether normalized earnings power is now durable.

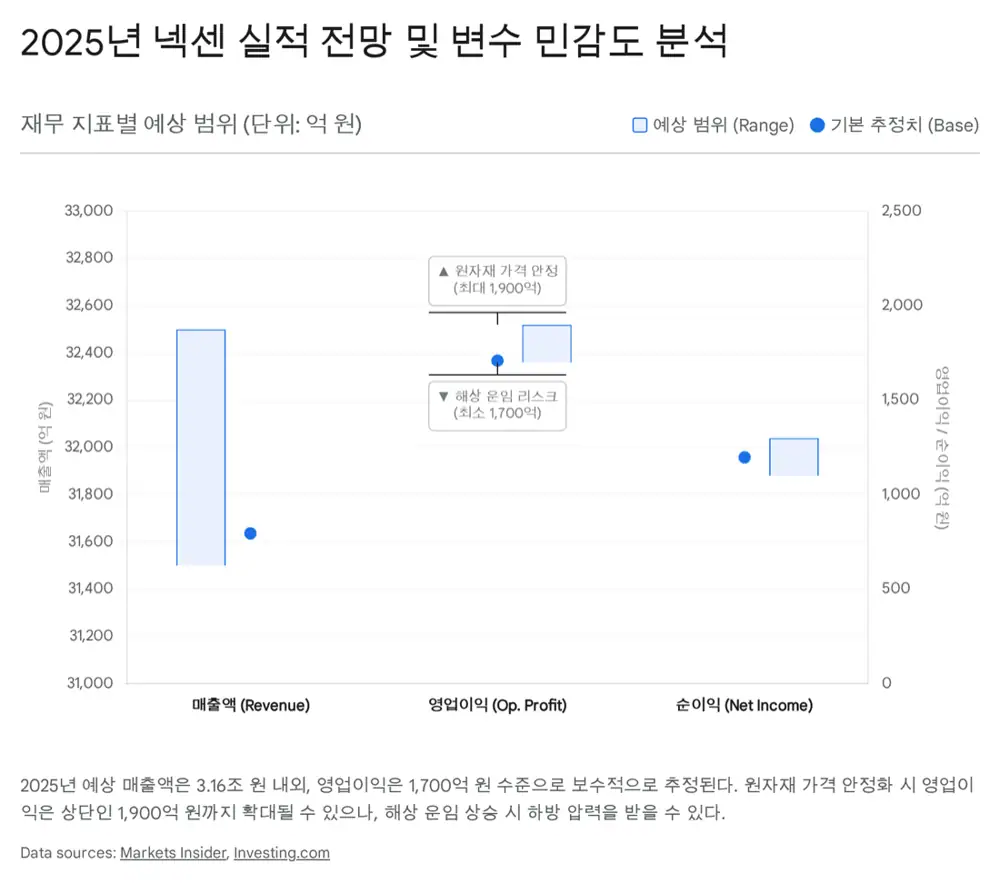

3. 2025 outlook and scenarios

Official fact: The source gives a 2025 base-case revenue range of KRW 3.35-3.45 trillion and operating profit of KRW 210-230 billion. In the bull case, EV tire mix exceeds 20%.

Bull

- Global auto sales and replacement tire demand recover together.

- EV and high-inch tire mix rises quickly, improving ASP.

- Freight and raw materials stabilize, expanding operating leverage.

Base

- Revenue grows 5-7% and operating margin stays around 6.5%.

- Czech plant stability and North American demand support sales.

Bear

- Raw materials, freight, and FX move against the company while global demand weakens.

- The holding-company discount and thin liquidity persist.

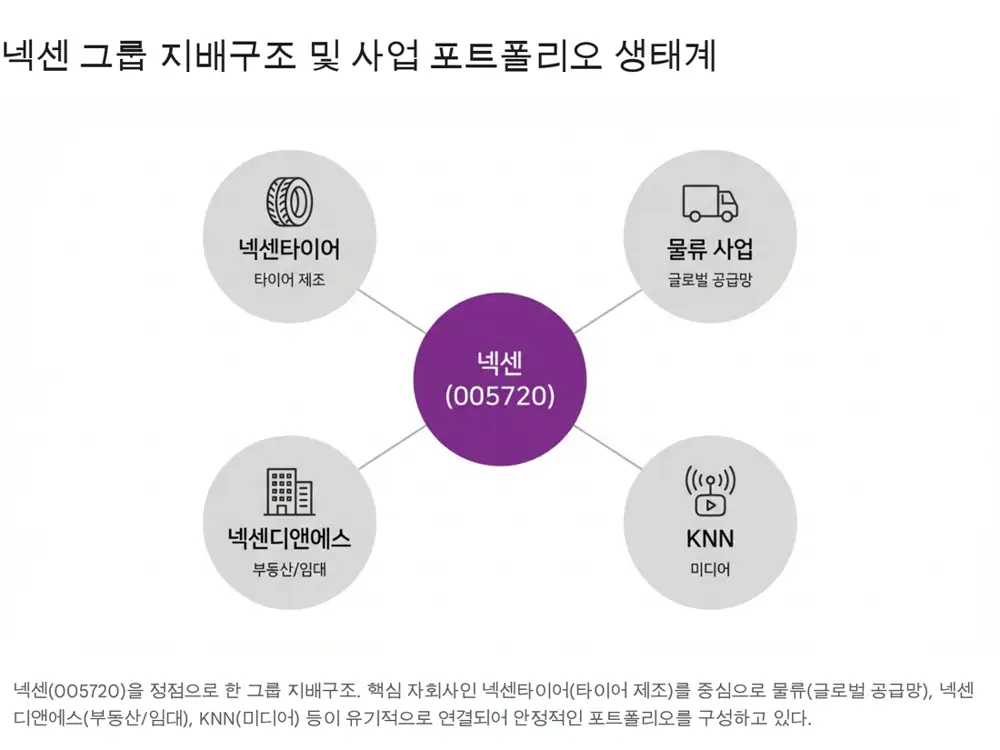

4. Business segments: rediscovering the portfolio

Four global bases

Korea, China, the U.S., and Europe give the group a strategic hedge against FX and tariff risk.

Tubes and solid tires

Industrial-vehicle niche products are smaller but less competitive and produce steady profit.

From captive to 3PL

Nexen Logistics is expanding from group freight volume toward third-party logistics customers.

Real estate, leisure, CVC

Nexen D&S leasing/development, golf operations, and Next Century Ventures add hidden asset value and growth options.

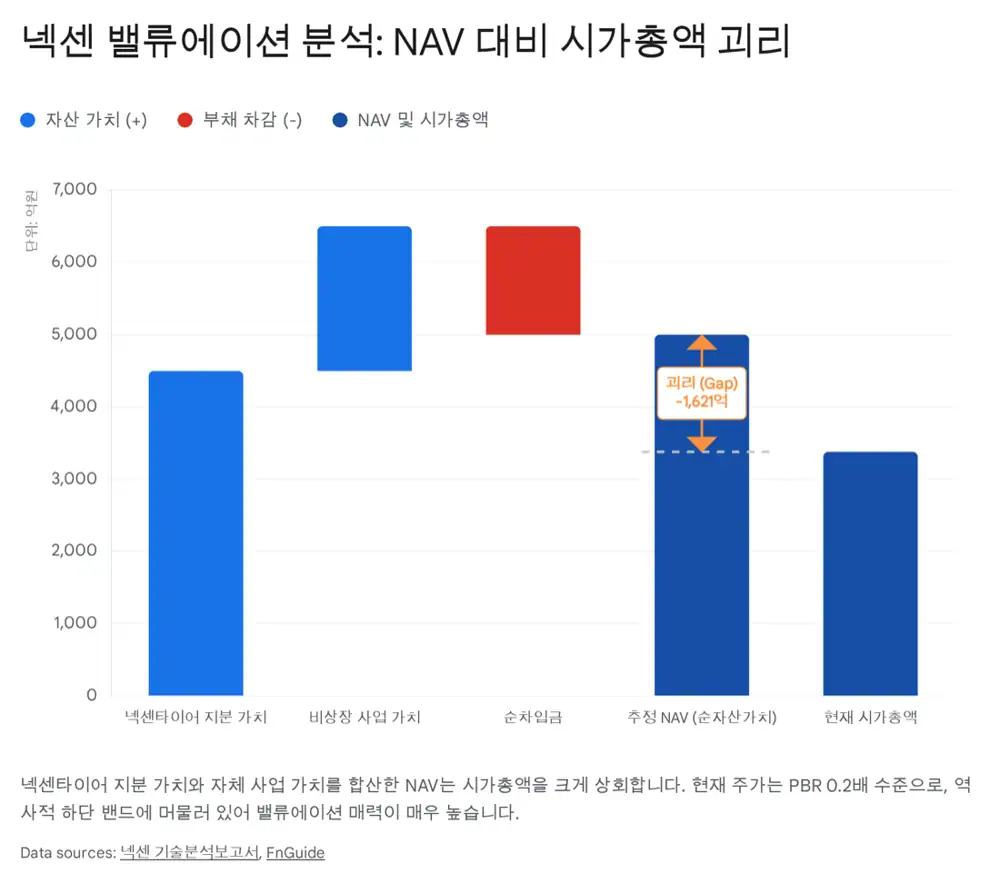

5. Valuation and my conclusion

The source values the Nexen Tire stake by assuming a KRW 800 billion market cap and Nexen’s roughly 44% ownership, giving about KRW 350 billion of stake value, or about KRW 175 billion after a 50% holding-company discount. It values the parent’s operating businesses at KRW 160-240 billion using KRW 20-30 billion of estimated standalone operating profit and an 8x target multiple, and conservatively counts 50% of more than KRW 500 billion of real estate and investment assets.

Interpretation: The source’s KRW 9,000-11,000 target range and KRW 8,517 consensus fair value come from the view that the current price does not reflect net assets or earnings power. I would treat the source’s strong-buy language as the author’s view, and monitor freight, raw materials, EV mix, and shareholder returns before acting.

Sources

- Original post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224114970434

- Reference 1: https://www.thecommoditiesnews.com/news/articleView.html?idxno=7548

- Reference 2: https://xml.newstomato.com/ReadNews.aspx?no=1234850

- Reference 3: https://markets.businessinsider.com/stocks/nexen_tire-stock

- Reference 4: https://comp.fnguide.com/SVO2/asp/SVD_Consensus.asp?pGB=1&gicode=A002350&cID=&MenuYn=Y&ReportGB=&NewMenuID=108&stkGb=701

- Reference 5: https://www.thenewsmarket.com/news/nexen-tire-strengthens-global-market-penetration-with-locally-customized-products/s/c9bf04a9-7a41-43e7-acaa-40326f7b28a5