DEEP RESEARCH · ST PHARM/xRNA CDMO

ST Pharm: Global xRNA CDMO Transition and 2026 Growth Momentum

A review of oligonucleotide CDMO demand, the second oligo plant, SmartCap®, and proprietary pipeline optionality.

0. Bottom line first

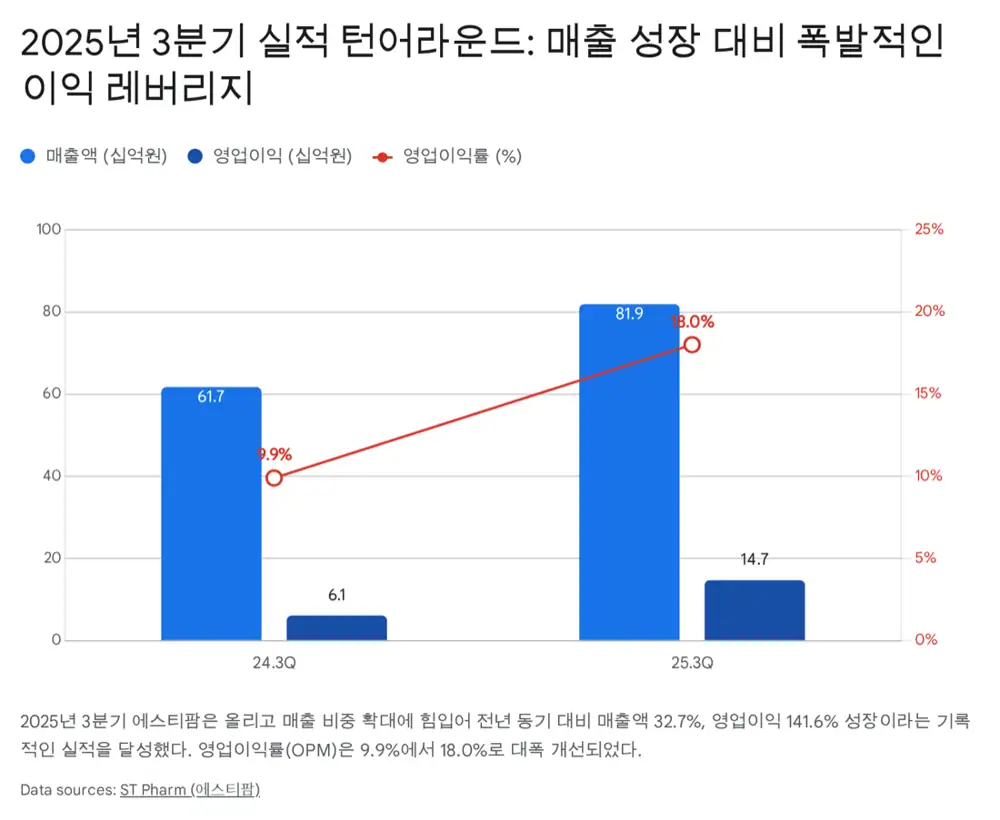

I view ST Pharm not as a simple API manufacturer, but as a CDMO exposed to both oligonucleotide API supply shortage and xRNA platform expansion. Q3 2025 revenue of KRW 81.9B and operating profit of KRW 14.7B confirmed the turnaround; in 2026, full operation of the second oligo plant and commercial-volume growth become the key variables.

KRW 81.9B revenue

Revenue rose 32.7% from KRW 61.7B a year earlier, while operating profit jumped 141.6% to KRW 14.7B.

KRW 68.6B oligo revenue

Oligo revenue grew 92.9% from KRW 35.6B and represented about 83.8% of total revenue.

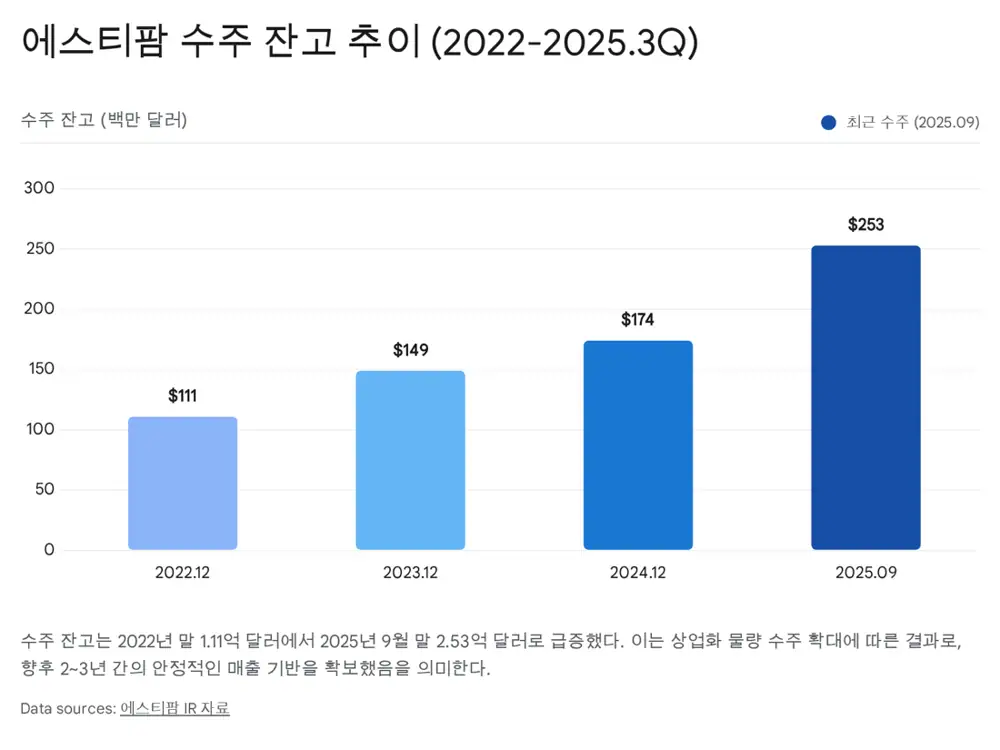

USD 253M backlog

Backlog more than doubled from USD 111M at the end of 2022, and the company had 43 projects as of Q3 2025.

1. Industry transition and ST Pharm’s position

The biopharma industry is moving from small molecules to antibodies and now to nucleic-acid therapeutics that use DNA and RNA to block or modulate production of disease-causing proteins. This is not merely a modality expansion; it changes treatment from symptom relief toward root-cause intervention.

Official fact: The source identifies oligonucleotides and mRNA as the core pillars of next-generation therapeutics. Oligonucleotide drugs are expanding from rare diseases into chronic diseases such as hyperlipidemia, cardiovascular disease, and hepatitis B, with patient populations in the tens of millions; only a very small number of companies have high-quality cGMP-grade production facilities.

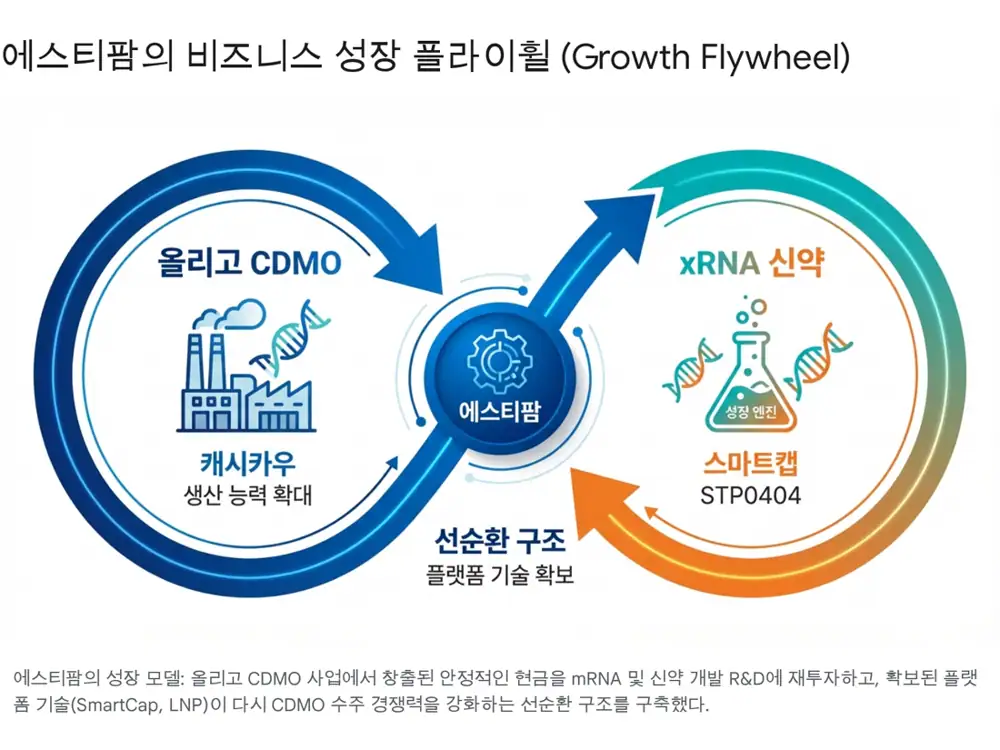

Interpretation: ST Pharm’s investment point is less “it manufactures well” and more “there are not enough qualified manufacturers.” For global pharma, a partner that combines process development, cGMP production, proprietary 5'-Capping technology, and drug-development support becomes scarce.

2. 2025 results: product mix lifted margins

Official fact: Q3 2025 consolidated revenue was KRW 81.9B, up 32.7% from KRW 61.7B a year earlier, and operating profit was KRW 14.7B, up 141.6% from KRW 6.1B.

| Item | Source figure | How to read it |

|---|---|---|

| Oligo revenue | KRW 68.6B, +92.9% YoY | About 83.8% of total revenue, showing identity shift toward high-value oligo API |

| Clinical oligo revenue | KRW 34.5B, up 482% from KRW 5.9B | A leading indicator of larger late-stage clinical sample demand |

| Small-molecule revenue | KRW 100M, down 99.1% from KRW 8.8B | Low-margin business reduction and focus on high-margin segments |

| Operating margin | 9.9% → 18.0% | Product-mix improvement drove company-wide profitability |

For 2025, market consensus is about KRW 326.7B~343.1B of revenue and KRW 48.6B~59.6B of operating profit. That implies revenue growth of about 19~25% and operating profit growth of 75~115%. With cumulative Q3 revenue of about KRW 202.6B, Q4 needs about KRW 120B~140B of revenue.

Interpretation: The target is demanding, but there are drivers. Commercial-volume production from the second oligo plant starts in Q4 2025, the CDMO industry typically has a strong fourth quarter, and commercial products with FDA approval are scheduled for bulk production. Since more than 90% of sales are exports, favorable FX can also support KRW-reported results.

3. Oligo CDMO market: from rare disease to chronic disease

Historically, oligonucleotide drugs were concentrated in rare diseases such as Spinraza. Prices were high, but annual API demand was only tens of kilograms, so the CDMO market was limited.

Official fact: The source says Novartis’ hyperlipidemia drug Leqvio, or inclisiran, changed the market. In chronic diseases with tens of millions of patients, API demand rises from kilograms to tons. As cardiovascular, hepatitis B, and hypertension programs reach commercialization around 2026~2027, the source expects global demand for tens of tons of oligo API.

| Market indicator | Source figure | Meaning |

|---|---|---|

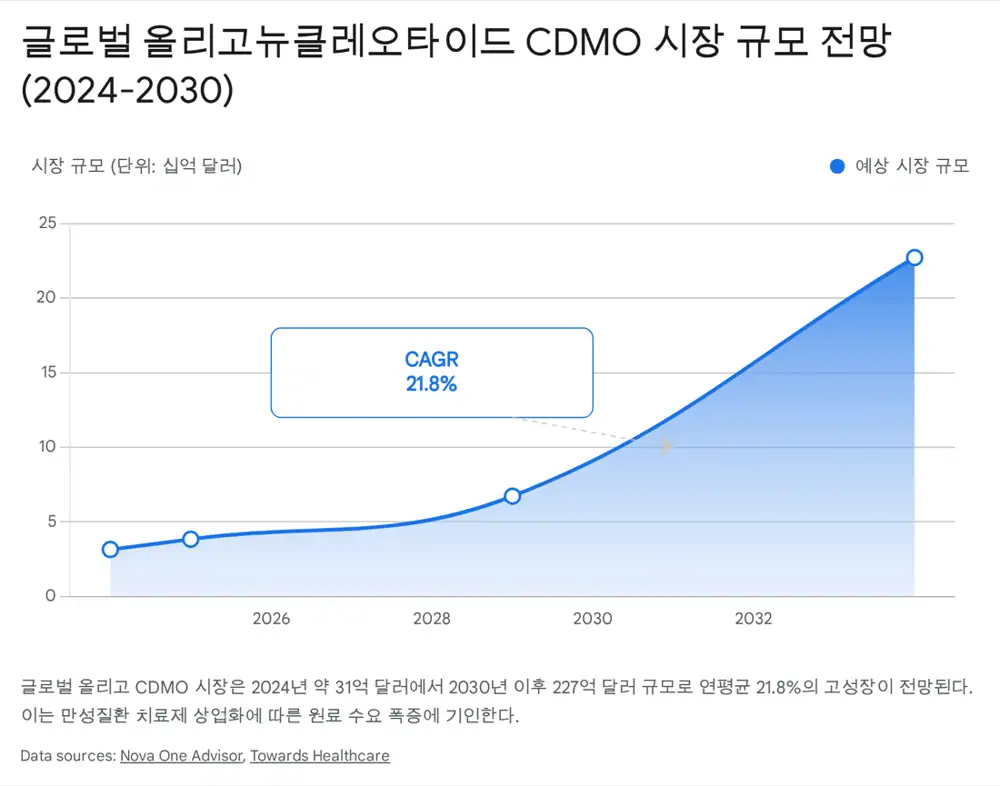

| Global oligo CDMO | About USD 2.5B~3.1B in 2024 | Still early in growth |

| Post-2030 estimate | USD 18B~22B, about KRW 30T | Chronic-disease expansion drives demand |

| CAGR | About 21.8% | Far above the general pharmaceutical market’s 5~7% |

Official fact: The source describes the global oligo CDMO market as supplier-favorable and concentrated among a few companies including ST Pharm, Agilent, and Nitto Denko Avecia. ST Pharm internally produces phosphoramidite monomers, which represent about 30~40% of API production cost, at its Banwol site and integrates this with oligo API production.

Interpretation: Monomer vertical integration creates three advantages: cost reduction, lower supply-chain risk, and quality control from the raw-material stage. Hybrid Enzymatic Ligation can reduce organic-solvent use and enable long-mer oligo synthesis, supporting both ESG and process efficiency.

4. Backlog and the second oligo plant: removing the bottleneck

Official fact: As of the end of September 2025, backlog was about USD 253M, or roughly KRW 354.0B. This was more than double the USD 111M backlog at the end of 2022. In 2025 alone, 13 new CDMO orders were added, bringing the total project count to 43.

The quality of orders is also changing. As of Q3 2025, cumulative commercial oligo revenue was KRW 103.8B, up 105.1% YoY. The source sees commercial volumes from blockbuster-class drugs in hyperlipidemia, blood cancer, cardiovascular disease, and spinal muscular atrophy starting to be reflected.

| Second oligo plant item | Source content |

|---|---|

| Investment | More than KRW 110.0B |

| Start-up | Commercial operation expected from Q4 2025 |

| Production lines | Designed for up to 8~10 lines |

| Initial capacity | Estimated around 8 mole |

| Existing first oligo plant | About 6.4 mole |

| Total capacity after completion | More than 14 mole, more than doubling capacity |

Interpretation: The second oligo plant is not just more floor space. Dedicated lines can reduce cross-contamination risk and strengthen cGMP compliance. The 2026 scenario of revenue above KRW 400.0B and operating margin in the mid-20% range depends on bottleneck removal and fixed-cost leverage.

5. mRNA platform and proprietary pipeline

Official fact: ST Pharm developed its own 5'-Capping technology, a core mRNA manufacturing process, and commercialized it as SmartCap®. The source frames this as a cost-efficient and flexible challenge to the market dominated by TriLink’s CleanCap®.

SmartCap® has started to receive market validation through supply agreements and partnerships with Belgian mRNA vaccine developer Quantoom Biosciences and German specialty-chemicals company Evonik. Q3 2025 mRNA-related revenue was KRW 1.4B, still early, but oncology vaccines and rare-disease therapeutics could add royalty-inclusive growth potential.

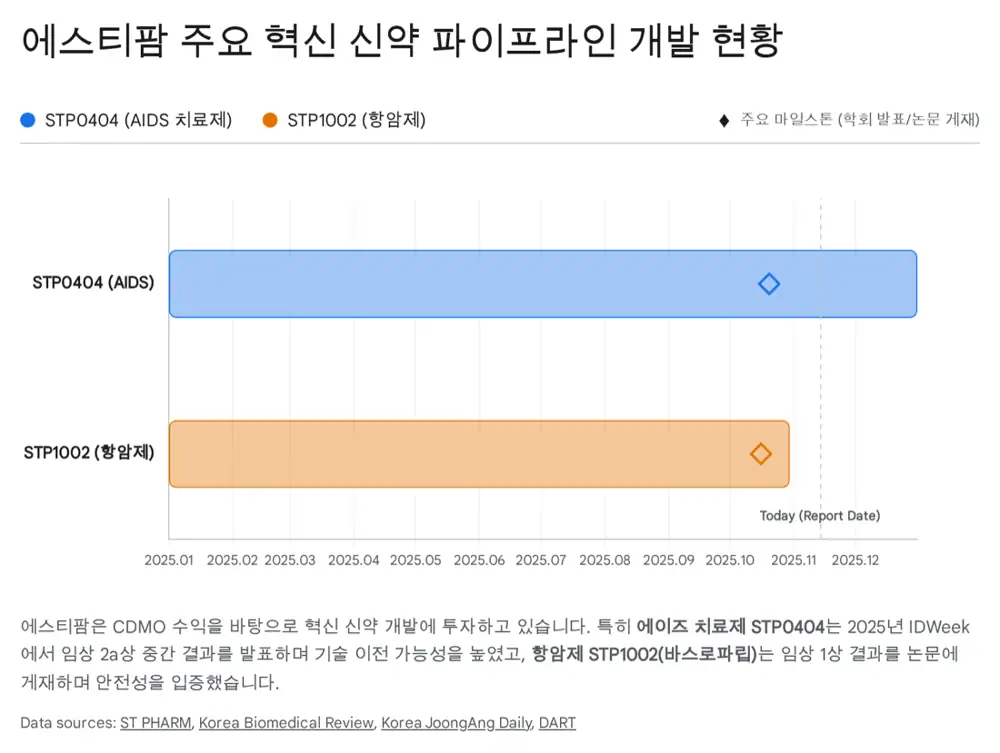

Pirmitegravir

A first-in-class ALLINI HIV candidate. Interim phase 2a results showed average viral-load reduction of 1.191~1.552 log10 copies/mL on day 11.

Basroparib

An oral colorectal-cancer therapy that selectively inhibits tankyrase. A phase 1 paper in October 2025 confirmed safety and tolerability.

Drug-development call option

If licensing succeeds, valuation could move from a conservative CDMO multiple toward a high-growth drug-developer multiple.

STP0404 phase 2a interim data were presented orally at IDWeek 2025 in October 2025. Unlike existing drugs that bind the enzyme active site, STP0404 binds an allosteric site and induces viral genetic material to leave the capsid, according to the source. No serious adverse events were reported, and the source treats functional-cure potential and out-licensing as key milestones.

6. Risks and conclusion

- FX volatility: More than 90% of sales are exports, so sharp KRW appreciation can hurt translated results. Imported raw materials and derivatives provide some natural hedge.

- Customer clinical failure: If customer programs fail or approvals are delayed, orders can be canceled or reduced. The 43-project portfolio creates diversification benefits.

- Geopolitics and the Biosecure Act: The Biosecure Act can benefit ST Pharm by pressuring Chinese biotech suppliers, but supply-chain and trade-rule changes still require monitoring.

Official fact: The source forecasts 2026 revenue to exceed KRW 400.0B and operating margin to remain above 15%. ROE is expected to improve from 7.8% in 2024 to 9~10% in 2025 and potentially settle in double digits in 2026.

Interpretation: The conclusion is “Buy the Transition.” The market offers structural oligo CDMO shortage, the company has monomer vertical integration and SmartCap®, and momentum comes from second-oligo-plant commercialization and STP0404 clinical data. Backlog and second-plant utilization matter more than short-term quarterly volatility.

Sources

- Original post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224114969546

- KRX semiannual report: https://kind.krx.co.kr/common/disclsviewer.do?method=search&acptno=20240814002189&docno=&viewerhost=&

- IBK Securities ST Pharm report: https://www.ibks.com/company/common/download.jsp?filepath=/files/tradeinfo/busreport&filename=20250911194235930_ko.pdf

- Mirae Asset Securities ST Pharm report: https://securities.miraeasset.com/bbs/download/2139563.pdf?attachmentId=2139563

- Hit News oligo supply expansion: https://www.hitnews.co.kr/news/articleView.html?idxno=68921

- Towards Healthcare Oligonucleotide CDMO Market: https://www.towardshealthcare.com/insights/oligonucleotide-cdmo-market-sizing

- Nova One Advisor Oligonucleotide CDMO Market: https://www.novaoneadvisor.com/report/oligonucleotide-cdmo-market

- ROA ST Pharm material: https://static.roa.ai/research/company/20251030_company_743373000.pdf

- ST Pharm STP0404 announcement: https://www.stpharm.co.kr/ko/pr/all/%EC%95%88%EB%82%B4-pirmitegravir-stp0404-%EC%9E%84%EC%83%812a%EC%83%81-%EC%A4%91%EA%B0%84%EA%B2%B0%EA%B3%BC-10%EC%9B%94-%EA%B8%80%EB%A1%9C%EB%B2%8C-%ED%95%99%ED%9A%8C%EC%97%90%EC%84%9C-%EB%B0%9C

- Korea Biomedical Review STP0404: https://www.koreabiomed.com/news/articleView.html?idxno=29336

- Korea JoongAng Daily STP0404: https://koreajoongangdaily.joins.com/news/2025-10-29/business/guestReports/ST-Pharms-Primitegravir-offers-potential-breakthrough-in-HIV-treatment/2431915