DEEP RESEARCH · ILDONG PHARMACEUTICAL

Ildong Pharmaceutical Deep Dive: Structural Turnaround and Yunovia Pipeline

A review of the R&D split-off, oral GLP-1 candidate, and P-CAB asset redeployment

0. Bottom line first

The core change at Ildong is the separation of high-cost R&D into Yunovia, which makes the parent company's operating profitability visible while keeping upside from assets such as ID110521156 and fexuprazan/padoprazan-style P-CAB development. The clinical Phase 2 uncertainty, KRW 30 billion convertible-bond overhang, and global obesity-drug race must be considered together.

Core business profitability

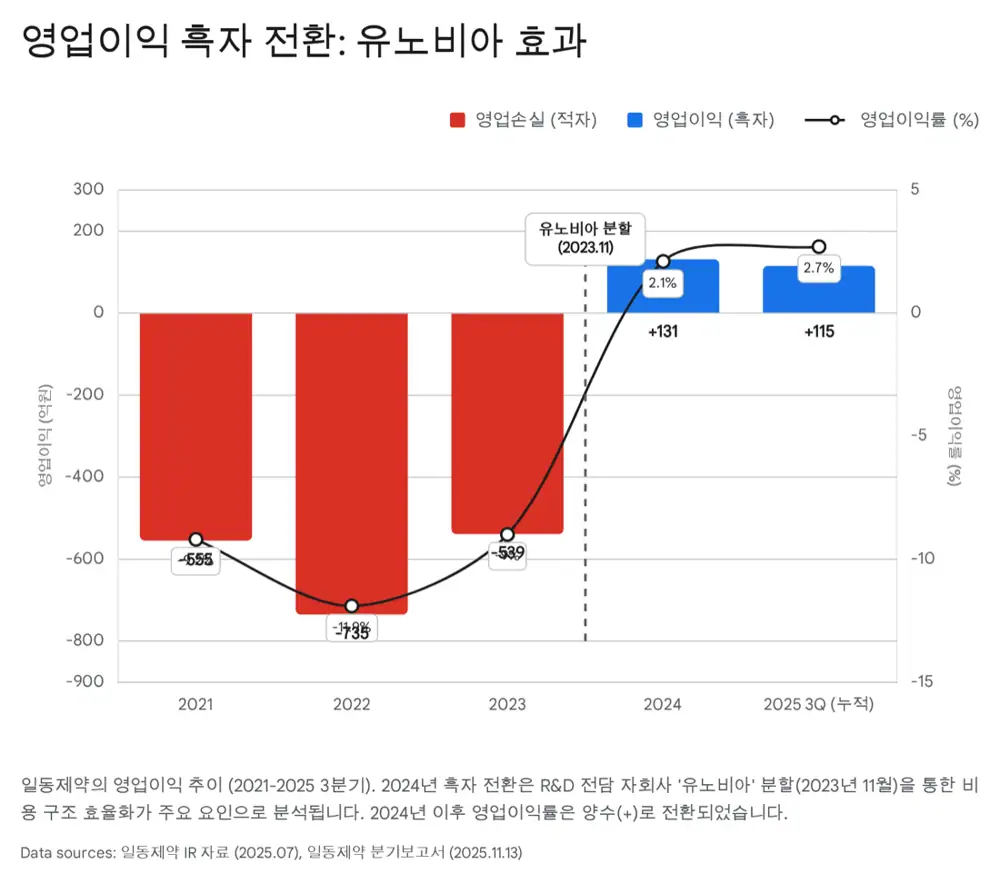

The source highlights 2024 separate operating profit of KRW 13.1 billion and an 8.2% operating margin.

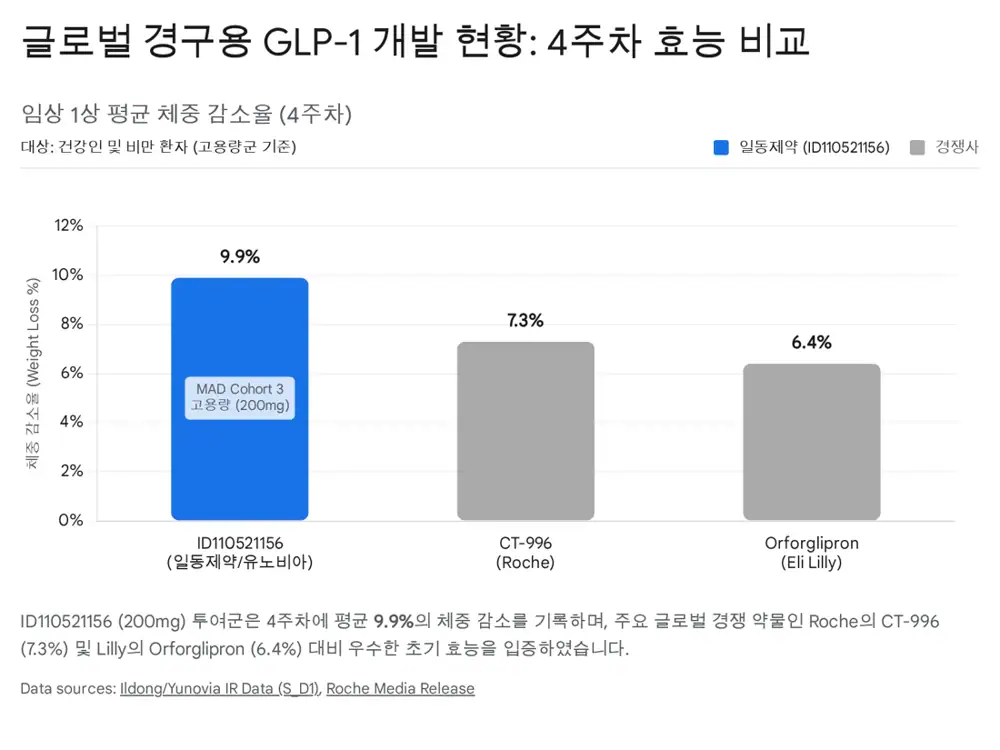

ID110521156

An oral small-molecule GLP-1 receptor agonist, described as having completed Phase 1 and preparing for Phase 2.

CB and clinical risk

KRW 30 billion convertible bonds, a KRW 18,427 conversion price, and 16-week U.S. Phase 2 data are key checkpoints.

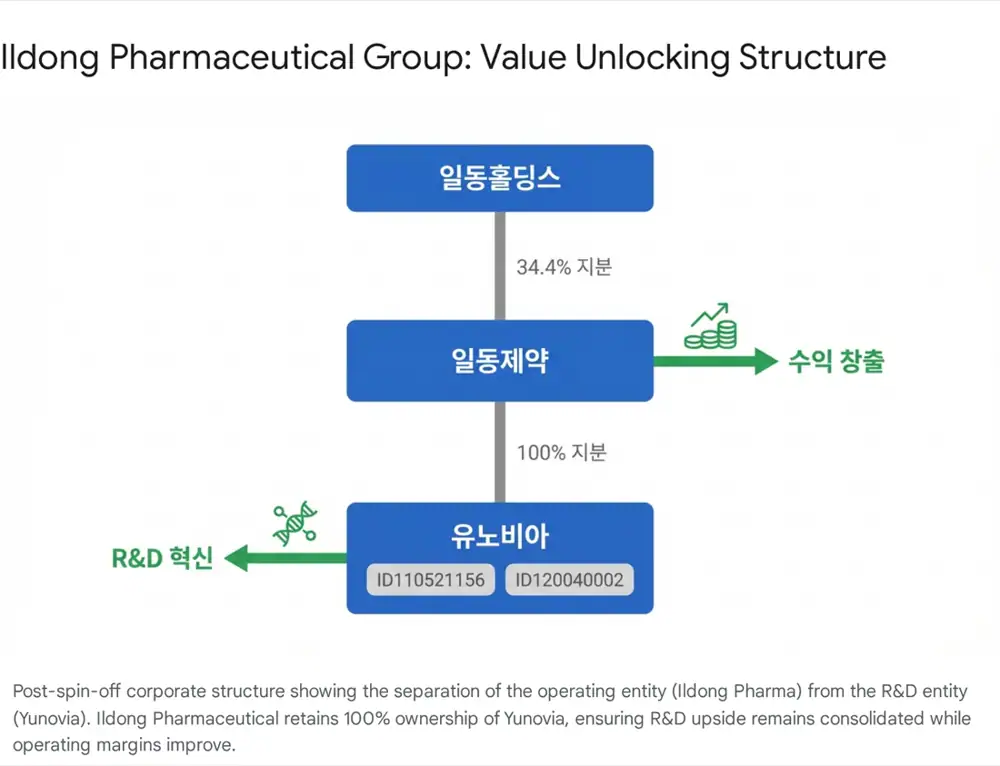

1. Corporate structure change

Official fact: The source states that Ildong was founded in 1941, reorganized under a holding-company structure in 2016, and had capital of KRW 28.1 billion and 1,056 employees at year-end 2024. Ildong Holdings owns 34.4% of Ildong Pharmaceutical, while Ildong owns 100% of Yunovia and Ilead BMS.

Interpretation: Yunovia is not just an accounting carve-out. It separates the parent company's cash-generating pharmaceutical business from a more flexible biotech vehicle for financing and licensing.

2. Financial turnaround

Official fact: The source gives cumulative Q3 2025 consolidated revenue of KRW 419.913 billion. It says the separate operating profit turned to KRW 13.1 billion in 2024 with an 8.2% separate operating margin, while cumulative Q3 2025 R&D expense was KRW 26.77 billion, about 6.46% of revenue.

Interpretation: The change is more about cost structure than sales growth. R&D once approached 20% of sales; after the split, the core business's earnings power became visible again.

| Item | Source figure | Meaning |

|---|---|---|

| Cumulative Q3 2025 revenue | KRW 419.913 billion | Maintained scale of the pharma business |

| 2024 separate operating profit | KRW 13.1 billion | Turnaround after large losses |

| 2024 separate operating margin | 8.2% | Recovered core profitability |

| Cumulative Q3 2025 R&D | KRW 26.77 billion, 6.46% of sales | R&D at a more manageable level |

3. Pipeline: GLP-1 and P-CAB

Official fact: ID110521156 is described as an oral small-molecule GLP-1 receptor agonist that has completed Phase 1 and is preparing for Phase 2. The source compares it with Lilly's orforglipron and Roche's CT-996, and highlights No Titration and No Food Effect convenience markers.

Official fact: The P-CAB candidate ID120040002, padoprazan in the source, had Korean rights licensed to Daewon Pharmaceutical, and Ildong later acquired all related assets and rights from Yunovia for about KRW 9.4 billion.

Interpretation: GLP-1 is the global licensing option; P-CAB is the nearer commercialization option. Moving a later-stage asset back to the sales-capable parent while funding Yunovia looks like deliberate capital allocation.

4. Market backdrop and risks

Official fact: The source cites an obesity-drug market potentially exceeding USD 100 billion by 2030 and says Goldman Sachs expects oral pills to represent 25% of the obesity-drug market. It also cites P-CAB market growth from USD 4 billion in 2024 to USD 7.5 billion in 2035.

Interpretation: The megatrend is attractive, but Ildong is a later entrant. Four-week Phase 1 data cannot settle long-term safety or plateau questions, so the 16-week U.S. Phase 2 profile is the key test.

Main risks

- Phase 1 success does not guarantee Phase 2 success.

- KRW 30 billion of convertible bonds may dilute existing shareholders.

- Lilly, Roche, Pfizer, Hanmi Pharm, and Dong-A ST all intensify the competitive race.

5. Investment view

I read Ildong as a hybrid: a parent with restored cash flow and a biotech subsidiary with high-upside options. That combination can re-rate sharply if it works, but the clinical and financing variables are still real. The U.S. Phase 2 start, P-CAB Phase 3 completion, and tangible licensing progress are the events I would track.

Sources

- 네이버블로그 원문: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224114785528

- 일동제약, 자회사 P-CAB 신약 권리 94억원에 인수 - 데일리팜: https://m.dailypharm.com/user/news/333352

- ID110521156 / Ildong - LARVOL DELTA: https://delta.larvol.com/Products/?ProductId=97b95328-9059-4357-af31-9178d461593b

- 일동제약 P-CAB 후보물질 양수 배경: https://drive.google.com/open?id=1p8uem3u-FlKl7B_3cbYh5wZo6QpbpkRJ0JeseXyoFXI

- 일동제약, 300억 규모 전환사채 발행 - 히트뉴스: https://www.hitnews.co.kr/news/articleView.html?idxno=49159

- Goldman Sachs obesity drug market view: https://www.goldmansachs.com/insights/articles/the-anti-obesity-drug-market-may-prove-smaller-than-expected

- Lilly oral GLP-1 orforglipron Phase 3 release: https://investor.lilly.com/news-releases/news-release-details/lillys-oral-glp-1-orforglipron-demonstrated-superior-glycemic

- Pfizer discontinues danuglipron development: https://www.pharmexec.com/view/pfizer-discontinues-development-danuglipron-chronic-weight-management

- Roche CT-996 Phase I release: https://www.roche.com/media/releases/med-cor-2024-07-17

- BioSpace on Roche obesity pill safety concerns: https://www.biospace.com/drug-development/roches-obesity-pill-candidate-hit-with-safety-concerns-despite-strong-efficacy-data

- 더바이오 파도프라잔 도입 기사: https://www.thebionews.net/news/articleView.html?idxno=20218

- J.P. Morgan obesity drugs research: https://www.jpmorgan.com/insights/global-research/current-events/obesity-drugs

- P-CAB market size report: https://www.wiseguyreports.com/reports/potassium-competitive-acid-blocker-p-cab-market