DEEP RESEARCH · AUTOCRYPT

AUTOCRYPT: Vehicle Security Infrastructure and Valuation Re-rating in the SDV Era

A report on UN R155/156, V2X-PKI, IVS, PnC, royalty transition, and overhang risk

0. Bottom line first

As vehicles become SDVs, cybersecurity shifts from optional software to required safety and regulatory infrastructure. Near-term overhang and losses are risks, but confirmed royalty revenue could support valuation re-rating.

Official fact: The source states Date: December 18, 2025, Ticker: 331740.KQ, Rating: BUY, Target Price KRW 24,000, and Current Price KRW 15,580 as of Dec. 12, 2025.

Interpretation: The target price is the source author's valuation assumption, not investment advice. Royalty revenue, cash flow, lock-up releases, and new orders must be checked first.

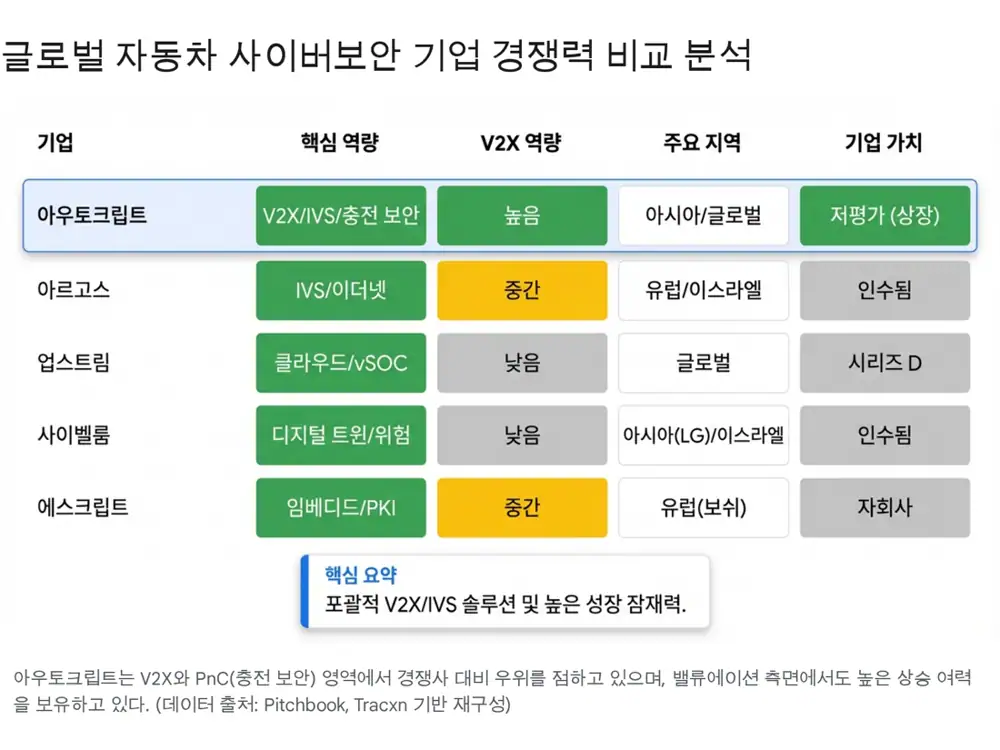

1. Investment point: regulatory supercycle

The source argues that UN R155/156 became mandatory for all vehicle types in Europe from July 2024, making vehicle cybersecurity a survival requirement rather than an optional feature. References with Hyundai Motor Group and other OEMs are important trust assets in a high-barrier automotive market.

2. Technology moat: combining V2X and IVS

Traffic trust layer

The source mentions capacity to issue and manage more than 50 million certificates.

Misbehavior detection

Local and Global MBD detect and respond to tampered communication messages.

In-vehicle network security

Provides firewalls and intrusion detection for CAN, CAN-FD, and Ethernet communications.

Lightweight crypto module

Optimized for real-time encryption and decryption in resource-constrained ECUs.

3. Partnerships and expansion

Collaboration with Hyundai Motor Group, Hyundai AutoEver, and Hyundai Mobis is the key domestic reference. The source says security application may expand from IVI controllers to five controllers including TCU and BSM, and potentially to more than 20 controllers when OTA adoption increases.

Official fact: The source says AUTOCRYPT signed a 26-month Cyber Resilience Act response project with LS Mtron in December 2025.

Interpretation: This suggests possible expansion beyond cars into agricultural and industrial machinery.

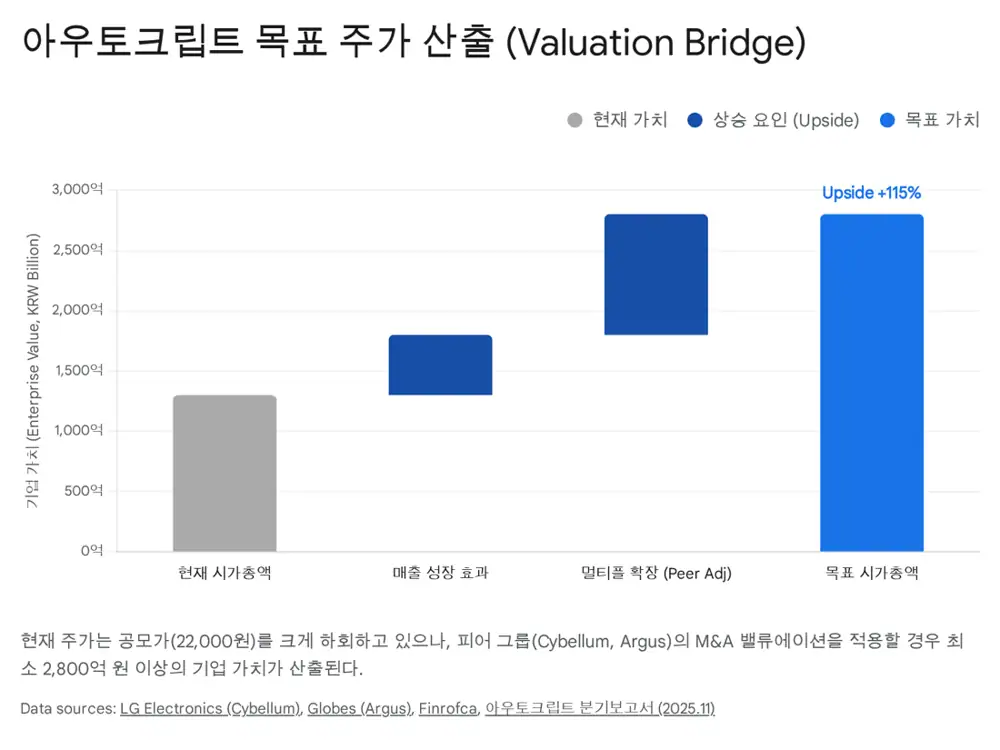

4. Valuation frame

| Item | Source figure/assumption | Meaning |

|---|---|---|

| IPO price | KRW 22,000 | Listing expectation benchmark |

| Current price | KRW 15,580 on Dec. 12, 2025 | Described as 30-40% below IPO price |

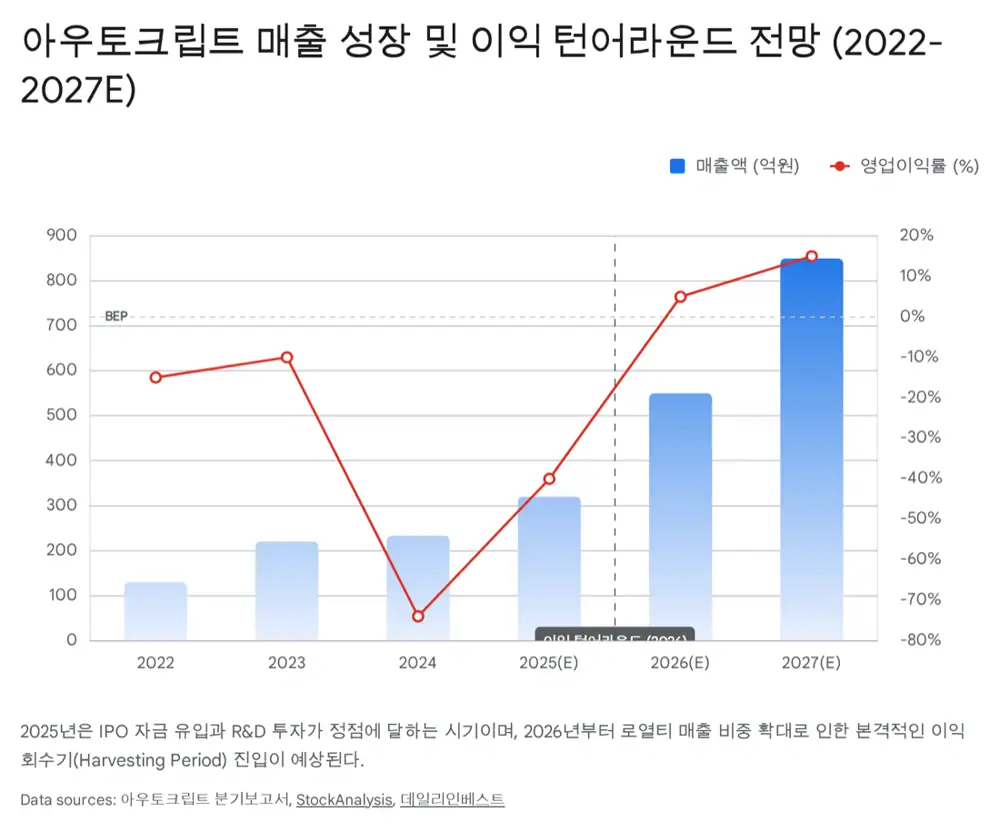

| 2026F revenue | KRW 35bn | Assumes royalty revenue acceleration |

| Target PSR | 8.0x | Source's conservative cybersecurity peer assumption |

| Fair market cap | KRW 280bn | KRW 35bn × 8.0 |

| Target price | About KRW 24,000 | Source conclusion of roughly 50-70% upside |

5. Risks and mitigation logic

- Overhang: the source cites a 5.28% mandatory holding commitment ratio and 35% tradable shares on listing day.

- SDV delay: slower OEM SDV transition could delay royalty revenue.

- Competition: Israeli security startups and global big tech may enter the market.

- Mitigants: UN R155 is mandatory, and the V2X+IVS+PnC portfolio plus Asian references provide defense.

6. My checkpoints

- Whether royalty revenue improves breakeven economics in 2026.

- Whether overseas OEM or Tier 1 orders beyond Hyundai Group are confirmed.

- Whether the LS Mtron CRA project becomes a precedent for non-auto revenue.

- Whether the stock moves only on expectations after overhang pressure eases.

Sources

- 네이버블로그 원문: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224114553706

- Investing.com: https://www.investing.com/equities/autocrypt

- 주달 2025.12.11: https://www.judal.co.kr/?view=stockAI&shareToken=GThIXyExR9rkpfqw

- VicOne UN R155: https://vicone.com/why-vicone/un-r155

- MarketsandMarkets: https://www.marketsandmarkets.com/Market-Reports/cyber-security-automotive-industry-market-170885898.html

- DailyInvest: http://www.dailyinvest.kr/news/articleView.html?idxno=69505

- CYEQT: https://www.cyeqt.com/en/un-r155-worldwide-how-countries-regulate-vehicle-cybersecurity-in-2025/

- YouTube: https://www.youtube.com/watch?v=M3g0ohstVk4

- NewsTomato: https://www.newstomato.com/ReadNews.aspx?no=1267186

- Catch: https://www.catch.co.kr/Comp/CompInfo/JS9571

- 주달 2025.12.03: https://www.judal.co.kr/?view=stockAI&shareToken=RdNNFklgWOxqocSO

- LG Cybellum: https://www.lg.com/global/newsroom/news/vehicle-component-solutions/lg-to-acquire-israeli-vehicle-cybersecurity-risk-assessment-solution-provider-cybellum/

- Globes Argus: https://en.globes.co.il/en/article-continental-buys-israeli-co-argus-cyber-security-1001210311

- Finro cybersecurity valuation: https://www.finrofca.com/news/cybersecurity-valuation-mid-2025

- 유진투자증권 PDF: https://www.eugenefn.com/common/files/amail//20250624_B_jongsun.park_2398.pdf