DEEP RESEARCH · Korea DSP Big Three

SemiFive · Gaonchips · AD Technology — 2025-2028 Chiplet War Opens

AI paradigm shift and Samsung Foundry's DSP ecosystem: business models, financials and chiplet roadmaps compared

0. Bottom line first

Korea's design-solution-partner (DSP) sector is consolidating into three camps: "Tech-leader" Gaonchips (2nm GAA + I-Cube packaging vanguard), "Scale-king" AD Technology (500+ engineers + in-house interposer design), and "Platform" SemiFive (SoC platform + RISC-V + UCIe IP). All three depend on the success of Samsung Foundry's 2nm (SF2) node and 2.5D/3D advanced packaging yield. SemiFive's innovation is real but offset by a loss-making P&L (2024 OP −KRW 22.9 bn, NI −KRW 290.9 bn) and IPO-valuation pushback. Gaonchips offers explosive 2026+ upside via PFN/DeepX 2nm references; AD Technology offers earnings stability through HPC server design.

1. AI semis explosion and foundry ecosystem reshuffle

In 2025 the chip industry rides the AI wave. Big-tech ASIC self-sufficiency (Google, Tesla, Meta) is accelerating, and at sub-3nm geometries, design houses (DSPs) evolve from passive "bridges" into full-stack platform partners spanning IP sourcing, packaging design, and yield management.

As Samsung Foundry pushes 2nm GAA + 2.5D/3D advanced packaging (I-Cube, X-Cube), the three core SAFE-ecosystem DSPs — SemiFive, Gaonchips, AD Technology — are more strategically important than ever.

2. SemiFive — platform innovation, financial challenge

2.1 Company overview

Founded 2019. Vision: turn system-semiconductor design into a "platform." Strategic relationship with US RISC-V IP firm SiFive. Co-founder/CEO Cho Myung-hyun (ex-BCG).

2.2 Core model — SoC design platform

Pre-verified "subsystem libraries" for common blocks (CPU, memory interface, PCIe etc.) assembled via an automated "design engine."

- Reusability: Customers bring only their core IP (e.g. a custom NPU) and drop it on the platform. SemiFive cites up to 75% headcount reduction and 57% shorter development time.

- Platforms:

- Sesame (14nm AI inference) — AI accelerators, datacenter, ADAS on Samsung 14nm FinFET.

- Fermion (5nm HPC) — hyperscale / cloud servers on Samsung 5nm FinFET.

- WalnutCake (14nm AIoT) — low-power IoT, edge, wearables.

Already won first-generation chip projects from leading Korean AI startups (FuriosaAI, Rebellions, Mobilint). 2024 brought overseas wins — a US memory-device player "I" and a Chinese AI platform player "J."

2.3 Financial risk — growing pains and the profitability dilemma

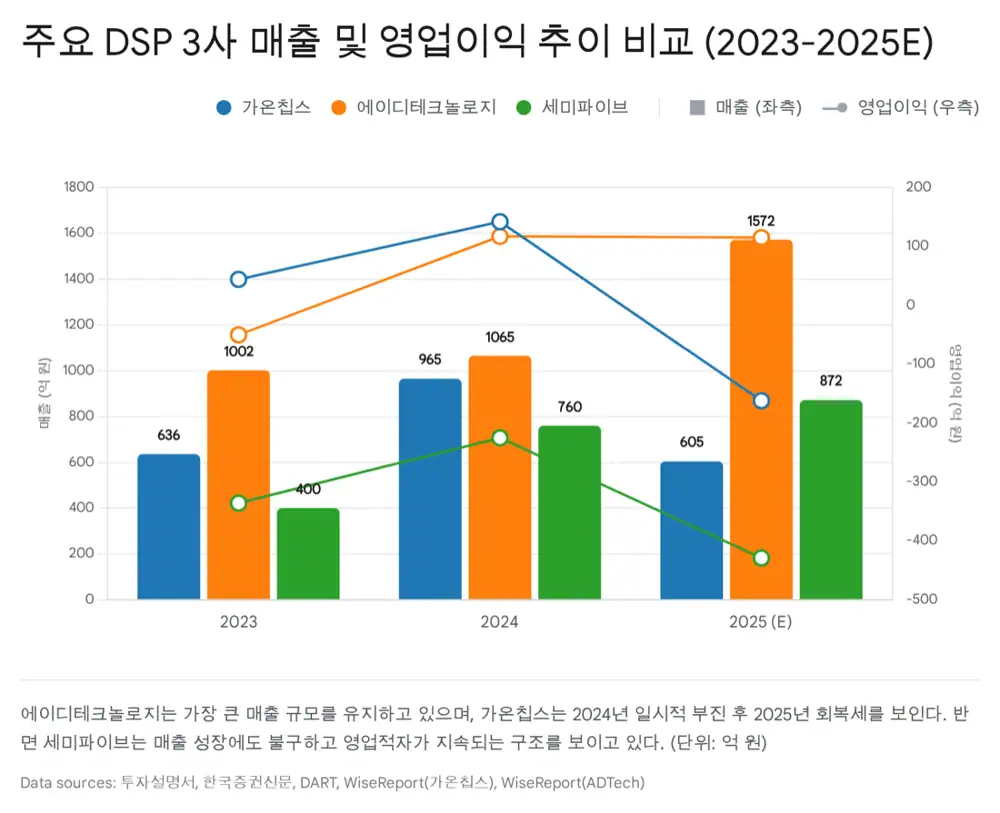

Official fact: 2024 consolidated revenue KRW 111.8 bn, operating loss KRW 22.9 bn, net loss (impacted by derivative valuation losses) about KRW 290.9 bn. As of 9M-2025, mass-production revenue share was 23.1%.

- High fixed costs: platform R&D, 357 engineers (2024), stock-based comp.

- Accumulated deficit → IPO valuation contention → IPO proceeds intended for debt repayment / B/S repair.

- True turnaround requires the NRE-to-mass-production "scale-up" step.

2.4 Peer-selection controversy

Peers cited for IPO pricing: Taiwan's Faraday, Alchip, GUC — already trillion-won market caps and steady profits. Applying the same PER to a loss-making SemiFive is what's stoking the overvaluation debate.

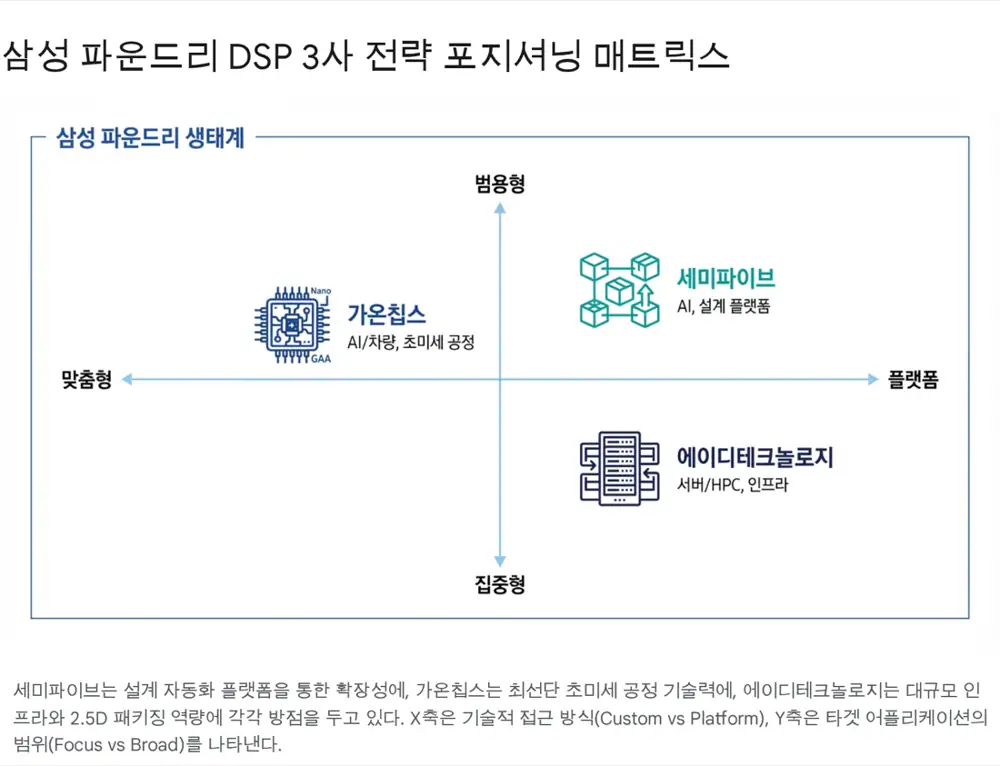

3. Peer deep dive: Gaonchips vs AD Technology

3.1 Gaonchips — the tech vanguard of Samsung Foundry

- 2nm GAA wins: Won a turnkey project from Japan's AI unicorn PFN (Preferred Networks) on Samsung 2nm — Samsung Foundry's first global flagship 2nm reference. Korea's DeepX 'DX-M2' next-gen chip also on Samsung 2nm.

- Japan strategy: Gaonchips Japan attacking non-memory demand — PFN is the proof.

- Financials: 2023 sales KRW 63.6 bn, OP KRW 4.4 bn (profitable). 2024–2025 likely a temporary loss as advanced-node R&D peaks; explosive growth expected from 2026 as backlog converts to mass-production revenue.

3.2 AD Technology — economies of scale + infrastructure

- Former TSMC VCA → moved into the Samsung ecosystem. About 500+ design engineers — best at executing massive projects.

- Late 2023 won a 3nm server-grade chip project; in-housed interposer design targets the HPC market.

- Turnaround in 3Q-2024: revenue KRW 75.5 bn, back to operating profit.

3.3 Three-way model comparison

| Item | SemiFive | Gaonchips | AD Technology |

|---|---|---|---|

| Core model | SoC Platform Provider | High-End Tech Service | Scalable Infra Provider |

| Keywords | Automation · reuse · platform | Advanced node (GAA) · know-how | Large-scale infra · 2.5D packaging |

| Customers | AI startups · SMB fabless | Global big-tech · AI / Auto | Server / HPC · global majors |

| Position in Samsung Foundry | Ecosystem-expansion accelerator | Preferred 2nm/3nm advanced-node partner | Executor of big server / HPC projects |

| Revenue mix | Lower NRE + high mass-prod royalty target | High NRE + steady mass-prod | Balanced NRE + mass-prod |

| Headcount | ~350 (incl. IP sub) | ~250+ (expanding) | ~500+ (largest) |

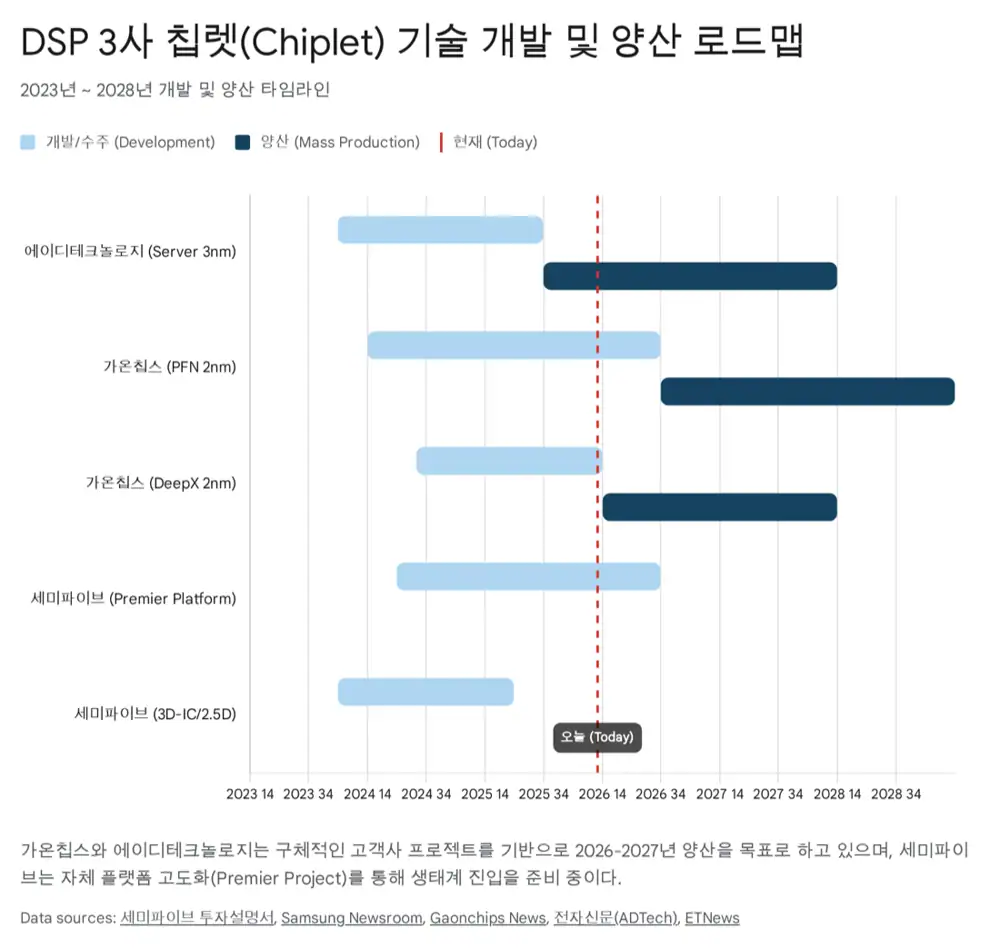

4. Chiplets — the next battlefield

Chiplets replace monolithic dies with multiple dies combined in a single package — improving yield, lowering cost, enabling heterogeneous integration.

4.1 Gaonchips — commercialization frontline, "turnkey"

- The PFN 2nm turnkey project includes Samsung's 2.5D package I-Cube S: logic + HBM on a silicon interposer. Targeting mass production by 2027.

- Demonstrates capability across design → packaging → test as a packaging-solution provider.

4.2 AD Technology — infrastructure-led 2.5D/3D

- Its 2023 3nm server project includes its own interposer design — taking the lead at the packaging stage.

- Strong "big die" handling from its TSMC heritage.

4.3 SemiFive — IP-based platformization

- In-house R&D project 'Premier' developing UCIe controller / PHY IP — the standardized chiplet interconnect.

- Pre-research on 3D IC memory integration. US R&D center. Combined with subsidiary Analog Bits' interface IP, SemiFive aims to be the supplier of "chiplet building materials (IP)."

Interpretation: If Gaonchips and AD Technology are the construction contractors building chiplets, SemiFive is the building-materials (IP) supplier. Early revenue visibility is lower, but scalability is higher once the market matures.

5. Customer base & revenue concentration

5.1 SemiFive — variety with concentration

Per the IPO prospectus, top-8 customer concentration in 2024 was 87.24%. Key customers: Rebellions, FuriosaAI, Mobilint. Export share rose to 21.26% in 9M-2025, yet performance is still tied to the success of Korean AI startups.

5.2 Gaonchips — global big-tech expansion

Steady cash cows in Korean automotive semis (Telechips, Nextchip) + the new global big-tech anchor PFN. A balanced two-axis exposure (auto + AI accelerators) — the highest-quality portfolio of the three.

5.3 AD Technology — overseas heavyweight customers

Built a memory-controller franchise with SK hynix; since moving to Samsung, secured (undisclosed) overseas server-grade big-tech customers. Server / HPC is less cyclical than mobile and locks in long-tail volume.

6. Conclusion — destiny tied to Samsung Foundry

The three-way split is set: "tech" Gaonchips, "scale" AD Technology, "platform" SemiFive. Their fates depend on Samsung Foundry SF2 success and 2.5D/3D advanced-packaging yields. If Samsung closes the gap on TSMC, the most technically intertwined Gaonchips reaps the earliest and largest reward.

- SemiFive: armed with a platform innovation, but priced rich and still loss-making. Watch whether the chiplet-IP strategy lands.

- Gaonchips: holds the strongest card — 2nm + chiplet mass production. Bet on the 2026+ acceleration rather than this year's numbers.

- AD Technology: solid fundamentals at a depressed valuation. Server-market traction is the rerating key.

Sources

- Original post (Naver Blog): https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224114507873

- 고평가 논란 겪은 '몸값 1조' 세미파이브…정정해도 평가 '반반': https://marketin.edaily.co.kr/News/Read?newsId=01718726642369000

- Samsung Electronics To Provide Turnkey Semiconductor Solutions With 2nm GAA Process and 2.5D Package to Preferred Networks: https://news.samsung.com/global/samsung-electronics-to-provide-turnkey-semiconductor-solutions-with-2nm-gaa-process-and-2-5d-package-to-preferred-networks

- [ChosunBiz] DEEPX Signs 2nm Process Agreement with Samsung Foundry and GAONCHIPS for Next-Generation Generative AI Chip 'DX-M2': https://www.gaonchips.com/en/sub/news/view.php?idx=268

- DEEPX Signs 2nm Process Agreement with Samsung Foundry to Develop World's First On-Device Generative AI Chip 'DX-M2' (GlobeNewswire): https://www.globenewswire.com/news-release/2025/08/20/3136461/0/en/DEEPX-Signs-2nm-Process-Agreement-with-Samsung-Foundry-to-Develop-World-s-First-On-Device-Generative-AI-Chip-DX-M2.html

- 가온칩스, 영업적자 확대 속 업황 회복 기대 (한국증권): https://www.ksdaily.co.kr/news/articleView.html?idxno=107315

- 에이디테크놀로지, 첫 3나노 설계 지원 수주 '2.5D 서버용 반도체' 개발 (Daum): https://v.daum.net/v/20231010110108689

- [실적속보] 에이디테크, 3Q 영업이익 1억...흑자전환 (아이투자): https://itooza.com/newsview/2017111411045818706

- [에이디테크놀로지] 분기보고서(일반법인) (KRX 공시): https://kind.krx.co.kr/common/disclsviewer.do?method=search&acptno=20241114001373

- 조명현 세미파이브 '칩렛 내년 양산·3D IC 메모리 개발 추진…글로벌 트렌드 이끌 것': http://technovalue.com/View.aspx?No=3673275

- 가온칩스 주가 (알파스퀘어): https://alphasquare.co.kr/home/stock-summary?code=399720

- 에이디테크놀로지 주가 (알파스퀘어): https://alphasquare.co.kr/home/stock-summary?code=200710

- 에이디테크놀로지 기업현황 (Wisereport): https://comp.wisereport.co.kr/company/c1010001.aspx?cmp_cd=200710