DEEP RESEARCH · BIOPLUS

BioPlus: MDM Crosslinking Technology and Vertical Integration as a Bio-Platform Strategy

From HA filler cash cow to GLP-1, toxin, and DDS platform expansion

0. Bottom line first

My core view is that BioPlus is not just an HA filler manufacturer. It is trying to become a platform company between aesthetics and biopharma by combining MDM® crosslinking technology, the Eumseong Bio-Complex, and the Ubiprotain acquisition. The key test is whether the 2024-2025 margin decline and cash-flow gap are temporary growth pains or structural deterioration.

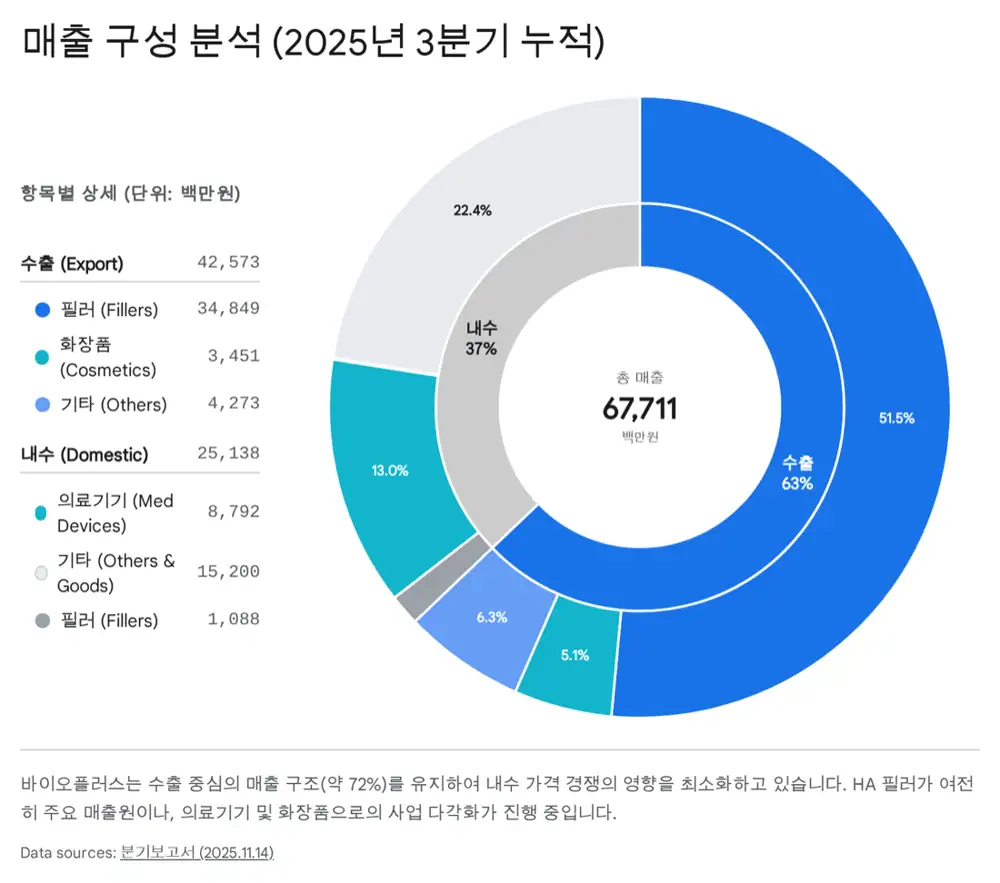

Official fact: The source presents cumulative 3Q25 revenue of KRW 67.7 billion, operating profit of KRW 14.0 billion, and an operating margin of about 20%. Historical operating margins had approached 40-50%, but were adjusted by distribution restructuring and new-business investment.

Interpretation: Reducing low-margin ODM, strengthening direct/branded sales, launching Bonyx, GLP-1 R&D, and global marketing costs weigh on short-term earnings, but can be read as a transition toward higher-quality revenue and more brand control.

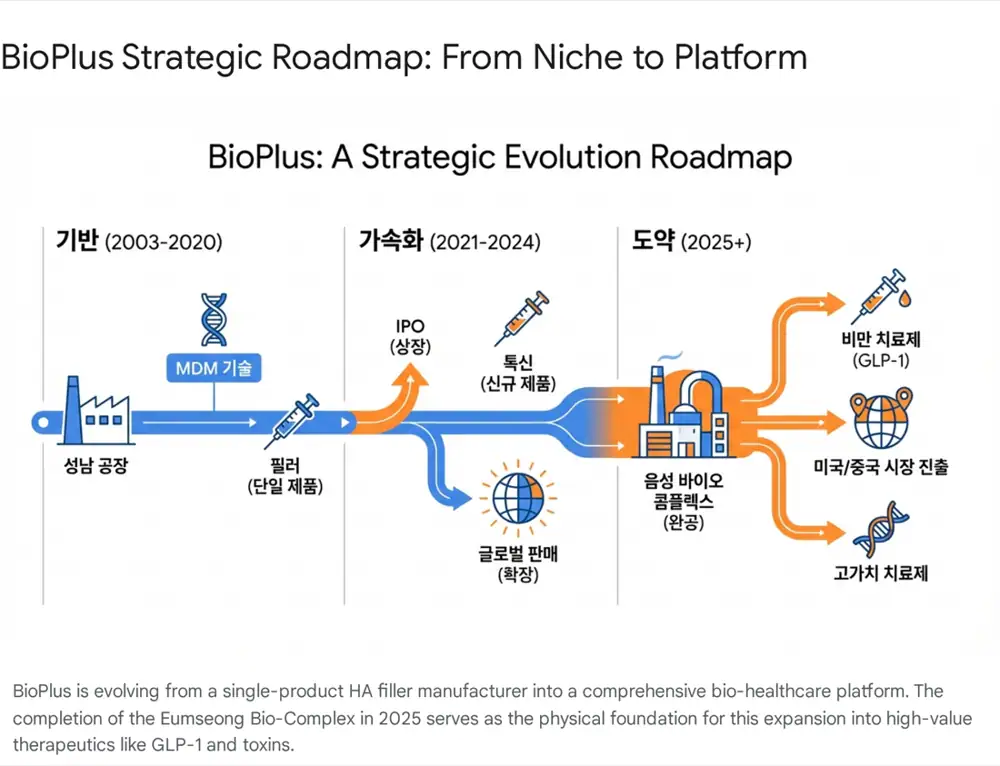

1. Corporate DNA: the contrarian DVS bet

BioPlus began in 2003 as Human Tissue Korea, focused on tissue engineering and human tissue graft materials. The decisive pivot came when BDDE was the standard HA filler crosslinker and BioPlus chose DVS instead. DVS can form stronger, more rigid bonds, but its high reactivity makes residual removal difficult.

Official fact: The source says BioPlus built MDAP™, a multi-step purification technology to remove residual DVS toxicity, and the broader MDM® Technology platform after years of R&D. It received KFDA product approval in 2014.

Interpretation: This pivot changed the company identity from generic manufacturing to material-science technology. CEO Jung Hyun-kyu’s philosophy also favors differentiated physical properties, such as viscoelasticity and moldability, over celebrity-driven advertising.

Jung Hyun-kyu

A technology-centered leader with an environmental-engineering PhD who led the 2021 KOSDAQ listing and owns about 21.57%.

Oh Seung-hwan

Manages financing for the Eumseong Bio-Complex and new businesses, including CB issuance and treasury-share use.

CTO Kim Jin-hwan and team

Researchers from Korean bio companies including LG Life Sciences, Peptron, and Alteogen support protein-recombination and DDS expansion.

2. Business model and global strategy

BioPlus is migrating from ODM toward branded direct sales and private-label contracts with large global partners. About 72% of revenue comes from overseas markets, reflecting a choice to avoid intense domestic price competition and maximize profitability where premium pricing works.

HA fillers

The core business accounting for more than 80% of total revenue.

InterBlock and HyalSyno

Anti-adhesion and joint-tissue repair products partly buffer aesthetic-cycle volatility.

Bonyx

A new post-procedure home-care business with small current contribution but ongoing brand investment.

Official fact: The Hainan project uses a local factory and Class II medical-device production/sales approval instead of simply waiting for NMPA import approval. The source mentions GMP certification for the Hainan plant in March 2025.

For the U.S., BioPlus established BioPlus USA Inc. in 3Q25 to directly manage FDA clinical and approval processes and prepare a sales network. For South America, especially Brazil, the source emphasizes demand for body contouring and fit with high-viscosity fillers.

3. MDM® technology moat

| Item | Source point | Investment interpretation |

|---|---|---|

| BDDE dilemma | Higher crosslinking for durability can increase incomplete crosslinking and toxicity, inflammation, or swelling concerns. | The incumbent standard leaves room for differentiation. |

| DVS solution | DVS has a short molecular length and strong bonding, making fillers firmer and longer-lasting, but purification is difficult. | Commercialization difficulty becomes an entry barrier. |

| MDM innovation | A patented process nearly removes residual DVS toxicity and creates firm but safe fillers. | Differentiated in areas needing structural support, such as nose, chin, and body fillers. |

Interpretation: The lock-in described by the source is closer to physician injection feel than consumer brand awareness. Once physicians become used to high G-prime and moldability, moving back to thinner products becomes harder.

4. Capacity and vertical integration

Official fact: BioPlus invested about KRW 160 billion to build the Eumseong Bio-Complex in Chungbuk. The source says the 2025 completion and ramp-up enable annual capacity for 36 million botulinum-toxin vials, 40 million obesity-treatment units, and 40 million filler syringes.

Subsidiary Infinita produces prefilled syringes and related materials, reducing external dependence and improving quality-control consistency. The acquisition of a 52.96% stake in Ubiprotain is presented as capital allocation that secures protein-recombination technology for botulinum toxin and GLP-1 obesity treatments.

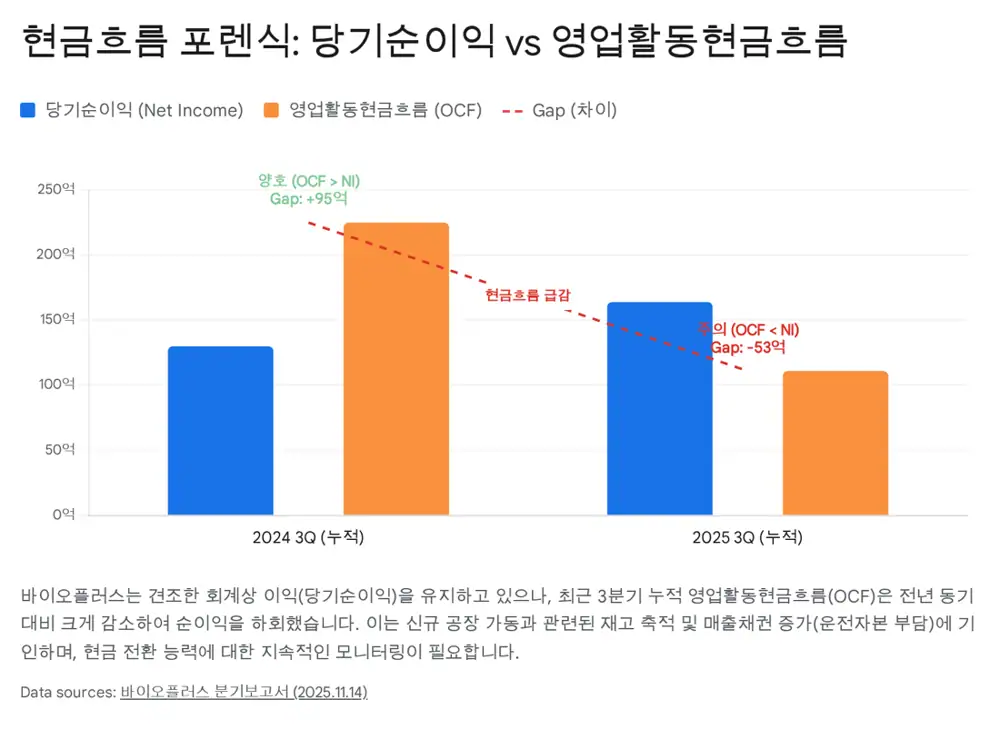

5. Financials and cash flow

2024-2025 was the peak CAPEX period for Eumseong construction. The source argues this hurt near-term free cash flow, but once major investment ends from 2026, operating leverage may emerge despite depreciation.

- Margin decline drivers: ODM reduction, direct-sales transition, Bonyx launch, obesity-treatment R&D, and higher global marketing costs.

- Cash-flow gap: Net income is positive, but OCF tends to be lower or negative, with accounts receivable and inventories cited as the cause.

- Financing: CB proceeds were used for production facilities such as the Eumseong plant rather than operating expenses, which the source frames as “good debt.”

6. Scenarios and risks

Bull Case

- MDM technology acts as a hard-to-copy moat and supports excess returns.

- Eumseong Bio-Complex operation removes supply constraints and lifts revenue scale.

- If GLP-1 pipelines such as liraglutide generics and semaglutide microneedle patches produce clinical progress, the source argues the valuation could rerate from medical-device multiples to biopharma multiples.

Bear Case

- If China NMPA or U.S. FDA approval is delayed, Eumseong depreciation can weigh on earnings.

- Slow conversion of inventories and receivables into cash can create additional financing or liquidity pressure.

- If major regulators raise new safety issues around DVS crosslinkers, the company’s core MDM technology base could be challenged.

Sources

- Original post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224112263213

- Interview with BioPlus Chairman Jung Hyun-kyu - Daum: https://v.daum.net/v/20250416175225828?f=p

- BDDE/DVS safety debate - Daum: https://v.daum.net/v/ECuvw7orX5

- BioPlus biomaterials press release: https://ubioplus.com/press-release-bioplus-application-of-biomaterials-and-creation-of-new-growth-engines-for-bio-industry/

- BioPlus 6.6 trillion won subscriptions press release: https://ubioplus.com/press-release-bioplus-which-has-6-6-trillion-won-in-subscriptions-leaps-as-a-bio-company-that-encompasses-treatment-and-beauty/

- Asia Economy CORE: https://core.asiae.co.kr/article/2024121607520586161

- Medipana News on Hainan GMP approval: https://www.medipana.com/article/view.php?page=86&sch_menu=3&sch_cate=D&news_idx=340049

- DeneB Science: https://bioplus-deneb.com/DeneBScience

- BioPlus Filler Series PDF: https://ubioplus.com/wp-content/uploads/2022/07/IPCHE-Filler_Bochure_en_ver.0_220526_web.pdf

- Pharm EDaily on Eumseong plant completion: https://pharm.edaily.co.kr/news/read?newsId=01935206642169576

- Yakup on Ubiprotain control acquisition: http://m.yakup.com/news/index.html?mode=view&pmode=&cat=12&cat2=&cat3=&nid=262218&num_start=34430