DEEP RESEARCH · LX INTERNATIONAL

LX International and the Re-Rating Test for Korean Trading Houses

A comparison of LX's resource-logistics hybrid with POSCO International, Samsung C&T, and Japanese sogo shosha

0. Bottom line first

My conclusion is that LX International is in the middle of redirecting cash flow from coal and logistics into nickel and green materials, but the market has not yet recognized it as either a Japanese-style investment holding company or a POSCO International-style energy conglomerate.

Official fact: The source says Japanese trading houses were re-rated to roughly 1.5-2.0x PBR, and more broadly 1.5-2.3x, while Korean peers remain around 0.4-1.1x PBR as of 3Q25.

Interpretation: LX's discount appears to come not just from slow growth, but from coal profit dependence, captive LX Pantos volume, and a less forceful shareholder-return roadmap than Japanese peers.

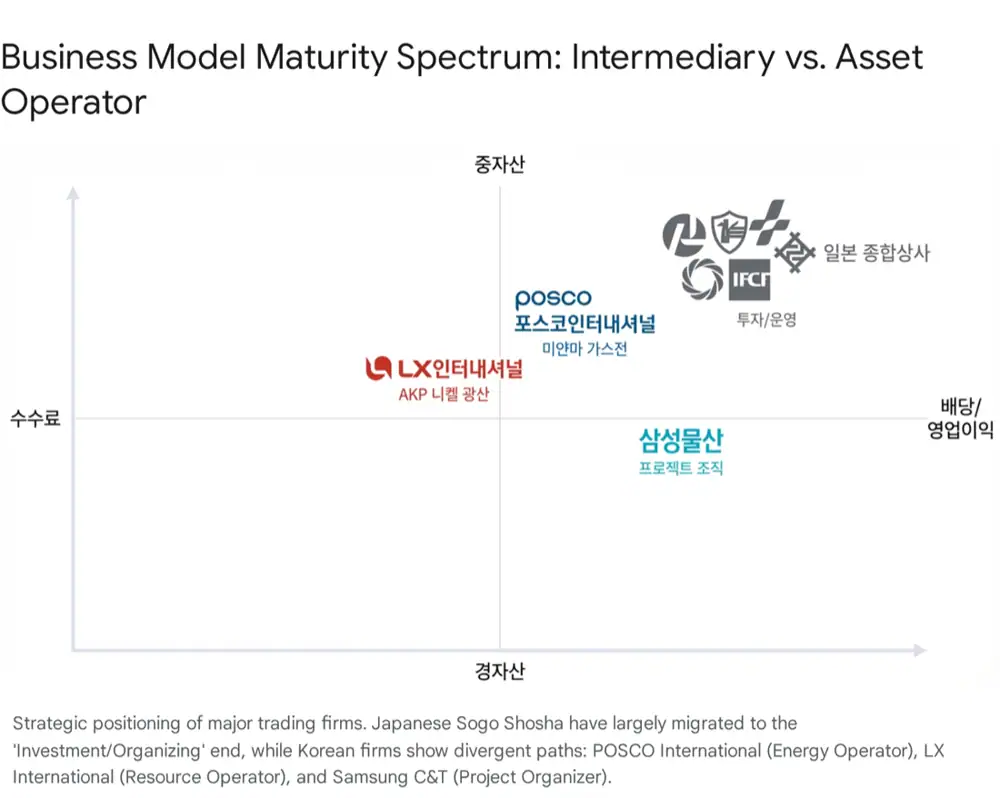

Resource-logistics hybrid

An operator model combining coal and nickel resources with LX Pantos logistics cash flow.

Energy integration

An asset-heavy corporation linking LNG exploration, terminals, power generation, and steel captive flow.

Project organizer

An asset-light model built around renewable project development and sale.

1. Structural evolution of trading companies

The traditional trading company arbitraged information gaps across borders. But as the internet and direct exports removed that information monopoly, simple trading margins settled around 0.5-1.5%. Global trading companies therefore moved beyond brokerage into direct operation of businesses or equity investments that generate dividends and equity-method income.

Japan's Mitsubishi Corporation and ITOCHU shifted after the 1990s toward investment-holding-company models, lifting contributions from non-resource areas such as convenience stores, food, and autos. ITOCHU is presented as a model of de-resource-ization, generating about 75-80% of net income from non-resource businesses.

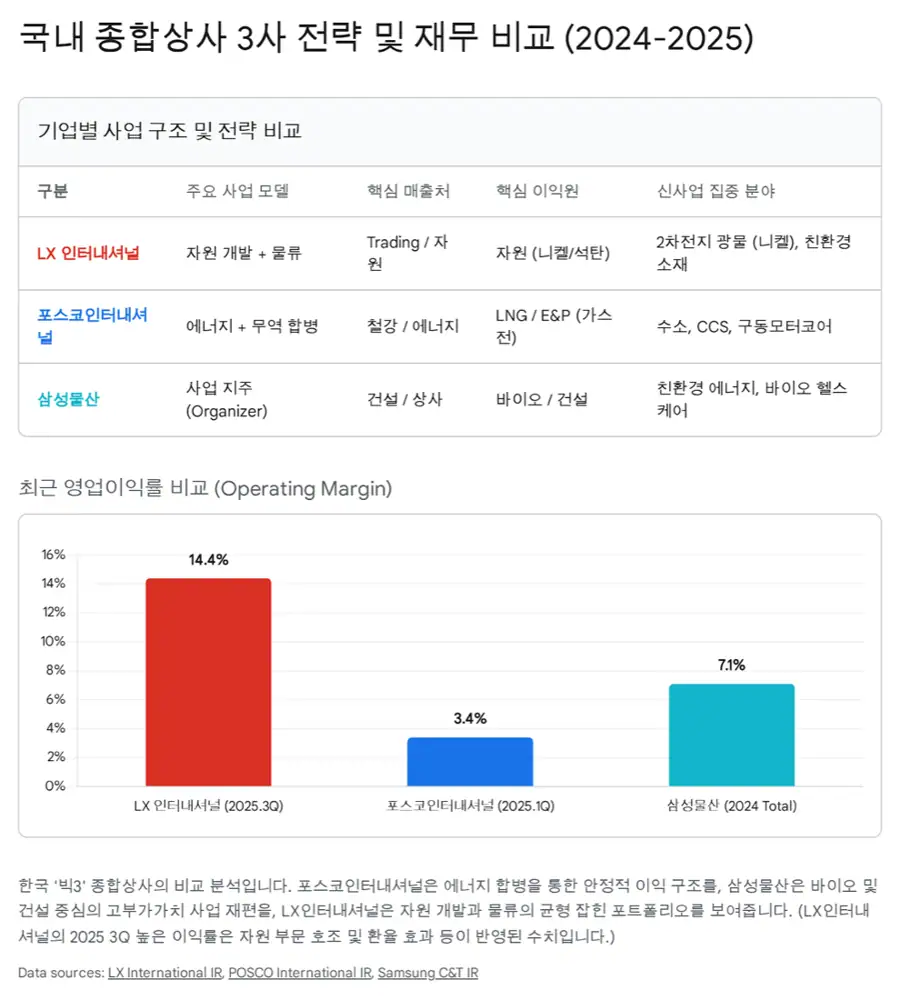

2. LX International: good cash flow, incomplete re-rating proof

Official fact: 3Q25 cumulative revenue is about KRW 12.3862tn. By segment, resources account for 7.3%, or about KRW 900.2bn; Trading/New Growth for 45.2%, or about KRW 5.6028tn; and logistics for 47.5%, or about KRW 5.8832tn.

| Segment | Source scale | Role | Key variable |

|---|---|---|---|

| Resources | 7.3%, about KRW 900.2bn | Low revenue share but high-margin cash cow | NEWC/ICI4 coal prices and nickel transition |

| Trading/New Growth | 45.2%, about KRW 5.6028tn | Resource trading, LCD panels, petrochemicals | Green materials and battery-material trading |

| Logistics | 47.5%, about KRW 5.8832tn | Stable cash flow centered on LX Pantos | SCFI decline and LG-family captive dependence |

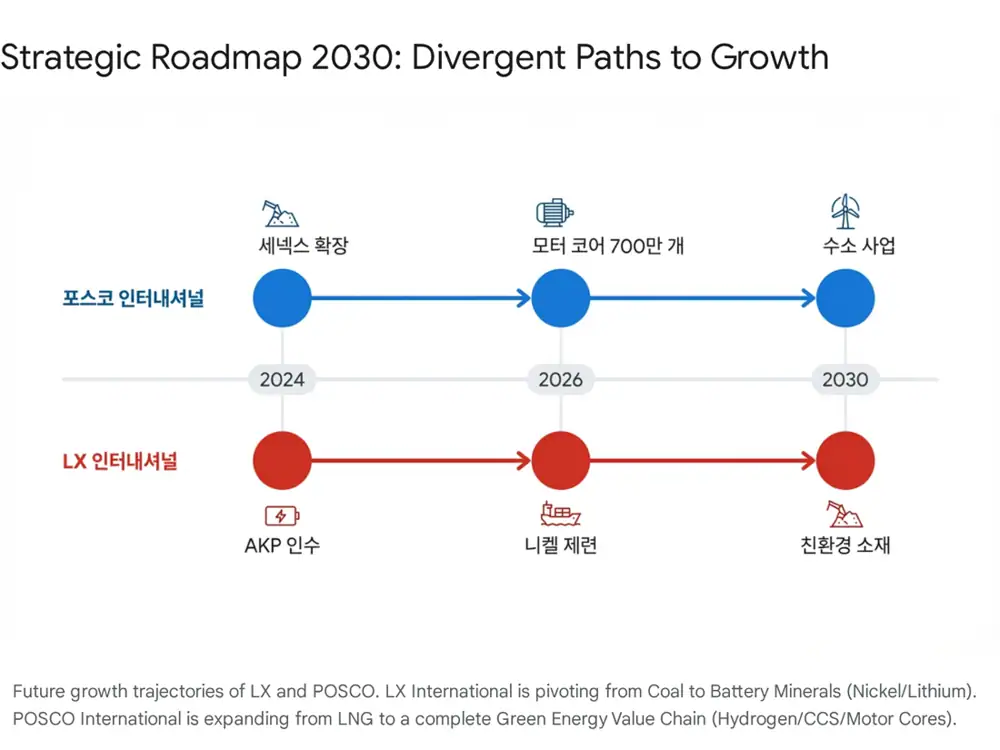

The decisive new business is Indonesia's AKP nickel mine. The source says LX acquired a 60% stake for KRW 133bn and gained control. The mine is near the Morowali Industrial Park on Sulawesi, with reserves of 36mn tonnes, enough for batteries for 7mn electric vehicles.

Interpretation: AKP is not just a thematic investment. It is the test case for LX to move beyond the image of a coal company and prove an operating value chain from mining to smelting, refining, and material trading.

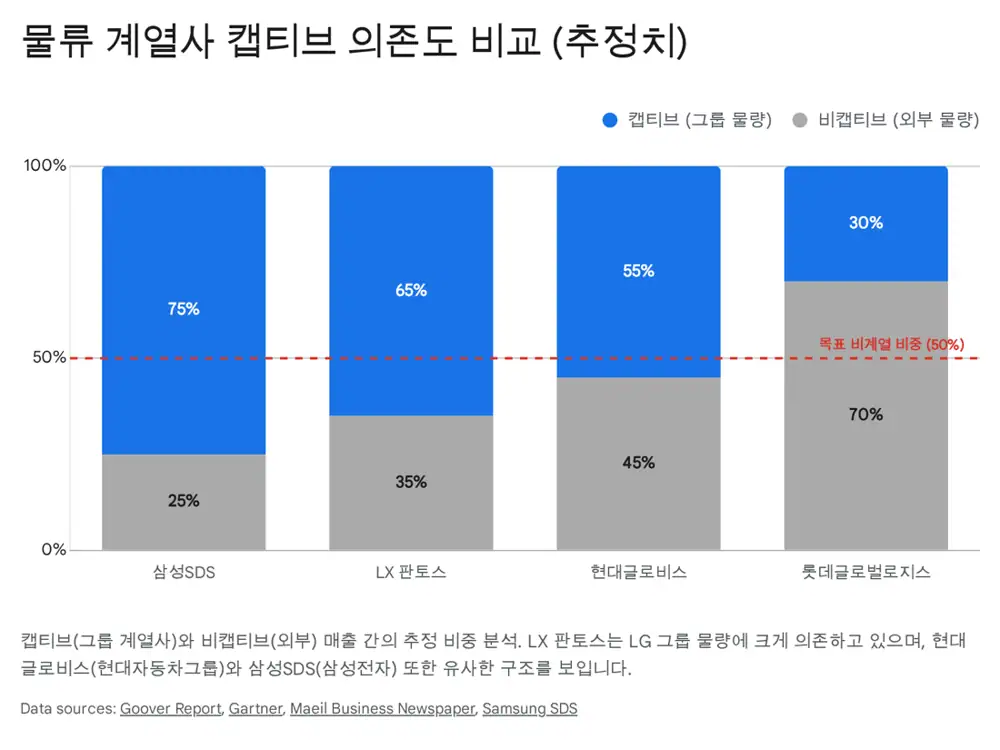

The risks remain. Resources are still sensitive to coal prices, and weak coal market conditions were cited as a cause of lower resource earnings in 3Q25. LX Pantos provides stable volume, but external estimates that roughly 60-70% of volume is captive LG-family freight make it harder for the market to value it as an independent logistics company.

3. Peer comparison: POSCO International and Samsung C&T

LNG value chain

Links Myanmar and Australian gas fields, the Gwangyang LNG terminal, and Incheon LNG power generation.

Group captive

Handles about 81% of POSCO Group steel exports and is expanding its battery-material procurement role.

Asset-light

Develops and sells solar, wind, and ESS projects rather than owning mines directly.

POSCO International created the most advanced Korean business-corporation model through the POSCO Energy merger. It owns the LNG chain and offsets low trading margins with high-margin energy profit, while the drive-motor-core business targets annual capacity of 7mn units by 2030.

Samsung C&T's trading arm relies less on heavy assets and more on Samsung's brand and financial network to originate renewable projects and sell project rights to financial investors. The source also says it is building solar and ESS pipelines in the U.S. and Australia, targeting more than 20GW of cumulative development capacity by 2025.

4. Lessons from Japanese trading houses and Korea's value-up pressure

Japanese trading houses are not merely equity investors. They send people into investees and lead management, establishing a business-management model. Warren Buffett's investment in them is tied to cash generation, portfolio stability, share buybacks, cancellations, and progressive dividends.

| Company | Source PBR | Discount or premium logic |

|---|---|---|

| LX International | About 0.44x | Coal ESG discount, conservative shareholder returns, captive logistics |

| POSCO International | About 1.1x | Energy merger synergy and battery-material theme |

| Samsung C&T | About 0.61x | Holding-company discount and market-cap gap versus assets |

| Japanese sogo shosha | 1.5-2.3x | Non-resource diversification, ROE improvement, clear shareholder returns |

Interpretation: To close the valuation gap with Japanese peers, Korean trading houses need more than new-business announcements. They need measurable proof of capital efficiency, payout policy, and share cancellation.

5. My checkpoints

- Watch whether AKP operations and expansion into nickel smelting, refining, precursors, and cathode-material trading translate into real revenue and profit.

- LX Pantos needs to lower LG-family captive dependence and prove independent sales power in the global 3PL market.

- A high dividend is not enough. The source says LX maintains a 6-8% dividend yield, but the market wants stronger shareholder returns including buybacks and cancellations.

- POSCO International is clearly associated with LNG and motor cores, while Samsung C&T is clearly associated with renewable development. LX must show that coal-to-green is not a slogan but a change in the income statement.

Sources

- 원문 / Original: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224112199646

- LX인터내셔널 리서치 자료: https://www.bondweb.co.kr/_research/downloadPage.asp?number=875282&gn=1

- Korean trading companies enhance shareholder value through business transformations: https://biz.chosun.com/en/en-industry/2024/12/26/HAF66MNIVJGCNAMIE4MGGKOB5A/

- Japanese trading companies guide: https://japan-dev.com/blog/japanese-trading-companies

- ITOCHU financial highlights: https://www.itochu.co.jp/en/ir/finance/highlights/index.html

- LX International 2025 Sustainability Report: https://www.lxinternational.com/asset/files/eng_report_2024-2025.pdf

- POSCO International 4Q24 earnings release: https://poscointl.com/upload/file/202502/20250203ANGmT5qh5ti.pdf

- Samsung C&T solar development article: https://dealsite.co.kr/articles/118695

- LX International AKP nickel mine press release: https://www.lxinternational.com/en/news/press_view?seq=434

- KED Global AKP nickel mine article: https://www.kedglobal.com/batteries/newsView/ked202311070013

- Indonesia Miner LX nickel and copper mines article: https://indonesiaminer.com/news/detail/2025-02-10154650-lx-international-seeks-to-acquire-nickel-copper-mines-in-indonesia

- MK AKP mine visit article: https://www.mk.co.kr/en/business/11026096

- Introducing LX International: http://www.lxinternational.com/asset/files/Introducing_LX_International_ENG%282507%29.pdf

- LX International captive risk analysis: https://seo.goover.ai/report/202503/go-public-report-ko-615166aa-e374-4505-b64f-a8eaa298a5de-0-0.html

- POSCO International merger and growth article: https://newsroom.posco.com/en/posco-international-accelerating-growth-through-investment-marking-2nd-year-since-merger-with-posco-energy/

- S&P Global POSCO International rating: https://www.spglobal.com/ratings/en/regulatory/article/-/view/sourceId/13230533

- MK POSCO overseas sales article: https://www.mk.co.kr/en/business/10979141

- Korea Times POSCO International and Samsung C&T portfolios: https://www.koreatimes.co.kr/business/companies/20240116/posco-international-samsung-ct-to-continue-hot-streak-in-2024-with-diversified-portfolios

- Samsung Electronics 3Q25 results: https://news.samsung.com/global/samsung-electronics-announces-third-quarter-2025-results

- Samsung C&T trading energy business: https://trading.samsungcnt.com/business/energy.do

- Hennessy Funds Mitsubishi Corporation spotlight: https://www.hennessyfunds.com/insights/company-spotlight-japan-fund-mitsubishi-corp

- Mitsubishi Corporation value creation story: https://www.mitsubishicorp.com/jp/en/ir/library/ar/pdf/areport/2022/02.pdf

- ITOCHU latest financial highlights: https://www.itochu.co.jp/en/ir/finance/review/index.html

- S&P Global Hyundai Glovis rating: https://www.spglobal.com/ratings/en/regulatory/article/-/view/sourceId/101614294

- Samsung SDS 2024 financial results: https://www.samsungsds.com/en/news/2024results-250124.html

- Judal LX International analysis: https://www.judal.co.kr/?view=stockAI&shareToken=LlhDX5kQNxgxuCQQ

- Eugene Investment LX International report: https://www.eugenefn.com/common/files/amail/20251106_001120_tjdgus2009_868.pdf