DEEP RESEARCH · LX INTERNATIONAL

LX International: Portfolio Shift from Old Energy to Green Materials

An investment frame combining coal/logistics cash flow with the Indonesian nickel growth option

0. Bottom line first

I view LX International as a transition company layering nickel and copper green-material options on top of older coal and logistics cash flows. A P/B around 0.4x and 6-7% dividend yield provide margin of safety, but Indonesian regulation and nickel oversupply must be watched together.

Official fact: The source presents LX International’s current valuation at about 0.4x P/B and says 2026 expected valuation is about 5.4-6.0x P/E and 0.3-0.4x P/B.

Interpretation: The market appears to be heavily discounting stranded-asset risk in coal while not fully pricing nickel growth. But re-rating becomes more convincing only when AKP nickel mine volume growth and logistics margin stabilization show up in numbers.

1. Portfolio transition

LX International started as Lucky-Goldstar Trading, but the source argues it should now be read more as an investment holding company than a simple trading house. The core moats are ownership-based resource development capability and a captive logistics network.

Ownership-based operator

Rather than merely brokering, LX can manage volume and cost through mine ownership and operating capability.

Captive logistics network

LX Pantos provides bargaining power in global logistics and stability from group cargo.

Information advantage

Information from resource development and logistics can feed trading expertise.

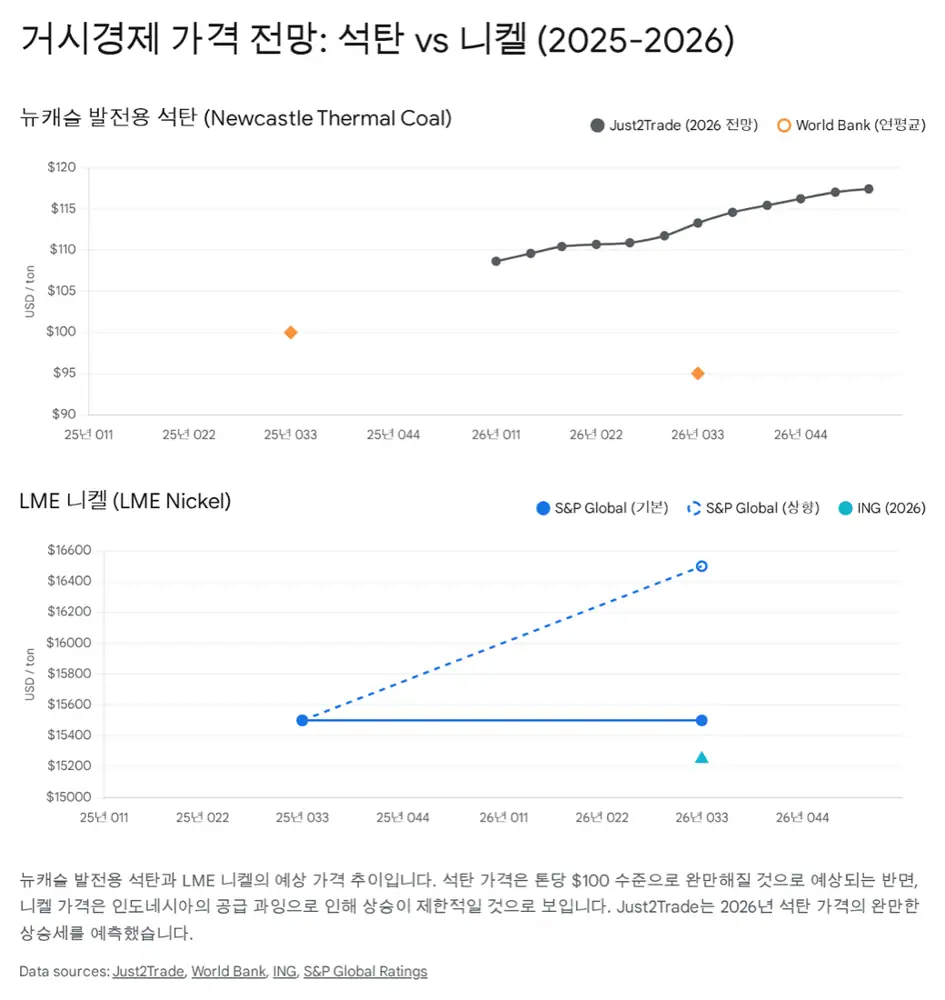

2. End markets: coal, nickel, logistics

The coal market is framed as managed decline: prices have normalized after the pandemic and energy crisis, but coal remains a cash-flow base. Nickel has a collision between long-term EV battery demand and short-term Indonesian oversupply.

| Market | Source view | Investment meaning |

|---|---|---|

| Coal | Downward stabilization | Cash generation and dividend funding, not growth |

| Nickel | Indonesian oversupply versus long-term battery demand | Volume, regulation, and cost control matter more than price alone |

| Logistics | End of pandemic boom and freight-rate normalization | Margin stabilization is a key variable for 2026 earnings recovery |

3. Q, P, C framework

Volume expansion

In commodities without strong pricing power, the company defends total profit by increasing production volume.

Price decline and base effect

Coal and nickel price corrections are a burden, but a lower base can make recovery rates look stronger.

Cost and efficiency

For both resources and logistics, variable-cost management and efficiency drive earnings leverage.

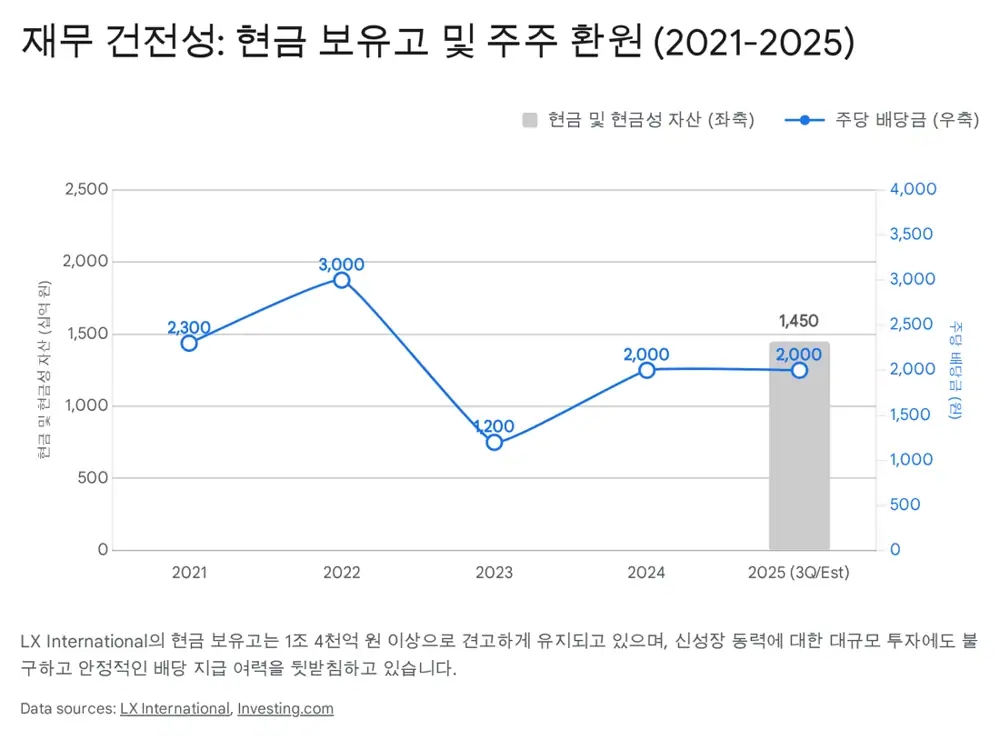

4. Financial health and capital allocation

Official fact: At the end of 3Q25, the source lists cash and cash equivalents at about KRW 1.45 trillion. Debt-to-equity is about 169%, and net debt ratio is about 34%.

Interpretation: Debt ratio alone may look high, but the source views it as healthy considering trading-finance liabilities in a general trading company. It also argues that LX still has additional M&A capacity after the roughly KRW 133 billion AKP mine acquisition.

Capital allocation is clearly moving toward green minerals. The source frames the AKP mine acquisition as a starting point and also mentions possible additional nickel and copper mine acquisitions in Indonesia, plus asset recycling such as reviewing the sale of the Pocheon Green Power stake.

5. Dividends and valuation

| Item | Source figure | Meaning |

|---|---|---|

| 2023 dividend | KRW 1,200 per share | Earnings-linked dividend history |

| 2024 dividend | KRW 2,000 per share | Payout ratio around 30-40% |

| 2025-2026 outlook | KRW 2,000 per share may be maintained | More than 6% yield at a low-KRW-30,000s share price |

| 2026E P/E | About 5.4-6.0x | Possible underpricing of future growth |

| 2026E P/B | 0.3-0.4x | Undervaluation relative to asset value |

The source contrasts this with POSCO International trading around 1.4x P/B and 18x P/E on expectations for entry into the secondary-battery materials value chain, and argues the gap is excessive.

6. 2026 outlook and risks

Official fact: Combining market consensus and industry analysis, the source presents 2026 operating profit at about KRW 485-496 billion, up more than 50% from the low-KRW-300 billion expected level for 2025.

- Growth drivers: AKP nickel mine volume growth and logistics profitability stabilization.

- Policy variable: stabilization of Indonesia’s RKAB quota approvals.

- Risks: export taxes, quota limits, and other Indonesian nickel regulations.

- Macro risk: lower cargo volume and weaker energy demand under global recession.

Interpretation: The source presents a BUY view, but I treat that as a research view rather than a recommendation: re-rating potential exists if portfolio transition and 2026 earnings normalization are verified.

Sources

- Original post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224111728932

- LX International to Acquire an Indonesian Nickel Mine: https://www.lxinternational.com/en/news/press_view?seq=434

- LX인터내셔널: https://www.bondweb.co.kr/_research/downloadPage.asp?number=875282&gn=1

- LX International company introduction: http://www.lxinternational.com/asset/files/Introducing_LX_International_ENG(2507).pdf

- Coal Price Forecast 2025, 2026-2030: https://j2t.com/solutions/blogview/coal-price-prediction/

- World Bank coal decline article: https://blogs.worldbank.org/en/opendata/weakening-demand--steady-supply--what-s-driving-coal-s-decline-i

- Coface nickel outlook: https://www.coface.com/news-economy-and-insights/nickel-has-a-future-despite-low-prices

- Petromindo nickel surplus through 2026: https://www.petromindo.com/news/article/nickel-market-set-to-remain-in-surplus-through-2026-ing

- ING Think nickel still capped by surplus: https://think.ing.com/articles/nickel-still-capped-by-surplus/

- S&P Global Ratings metal price assumptions: https://www.spglobal.com/ratings/en/regulatory/article/-/view/sourceId/101650666

- Argus Indonesian nickel permits: https://www.argusmedia.com/ja/news-and-insights/latest-market-news/2739547-indonesian-nickel-firms-to-re-apply-for-2026-27-permits

- Mysteel Indonesia nickel quotas: https://www.mysteel.net/news/5104082-flash-indonesia-to-adjust-nickel-supply-quotas-in-2026

- Xeneta 2026 ocean freight tenders: https://www.xeneta.com/blog/october-spot-rate-spike-2026-ocean-freight-tenders

- Drewry World Container Index: https://www.drewry.co.uk/supply-chain-advisors/supply-chain-expertise/world-container-index-assessed-by-drewry

- Drewry 2026 ocean contracts: https://www.drewry.co.uk/news/news/shippers-in-the-driving-seat-to-secure-better-2026-ocean-contracts-after-reversal-of-trend

- Indonesia Miner LX nickel/copper mines: https://indonesiaminer.com/news/detail/2025-02-10154650-lx-international-seeks-to-acquire-nickel-copper-mines-in-indonesia

- 프라임경제 LX인터내셔널: https://m.newsprime.co.kr/section_view.html?no=668014

- LX International financial information: https://www.lxinternational.com/en/investment/balance_sheet

- Investing.com LX International dividends: https://www.investing.com/equities/lg-international-corp-dividends

- LX International stock information: https://www.lxinternational.com/en/investment/stock

- LX Holdings press release: https://www.lxholdings.co.kr/en/news.do

- 유진투자증권 LX인터내셔널: https://www.eugenefn.com/common/files/amail/20251106_001120_tjdgus2009_868.pdf

- 뉴스핌 리포트 브리핑: https://www.newspim.com/news/view/20251106000069

- FnGuide LX인터내셔널 경쟁사비교: https://wcomp.fnguide.com/CompanyInfo/Comparison?cmp_cd=001120