DEEP RESEARCH · HVM

HVM: Advanced Metals Platform for the Space and Aerospace Era

A look at vacuum melting, the Seosan second plant, space revenue mix, and the earnings turnaround

0. Bottom line first

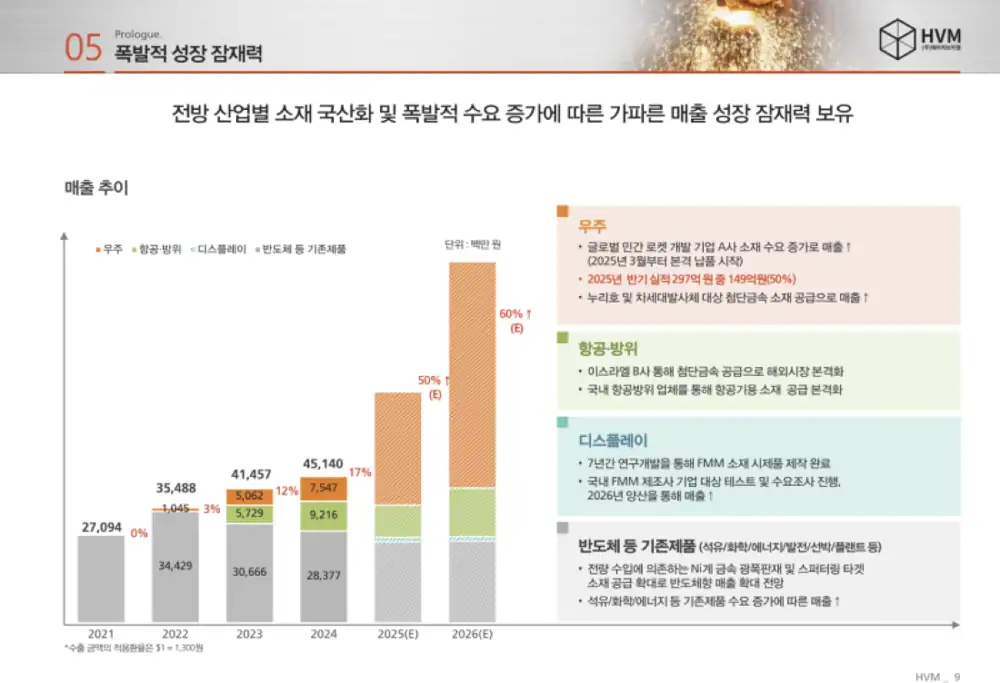

HVM should be read not as a simple metal processor but as an advanced-materials company making high-purity metals for extreme environments. The source points to 2025 Q3 cumulative revenue of KRW 43.1 billion, operating profit of KRW 4.6 billion, and space revenue above 50% as evidence that the business mix transition is now visible in numbers.

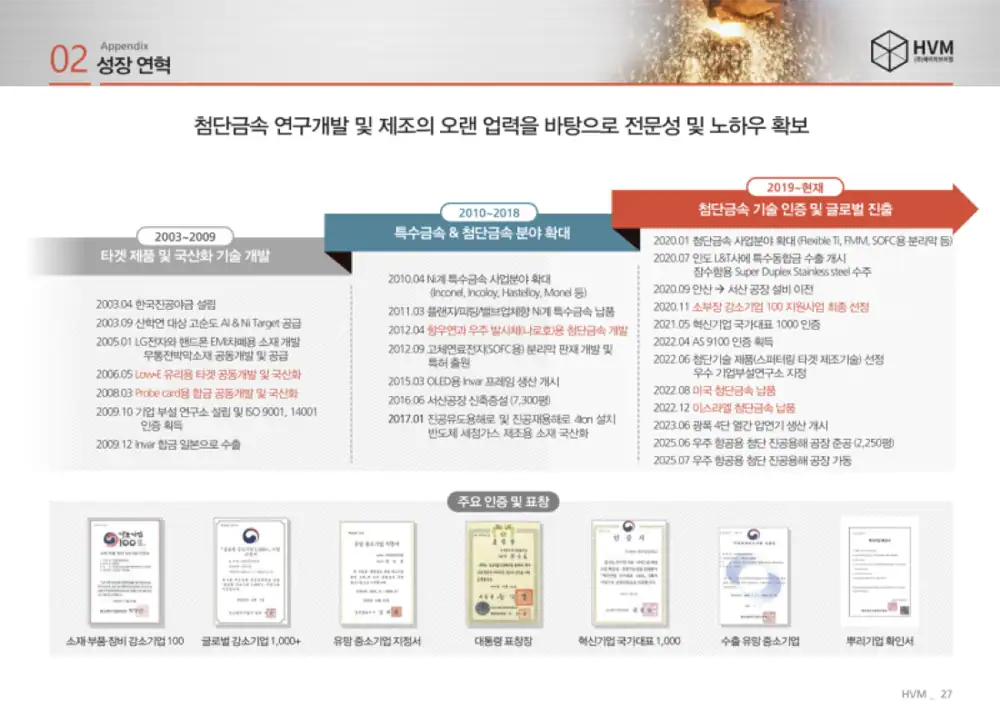

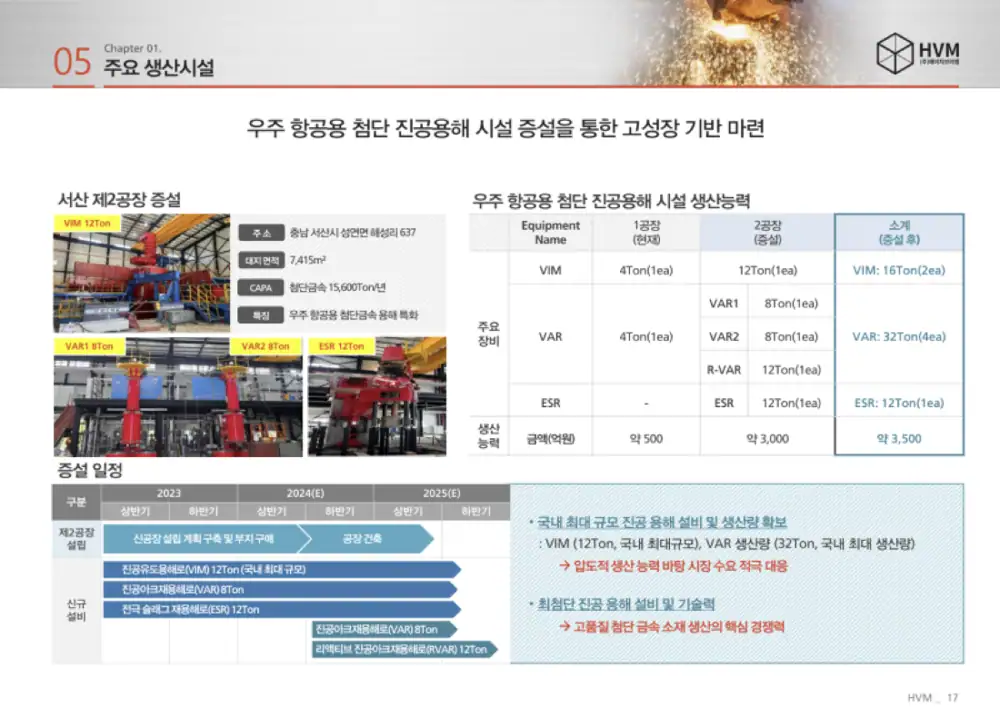

Official fact: The source reports 2025 Q3 cumulative revenue of KRW 43.1 billion, operating profit of KRW 4.6 billion, operating margin of 10.7%, and net income of KRW 2.794 billion. The Seosan second plant was completed in June 2025 with 12-ton VIM and large VAR equipment.

Interpretation: The core is not just localization of materials, but customer validation and capacity. If the global private-space customer reference and second-plant utilization both scale, a higher multiple than traditional metals can be argued.

1. Source images and company position

All source images are preserved. The charts and reference images should be read as supporting material for the source figures.

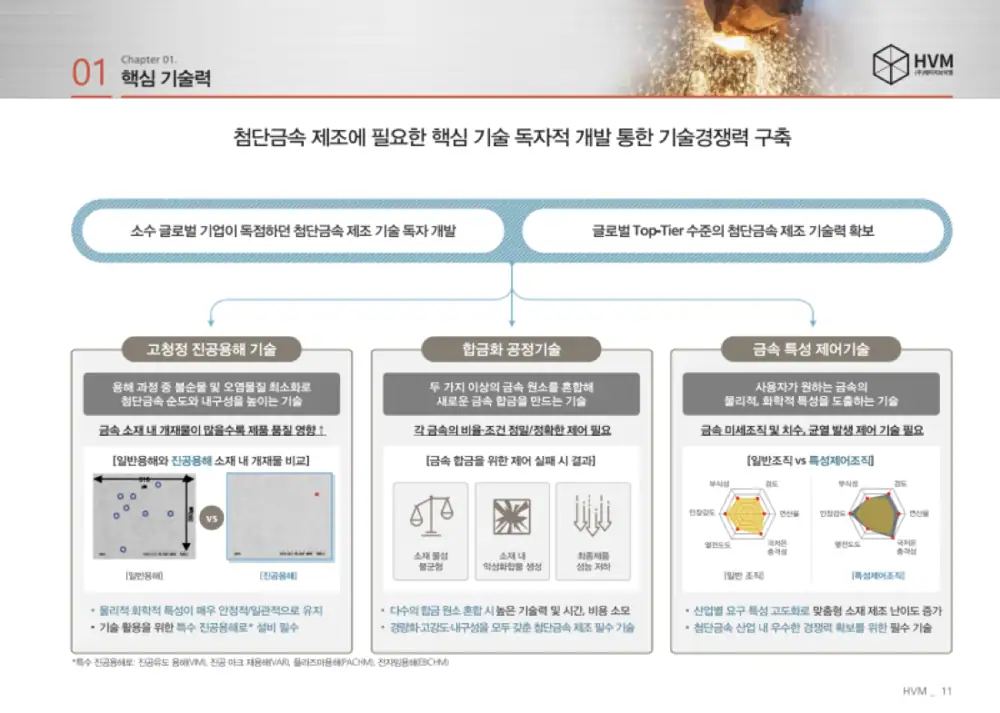

2. Technology: high-purity vacuum melting is the core

| Technology | Process feature | Strategic meaning |

|---|---|---|

| VIM | High-vacuum electromagnetic induction melting | Controls oxygen, nitrogen, hydrogen, and other impurities; 12-ton equipment supports large ingots |

| VAR | Vacuum arc remelting of electrodes | Improves homogeneity for space engines and aircraft turbines |

| ESR | Refining through a slag layer | Removes nonmetallic inclusions such as sulfur and improves surface quality |

| PACHM | Plasma arc and cold hearth | Titanium scrap recycling and cost competitiveness |

| EBCHM | Electron-beam ultra-high-vacuum melting | Development of refractory metals such as tantalum, niobium, and tungsten |

The source lists 18 domestic patents plus overseas patents and highlights hybrid melting for iron-nickel alloys, titanium electrode briquettes, high-purity silver sputtering targets, plasma torch technology, and variable molds as key IP.

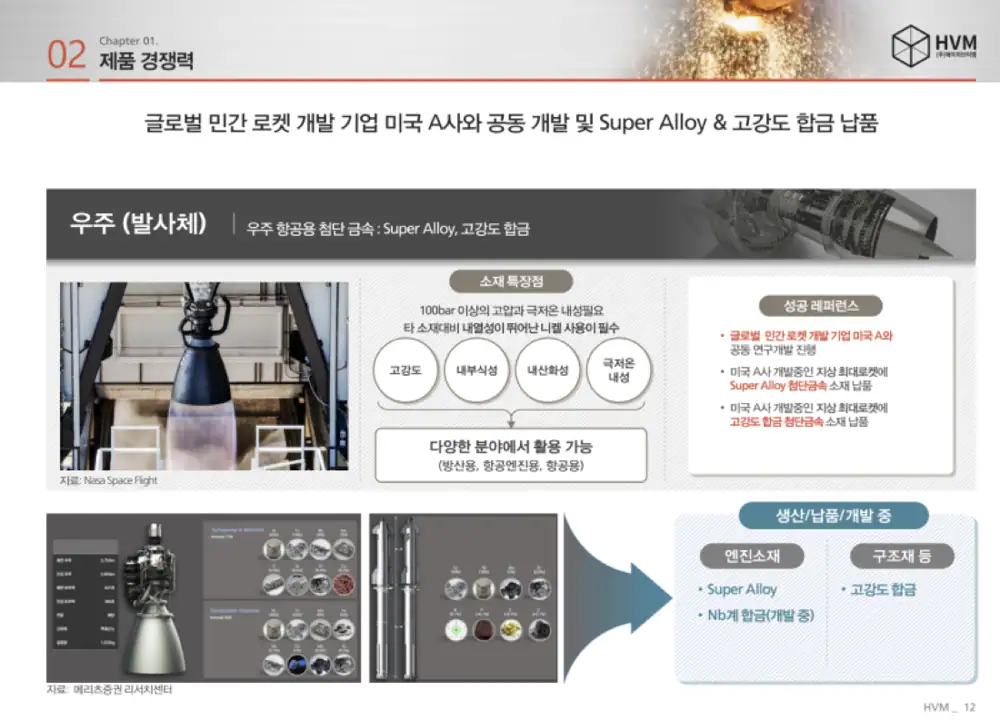

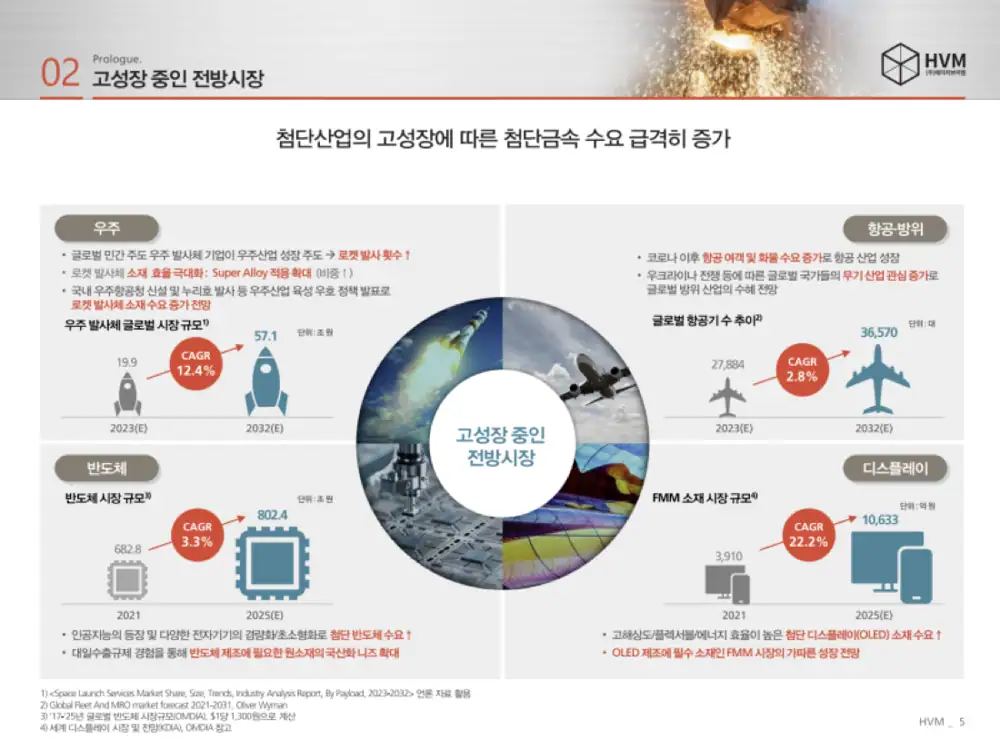

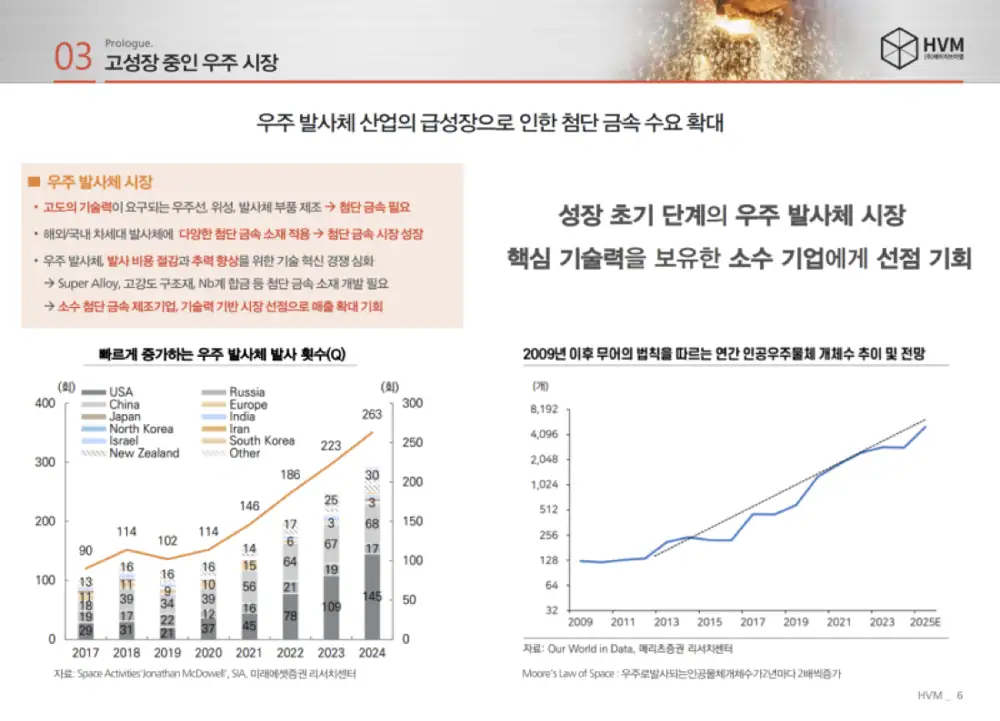

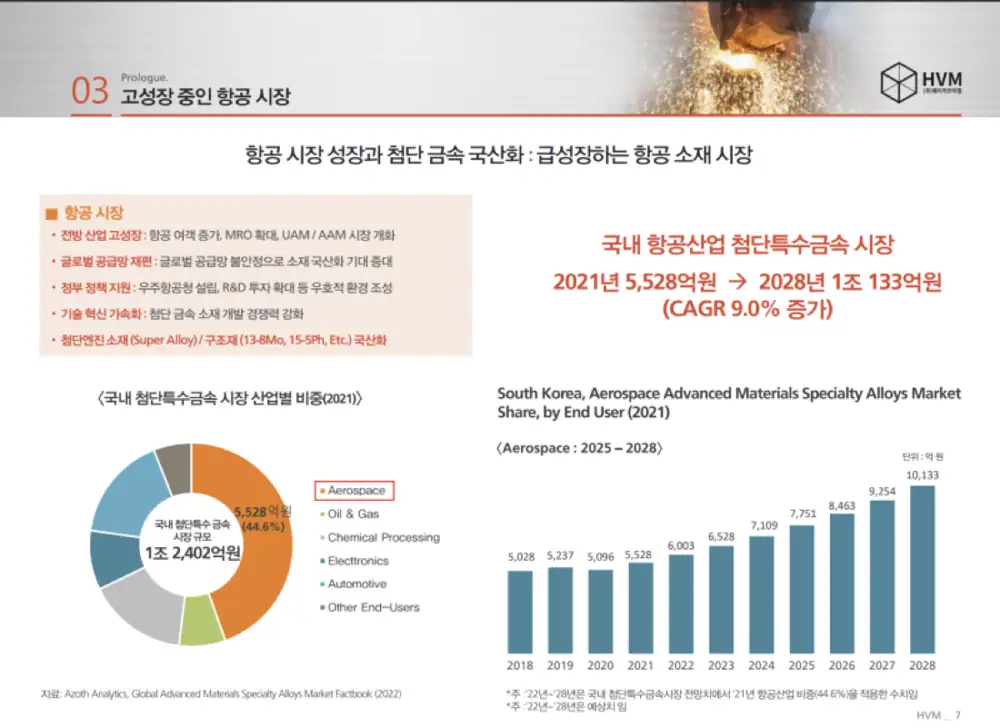

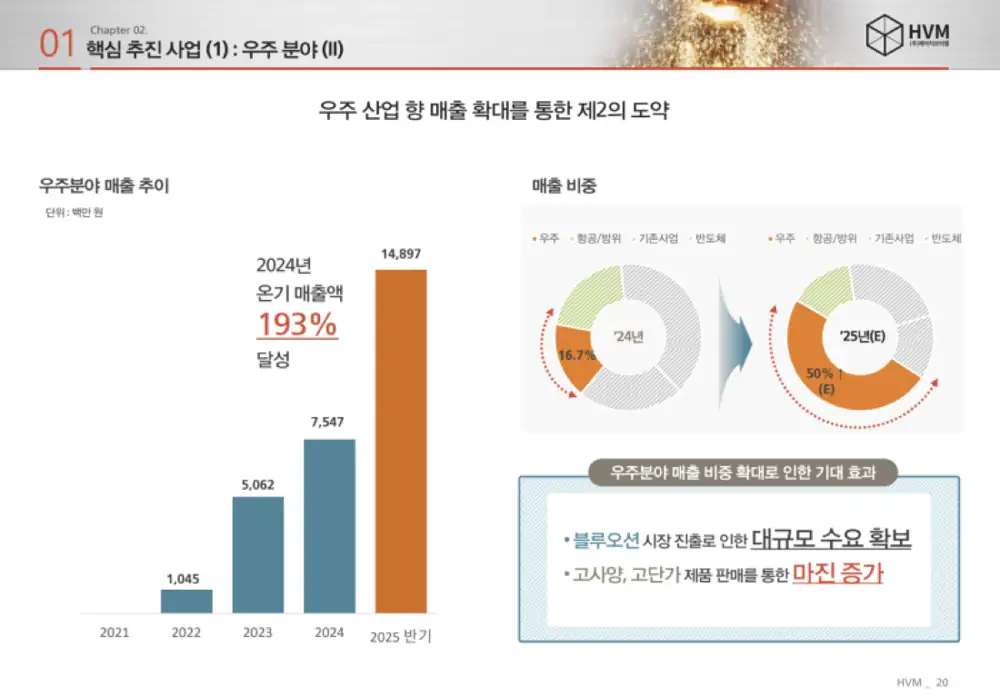

3. Business segments: space becomes the core

About KRW 24.1B

About 56% of 2025 Q3 cumulative revenue. Key products include nickel superalloys, copper alloys, and high-strength stainless steels.

About KRW 5.9B

Titanium alloys and superalloys can benefit from friend-shoring.

About KRW 6.2B

Corrosion- and heat-resistant alloys for petrochemical, plant, and power applications provide stable cash generation.

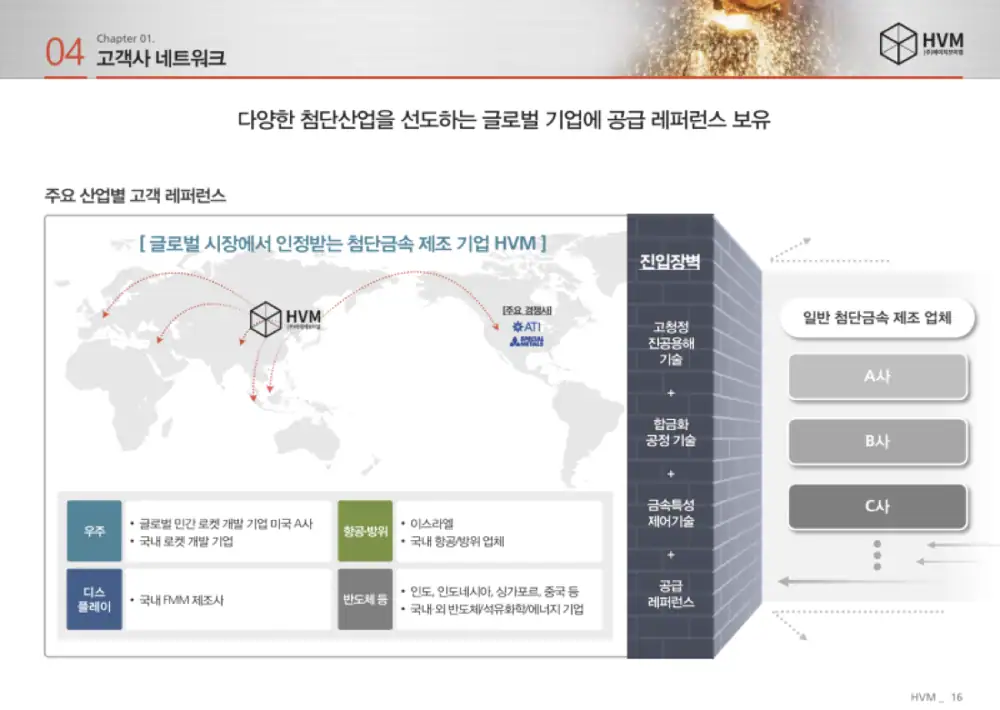

- The partnership with global private space company A is interpreted as a technology-validation reference.

- Post Russia-Ukraine titanium supply-chain instability increases the opportunity for Korean suppliers.

- Sputtering targets and Super Invar alloy for FMM are localization options for semiconductor and display materials.

4. Second plant and financial turnaround

| Item | 2025 Q3 cumulative | 2024 Q3 cumulative | YoY |

|---|---|---|---|

| Revenue | KRW 43,105M | KRW 32,853M | +31.2% |

| Gross profit | KRW 9,117M | KRW 5,843M | +56.0% |

| Operating profit | KRW 4,599M | KRW 1,587M | +189.8% |

| Operating margin | 10.7% | 4.8% | +5.9%p |

| Net income | KRW 2,794M | KRW 440M | +535.0% |

Official fact: The source cites total assets of KRW 168.4 billion, liabilities of KRW 86.3 billion, equity of KRW 82.1 billion, debt ratio of about 105%, current ratio of about 143%, and cash plus short-term financial instruments of about KRW 30.3 billion.

Interpretation: Early second-plant operation can show depreciation and inventory burden, but as utilization rises fixed-cost leverage can improve margins.

5. Risks and checkpoints

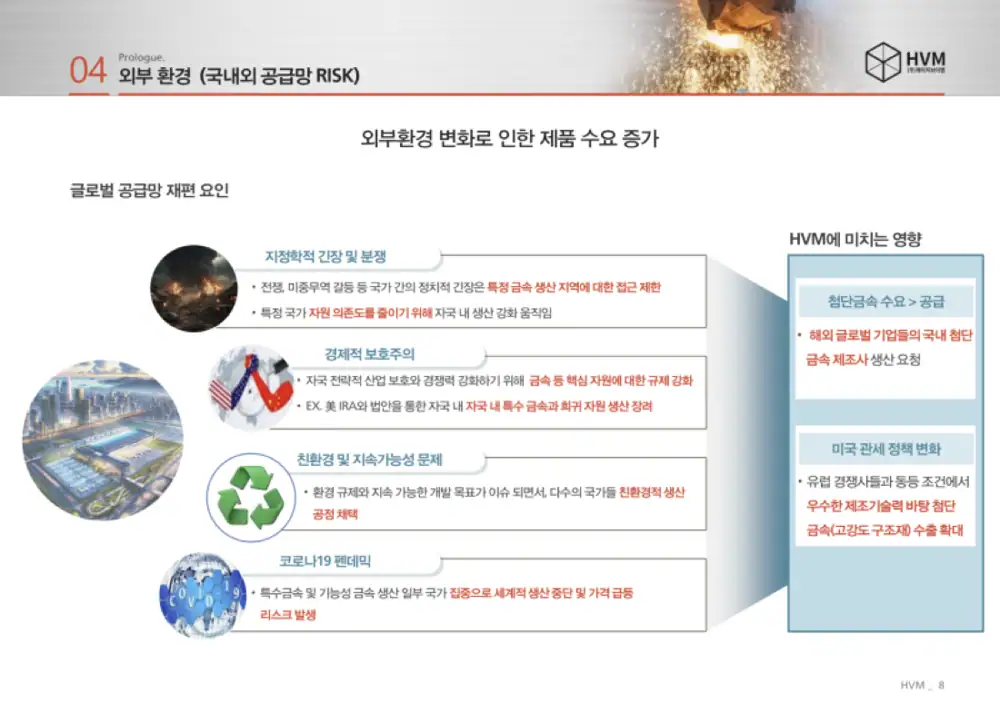

- Nickel, titanium, and copper price volatility directly affects cost ratio. The source presents surcharge systems and scrap recycling as mitigants.

- Heavy space revenue dependence on global company A may create customer concentration risk.

- About KRW 30.2 billion of convertible bonds can improve the balance sheet when converted, but also dilute shareholders.

- Watch whether 5-inch-plus titanium billets, refractory metals, and 3D-printing powders convert into mass-production revenue.