DEEP RESEARCH · ADTECHNOLOGY

ADTechnology and Siemens: Strategic Meaning of the ASIC Development Contract

Why a 2023 contract was disclosed in November 2025, and what it could mean for backlog and mass-production revenue.

0. Bottom line first

My read is that this was not simply a late disclosure. The source argues that the development scope expanded, the contract value increased, and the deal crossed the mandatory disclosure threshold. That points to project scale-up after technical validation.

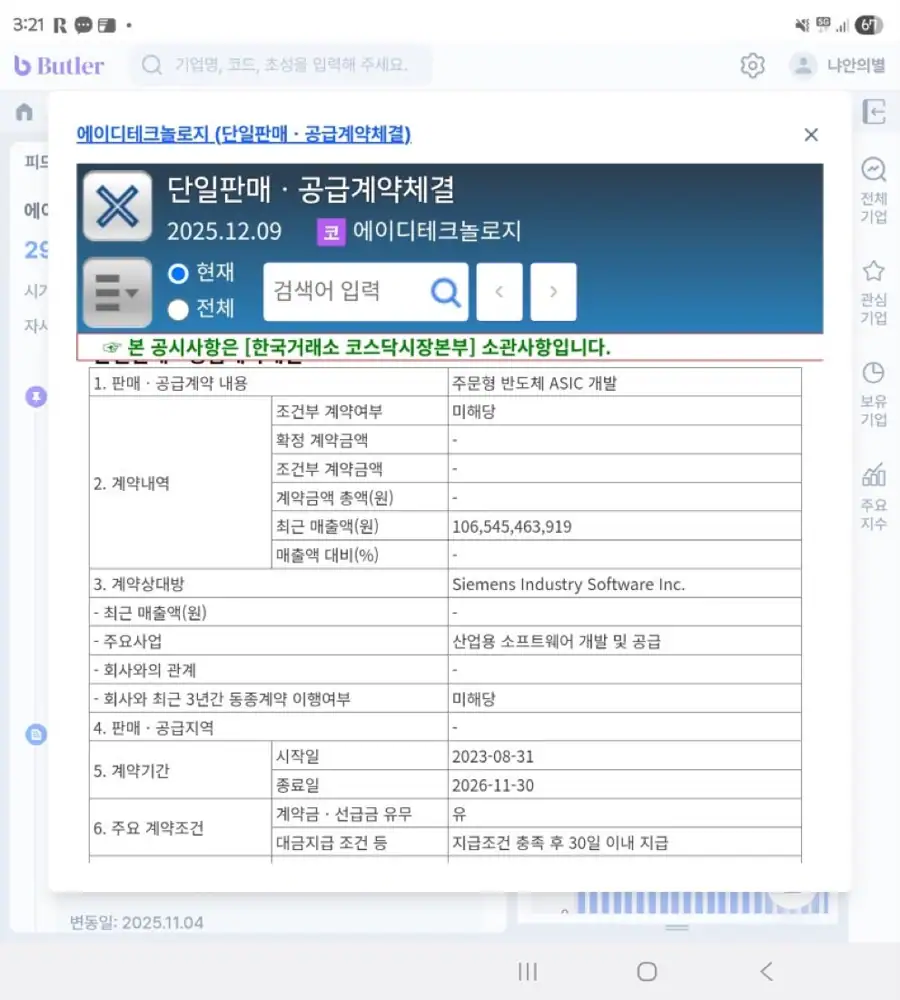

Official fact: Based on the disclosure image, the counterparty is Siemens Industry Software Inc., the contract scope is ASIC development, and the contract period runs from August 31, 2023 to November 30, 2026, or 39 months.

Interpretation: Using ADTechnology's 2024 consolidated sales of about KRW 106.5bn, the 10% single-sales/supply disclosure threshold is about KRW 10.6bn. The source reconstructs the event as a scope change that pushed the total contract value above the threshold.

1. Disclosure facts and technical difficulty

- Counterparty: Siemens Industry Software Inc., the digital-industry software arm including former Mentor Graphics.

- Contract type: ASIC development, or NRE.

- Contract period: August 31, 2023 to November 30, 2026, totaling 39 months.

- Payment terms: the source assumes progress billing or milestone-based payments.

Compared with a typical 12-18 month legacy ASIC project, 39 months is long. The source reads this as evidence of advanced-node work, a complex industrial/communications SoC, and possibly a full-turnkey project including prototyping and long qualification.

2. Qualitative change in backlog

Higher conversion probability

A global enterprise like Siemens lowers project-cancellation risk and raises the probability that backlog converts into revenue.

Longer revenue base

A multi-year contract can lift the baseline for quarterly NRE revenue. The source connects it to a possible development-sales jump from KRW 31.6bn in 3Q to KRW 48.0bn in 4Q 2025.

Follow-on opportunity

Success could open doors to Siemens healthcare, mobility, and other group projects.

The source estimates ordinary 14nm industrial SoC full-turnkey NRE at KRW 10-20bn, and KRW 30-50bn when customized IP and long validation for a large customer are included. Its recognition scenario is KRW 3-5bn in 2023, KRW 9-15bn in 2024, KRW 12-20bn in 2025, and KRW 6-10bn in 2026.

3. Project lifecycle

| Period | Phase | Activities | Backlog recognition |

|---|---|---|---|

| 2023.08-2024.02 | Architecture definition | PPA targets, Samsung 14nm PDK review, key IP selection | Initial payment recognized |

| 2024.03-2025.06 | RTL design and verification | Logic design, functional verification, emulation | Progress billing |

| 2025.07-2025.12 | Physical implementation | Synthesis, P&R, timing closure | Peak revenue recognition |

| 2026.01-2026.06 | Tape-out and prototype | GDS delivery, MPW/shuttle prototype wafer | Milestone revenue |

| 2026.07-2026.11 | Qualification and MP sign-off | Packaging, board tests, reliability tests, mass-production contract | Development ends and mass-production backlog begins |

4. Why Siemens, and why ADTechnology

The source treats Siemens as a company with semiconductor DNA, not just software. Siemens was the parent of Infineon, and Siemens DISW includes Mentor Graphics, acquired in 2017. Mentor is described alongside Synopsys and Cadence as a top-three EDA player.

- Siemens Veloce hardware emulators use custom ASICs.

- Simatic PLCs and industrial IoT gateways require communications chips.

- The source frames Samsung Foundry as a possible second source amid TSMC bottlenecks and supply-chain diversification.

- ADTechnology is interpreted as a partner that can reduce physical-design risk through Samsung Foundry PDK expertise and about 800 design engineers.

5. Scale estimate and end-market scenarios

Interpretation: The following figures are source-side simulations reverse-engineered from industry norms and a 2026 estimate. Actual contract terms may differ.

| Item | Source assumption |

|---|---|

| Process | Samsung Foundry 14LPP |

| Wafer | 300mm, 12-inch |

| Die size | 100mm² assumed |

| Yield | 85% initial mass-production yield for a mature node |

| 2026 mass-production revenue | KRW 19.5bn estimated |

| Annual wafer starts | About 3,000 wafers, or 250 wafers per month |

| Total expected revenue | About KRW 175-200bn over seven years |

Industrial IoT or communication controller

The source sees this as the most likely scenario, tied to Simatic IoT gateways or Scalance industrial switches.

Hardware emulation

The chip could support the Veloce Hardware Emulator or related I/O control.

Medical equipment

Another scenario is an imaging signal-processing unit for Siemens Healthineers MRI or CT equipment.

6. Final monitoring points

- Watch whether revenue recognition accelerates during the 2H 2025 physical implementation phase.

- 2026 tape-out and prototype success are the bridge from development revenue to mass-production revenue.

- A 39-month project carries risks from specification changes, engineering hurdles, and schedule delays.

- A global manufacturing slowdown could reduce Siemens industrial-automation demand and mass-production volume.

7. Appendix: expected revenue-recognition model

| Year | Quarter | Milestone | Activity | Estimated recognized revenue | Note |

|---|---|---|---|---|---|

| 2023 | 3Q | Kick-off | Contract, spec finalization, team setup | KRW 1.0bn | Initial payment |

| 2023 | 4Q | Architecture | Architecture design and IP selection | KRW 2.0bn | - |

| 2024 | 1Q-2Q | Front-end design | RTL coding and functional verification | KRW 5.0bn | Engineering ramp starts |

| 2024 | 3Q-4Q | Verification | Simulation and emulation | KRW 8.0bn | - |

| 2025 | 1Q-2Q | Implementation | Synthesis and DFT insertion | KRW 10.0bn | - |

| 2025 | 3Q-4Q | Physical design | P&R and timing closure | KRW 15.0bn | Current peak period |

| 2026 | 1Q | Tape-out | Foundry data handoff | KRW 5.0bn | Milestone |

| 2026 | 2Q | Prototyping | Prototype wafer receipt and packaging | KRW 3.0bn | - |

| 2026 | 3Q | Qualification | Reliability and system tests | KRW 2.0bn | - |

| 2026 | 4Q | Mass production | MP start | +KRW 19.5bn/year | Development ends, MP revenue begins |

Sources

- Naver Blog source: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224103786705

- Industrial conglomerate report: https://drive.google.com/open?id=1iRp07Hbd0Y5dc03Ok--YZHOxsswF-9V7

- 2H 2025 IR book: https://drive.google.com/open?id=1bci3pfT3KszMV55MQ6Gey8z6XZcsbd26

- SEMIFIVE analysis and competitor comparison: https://drive.google.com/open?id=1ZJN7Vzr43WnJxxZuL3xaCwiivq0DgsU1fOAFhWTNo-U