DEEP RESEARCH · TAEWOONG/WIND VALUE CHAIN

Taewoong: Offshore Wind Upsizing and the Conditions for a Super Supplier

A review of the 15,000-ton press, Ø11,000mm ring-rolling investment, 53.8% wind revenue mix, and AMPC variables in tower manufacturing.

0. Bottom line first

Taewoong is not just a forging company. It is a materials and components supplier capable of making the ultra-large flanges and ring parts required by offshore wind turbine upsizing. The key source numbers are a 53.8% wind-equipment revenue share, a 15,000-ton press, and a KRW 45B investment to upgrade from Ø9,500mm to Ø11,000mm ring rolling.

Ultra-large equipment

The 15,000-ton press and Ø9,500mm ring-rolling mill are capital-intensive assets competitors cannot easily copy.

Offshore wind positioning

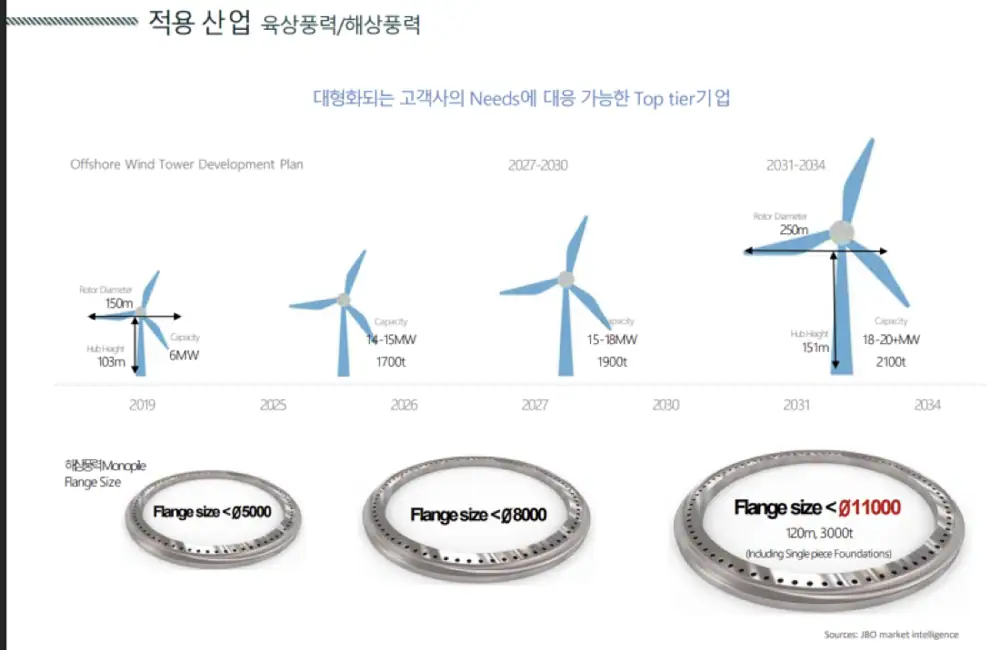

The Ø11,000mm ring-rolling upgrade targets the market for 15MW-class and larger offshore wind flanges.

Shift toward wind

Wind-equipment revenue share was 53.8% in Q3 2025, 9.1 percentage points higher than the 44.7% share in 2024.

1. Taewoong’s place in the supply chain

The wind industry is moving from onshore to offshore and from smaller turbines to 15MW and 20MW-class turbines. That shift increases both the size and strength requirements for towers, flanges, bearings, and shafts.

Official fact: The source uses the Q3 2025 quarterly report, Taewoong IR materials, and a CS Wind Q3 2025 analysis to compare Taewoong, the wind tower industry, and the market environment for Dongkuk S&C.

2. Manufacturing moat: open-die forging and vertical integration

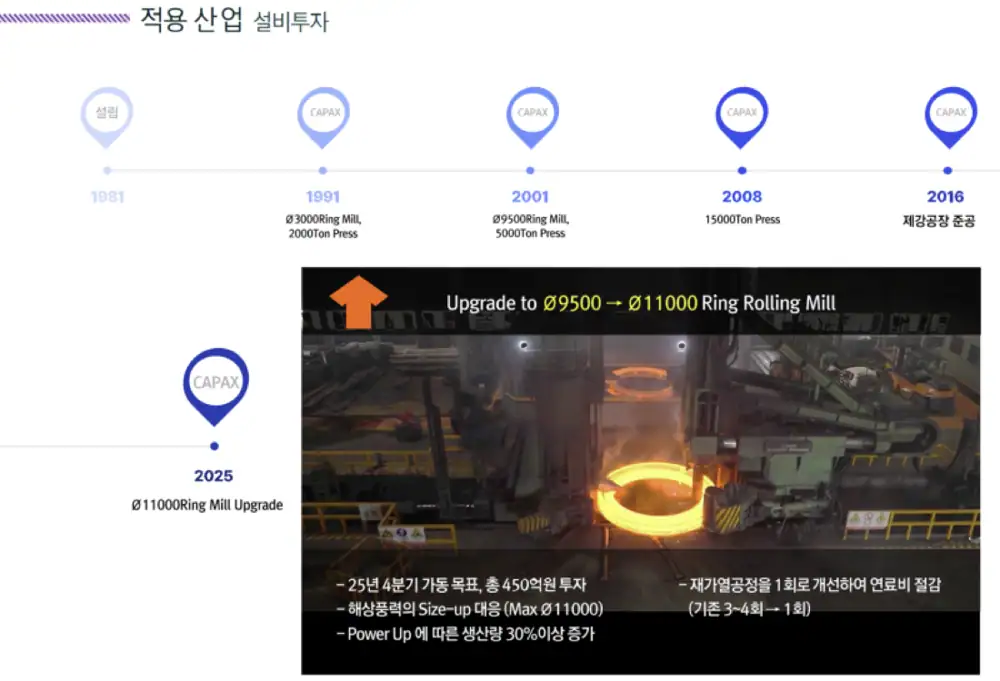

Taewoong began as Taewoong Forging in 1981 and has become a global materials specialist. It is focused on open-die forging and ring rolling, which makes seamless ring-shaped components.

Official fact: Taewoong owns a 15,000-ton ultra-large press and a Ø9,500mm ring-rolling mill. It is investing KRW 45B to upgrade to Ø11,000mm, which the source frames as an investment aimed at 15MW-class and larger offshore wind turbines.

Official fact: Taewoong completed its steelmaking plant in 2016, creating an integrated production system from electric-arc-furnace materials to forging.

- Cost competitiveness: more flexibility against raw-material price volatility and lower intermediate margins.

- Customized materials: production of forging-specific materials such as round bloom improves material loss and yield.

- Delivery and quality control: high-spec materials such as specialty steel can be developed and supplied quickly.

Interpretation: Vertical integration from steelmaking to ring rolling is not just a cost project. In offshore wind parts, it is a strategic asset for controlling delivery and quality.

3. Revenue mix: wind rises and local export matters

Taewoong has a diversified heavy-industry portfolio across wind, shipbuilding, industrial machinery, and plants, but recent data shows a clear shift toward wind.

| Industry | 2024 revenue/share | Q3 2025 revenue/share | Change | Interpretation |

|---|---|---|---|---|

| Wind equipment | KRW 172,546M / 44.7% | KRW 46,487M / 53.8% | +9.1%p | Sharp increase in offshore wind large-flange demand |

| Shipbuilding & marine engines | KRW 62,570M / 16.2% | KRW 14,302M / 16.5% | +0.3%p | Strength in LNG and other eco-ship orders |

| Industrial machinery | KRW 61,742M / 15.9% | KRW 12,864M / 14.9% | -1.0%p | Delayed global capex |

| Industrial plant | KRW 55,929M / 14.5% | KRW 6,878M / 8.0% | -6.5%p | Weak traditional chemical-plant investment |

| Power generation | KRW 14,254M / 3.7% | KRW 2,270M / 2.6% | -1.1%p | Waiting for SMR and next-gen nuclear markets |

Official fact: The source notes that the Q3 2025 sales figures are quarterly, three-month figures, while the share trend is consistent with cumulative data.

Exact onshore/offshore revenue splits are not disclosed in the financial statement notes. The source’s view is that onshore wind led growth from 2008 to 2017 with 2~3MW turbines, while offshore wind has become the main driver since 2018 as turbine capacity moved above 10MW toward 15MW and 20MW.

| Region | 2024 share | Q3 2025 share | Analysis |

|---|---|---|---|

| Domestic | 52.9% | 50.3% | Includes local production-base customers such as Doosan Enerbility, CS Bearing, and Korean shipbuilders |

| Europe | 14.9% | 20.5% | Exports to offshore-wind leaders such as Vestas and Siemens Gamesa expanded |

| Asia | 19.6% | 18.0% | China and Southeast Asia infrastructure demand |

| America | 12.6% | 11.2% | GE Vernova supply and onshore wind demand |

Interpretation: The 50.3% domestic share is not pure domestic demand. It includes “local export” to global companies with Korean production bases. The source estimates that end-user overseas exposure could approach 80~90%.

4. Wind tower industry and the AMPC variable

Wind tower companies such as Dongkuk S&C receive flanges from forging companies like Taewoong and steel plates from steelmakers, then use roll bending and welding to make towers. Because the source lacks Dongkuk S&C standalone data, it uses CS Wind’s Q3 2025 results as a proxy.

Official fact: AMPC, the advanced manufacturing production credit under the US IRA, has a major impact on tower manufacturers’ profit structure. In CS Wind’s case, the source states that AMPC subsidies were the key reason operating profit surprised despite weaker-than-expected revenue.

- AMPC means US production capacity and policy benefit eligibility become key valuation criteria.

- Offshore wind towers have large project size and long construction periods, making quarterly revenue sensitive to delivery timing and percentage-of-completion recognition.

- Onshore wind is a mature, competitive market, while offshore wind requires structures over 100 meters high and hundreds of tons in weight, raising the importance of welding, coating, and port access.

5. Comparing Taewoong with tower makers, and the conclusion

| Comparison item | Taewoong | Tower makers such as Dongkuk S&C |

|---|---|---|

| Core asset | Ultra-large press and ring-rolling mill | Welding equipment, yards, port access |

| Entry barrier | Very high due to heavy upfront capex | Medium; logistics barrier exceeds pure technology barrier |

| Logistics sensitivity | Low; components are easier to export | Very high; large volume makes shipping expensive |

| Main risks | Scrap and alloy-steel input prices | Anti-dumping duties and steel-plate prices |

| Benefit points | Turbine upsizing and higher component ASP | US IRA/AMPC and offshore wind expansion |

Interpretation: Taewoong bears high depreciation once equipment is installed, but the equipment itself is the entry barrier. Tower makers, by contrast, depend more on local production bases and policy benefits because their products are bulky.

Metrics I would watch

- Start-up of the new Ø11,000mm equipment at end-2025 and capacity expansion effects in 2026

- New orders and utilization for large offshore-wind flanges

- For tower makers including Dongkuk S&C, IRA continuity and actual offshore project delivery schedules

Overall, Taewoong is aiming to become a super supplier for the offshore wind era through material self-sufficiency and ultra-large ring-rolling investment. Tower makers have AMPC tailwinds, but project lumpiness and trade barriers must be watched together.

Sources

- Original Naver Blog post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224100954856

- Attached Taewoong IR 25.2Q Korean PDF: https://download.blog.naver.com/open/fa6fe653407170c4ef016f596385f985257389c6/EFsQaLZIxb3O89I2E-QRigSVEg-Y7dtnemsQLWUj_gMvH4-7UXsi7_i_C4AO_V1b-E3xbkf77qio71PjmLkUlsAaJxzZpBI/%ED%83%9C%EC%9B%85_IR25.2Q%28%EA%B5%AD%EB%AC%B8%29_2025.08.20.pdf

- CS Wind Q3 2025 reference analysis: https://drive.google.com/open?id=1fiNwBLoPamnjEajdbMFKnjf5VMjMEFVqZhnNAyBJn24