DEEP RESEARCH · SK ETERNIX

SK Eternix (475150 KS): The J-Curve of a Green-Energy Developer

A structured view of wind, fuel-cell, solar, and ESS portfolios and backlog monetization after 2026.

0. Bottom line first

The source argues that SK Eternix is moving past a 2025 transition year and entering a J-curve phase from 2026, when backlog and new projects begin converting into revenue. The key figures are KRW 638.7 billion of backlog, the 390MW Shinan Ui offshore wind project, more than 1.3GW of offshore wind pipeline, and a 3.0GW total pipeline.

Official fact: The source says SK Eternix, after its spin-off from SK D&D, established a pure-play developer model spanning development, EPC, O&M, and financial structuring.

Interpretation: The company should be viewed less as a conventional power-plant operator and more as a capital-efficient developer that takes early permitting risk and monetizes projects through financial close, development fees, PM service revenue, dividends, and equity exits.

1. Portfolio

Core growth engine

Gasiri 30MW and Uljin 53MW are operating. Gunwi Pungbaek 75MW and Uiseong Hwanghaksan 99MW are under construction. The offshore pipeline includes Shinan Ui 390MW and Incheon Gureopdo, totaling more than 1.3GW.

Cash-flow stabilizer

Based on Bloom Energy SOFC technology. Chilgok 20MW, Yakmok 9MW, and Boeun 20MW are operating, while Chungju 40MW, Daesowon 40MW, and Paju 31MW are under construction.

Financial structuring

The Solaronix funds aggregate small and mid-sized solar assets and generate development-service revenue.

Grid balancer

ESS revenue comes from owned sites and ESCO projects, while the longer-term opportunity is grid support as renewable generation grows.

2. Cumulative 3Q25 results

| Category | Revenue | Source analysis |

|---|---|---|

| Wind | KRW 82.7B | Gunwi Pungbaek 75MW reached 77% progress, with revenue recognized after turbine installation completion. |

| Solar | KRW 24.0B | Solaronix No. 2 and No. 3 development-service revenue of KRW 11.2B each was recognized. |

| Fuel cell | KRW 7.8B | Revenue is concentrated around equipment delivery timing. Chungju Eco Park delivery was expected in Q4. |

| ESS | KRW 23.2B | Revenue from owned sites and ESCO projects. |

| Operating profit | KRW 11.8B | Renewables profit was KRW 19.1B, offset by KRW 10.6B of unallocated costs. Consolidated OPM was 8.6%. |

3. 2025-2027 earnings path

Official fact: The source identifies Chungju Eco Park Fuel Cell, a 40MW project with KRW 171.9B total contract value, as the key variable for 2025 full-year results. It mentions the possibility of more than KRW 100B of Q4 revenue recognition.

- Expected 2025 revenue: KRW 230B-250B.

- Expected 2025 operating profit: KRW 20B-25B.

- From 2026, Uiseong Hwanghaksan, Daesowon/Paju fuel cells, Solaronix revenue, and early Shinan Ui recognition may connect.

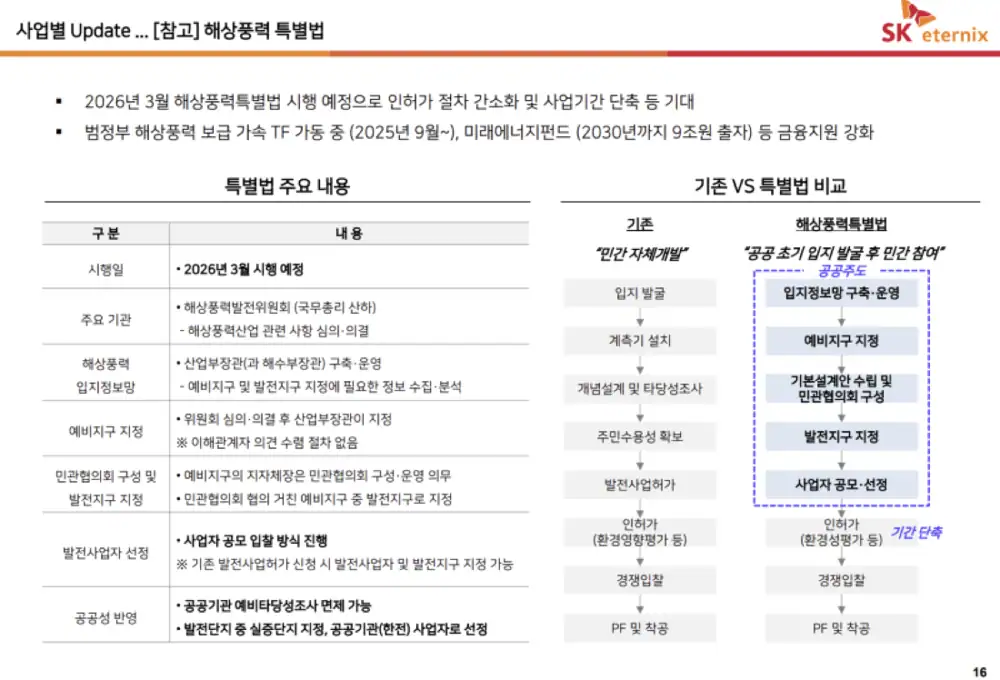

4. Shinan Ui and offshore wind legislation

Shinan Ui offshore wind is described as a 390MW project using 26 Vestas 15MW turbines, with total project cost estimated at about KRW 2.5T-3.0T. The source uses development fees of 3-5% of total project cost and gives KRW 2.5T x 4%, or about KRW 100B, as an example. After construction starts, annual EPC management revenue of KRW 30B-50B is expected, followed by 20 years of O&M and equity-method income after COD.

Official fact: Offshore wind special legislation is described as shifting from private-led site discovery to government-led planned sites, shortening permitting from an average 7-10 years to a target 4-5 years.

Interpretation: The source's simulation shows why time compression matters: assuming a KRW 300B bridge loan at a 6% rate and a two-year shorter usage period, about KRW 36B of financing cost could be saved; with a 6-7% WACC, project NPV could rise by about 15-20%.

5. Risks and balance sheet

- The 3Q25 debt ratio was 472%, but KRW 589.3B of advances received was included in total liabilities of KRW 1.1894T.

- Excluding advances received, the adjusted debt ratio is cited at about 245%.

- High rates pressure PF-heavy projects, while a rate-cut cycle would be favorable.

- Higher steel-pipe and submarine-cable costs could pressure EPC margins.

6. My conclusion

I would evaluate SK Eternix by the post-2026 revenue-recognition schedule rather than current earnings alone. The watchlist is Shinan Ui financial close and construction start, Chungju/Daesowon/Paju fuel-cell revenue recognition, offshore wind legislation, and the speed at which advances received convert into revenue.

Sources

- Naver Blog original: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224098514232

- LS Marine Solution competitiveness and cash-flow analysis: https://drive.google.com/open?id=1fvMP6Atk7eNdn4PQWi0Cxo0Egn8mhHb6UcLKqKqIxKY

- Daemyoung Energy quarterly report: https://drive.google.com/open?id=1-vJIO7F41PAZGcBrgWRB396NUQ_75z3A

- Utilities primer: https://drive.google.com/open?id=1pWnHCy_VLHXG5qKhWzpWLsFTpDmw4UdV