DEEP RESEARCH · LS MARINE SOLUTION

LS Marine Solution 2025 Q3 and Long-Term Outlook

Vessel scarcity and installation capability in offshore wind grids and submarine communications.

0. Bottom line first

Cumulative Q3 2025 revenue of KRW 188.4bn, backlog of KRW 676.2bn, and about KRW 400.0bn of liquidity form the financial base for LS Marine Solutions transition into LS Groups power and communications infrastructure construction platform.

1. Industry and corporate change

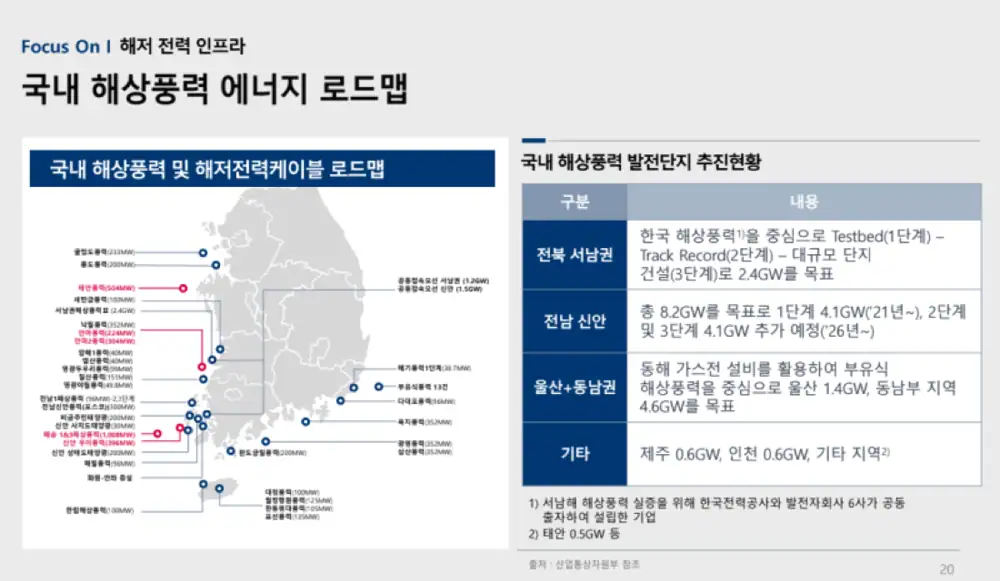

The source cites 2025-2034 offshore wind CAGR of 8.9-18.6%, EU targets of 300GW by 2050, and Korea targets of 14.3GW by 2030. On data, 99% of global traffic moves through submarine fiber cables, with AI server CAGR of 18% and submarine communications cable CAGR of 5.6-11.1% through 2030.

The predecessor KT Submarine was founded in 1995. LS Cable & System became the largest shareholder in August 2023, and as of Q3 2025 holds 67.8%, or 35,428,897 shares. The October 2024 acquisition of 100% of LS Buildwin created integrated subsea and underground construction capability.

2. Financials and backlog

| Item | Figure |

|---|---|

| Cumulative revenue | KRW 188.4bn, +110.8% versus KRW 89.4bn YoY |

| Subsea/underground revenue | Subsea KRW 58.2bn, underground KRW 130.1bn |

| OP/net income | KRW 8.48bn / KRW 7.34bn |

| Total assets | KRW 705.5bn, about +177% from KRW 254.2bn at end-2024 |

| Liquidity | Cash KRW 109.7bn + short-term financial assets KRW 291.1bn |

| Debt ratio | 12.7%, liabilities KRW 79.7bn and equity KRW 625.8bn |

| Backlog | KRW 676.2bn, subsea KRW 143.8bn and underground KRW 532.4bn |

3. Assets and regional opportunities

- GL2030 was built in 2012, has about 4,000t cable capacity being upgraded to about 7,000t, and has DP2 rating.

- The new 13,000t HVDC CLV requires KRW 345.8bn investment, is scheduled for 1H 2028 delivery, and is described as Asia-largest and global top-five spec.

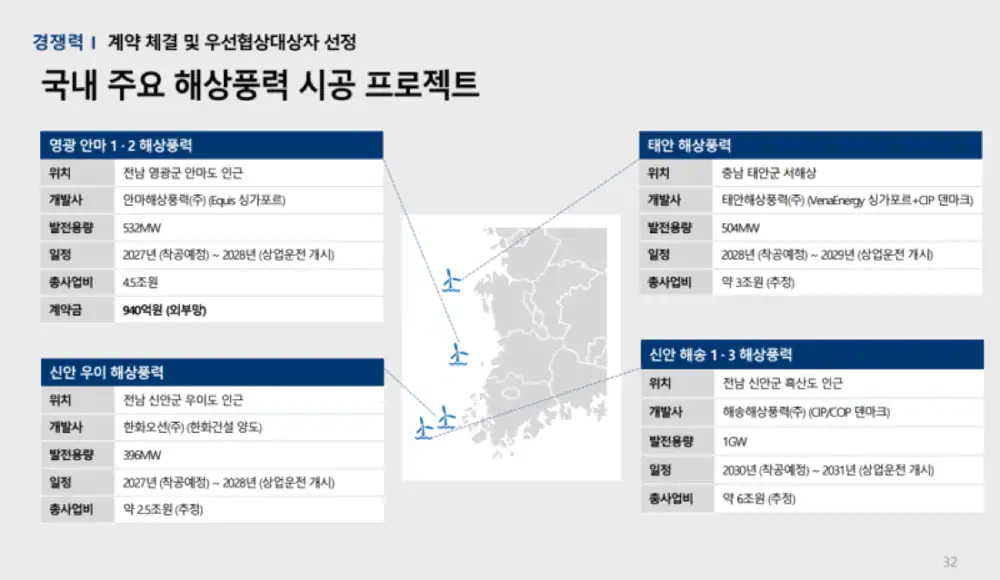

- Anma offshore wind is cited at about KRW 940.0bn including LS Cable & Systems portion, with revenue recognition expected from 2025.

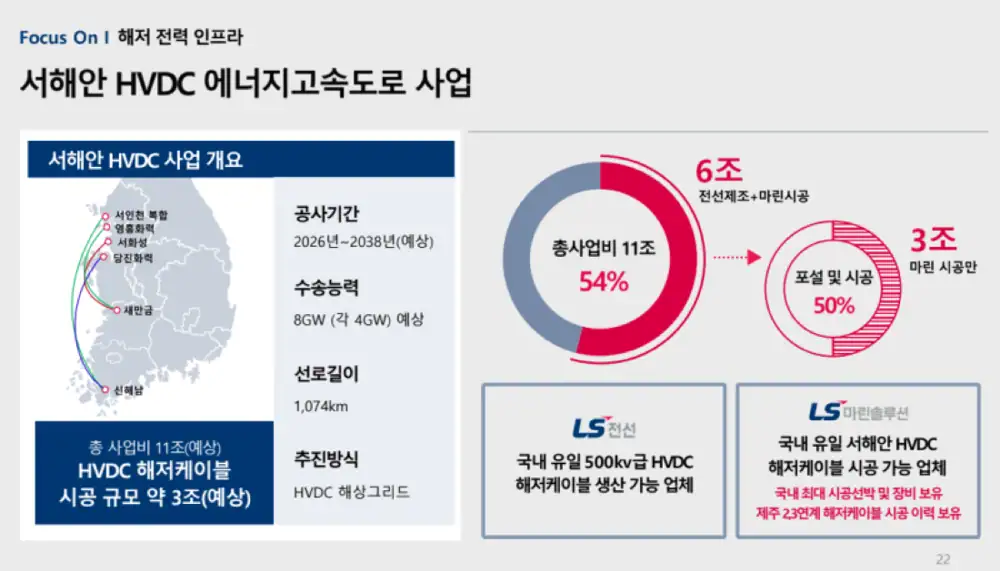

- The west-coast HVDC energy highway is presented as an opportunity of about KRW 11tn.

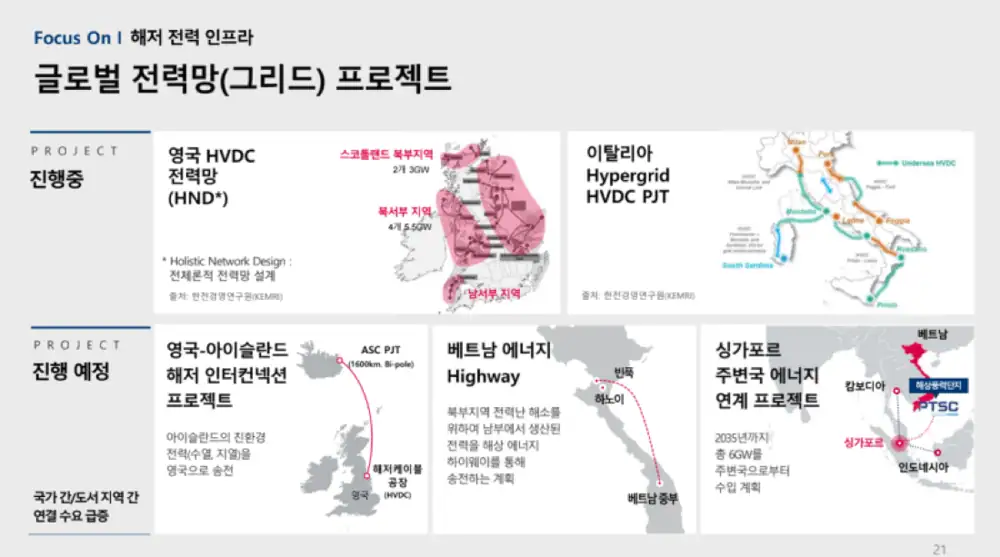

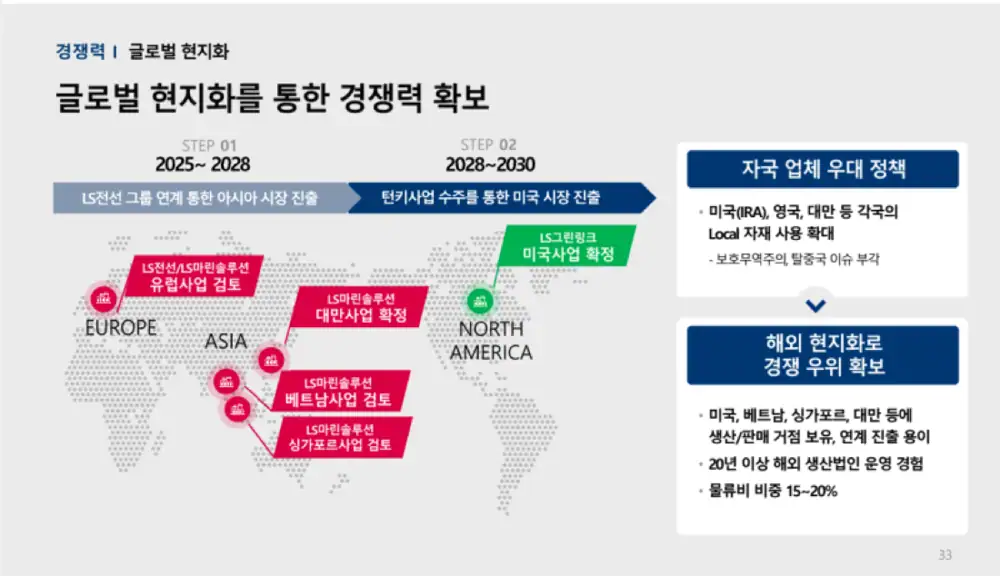

- Taiwan TPC phase 2 and Vietnams PDP8 target of 6GW offshore wind by 2030 are overseas opportunities.

4. Risks and conclusion

The KRW 200.0bn exchangeable bond is an overhang risk, and the KRW 345.8bn new-vessel CAPEX can burden cash flow before 2028 delivery. Submarine construction is sensitive to weather, sea conditions, project delays, and geopolitical variables. The key is converting backlog into revenue and profit before the 2028 CLV arrives.

Sources

- Original Naver post

- https://drive.google.com/open?id=1Y9bygXfP7q_6r-26YrD_9b1xWsq8RY_51Ju-kHuEjm8

- https://drive.google.com/open?id=1cCH2iUc-vz0l0vRkm3tUHEZX2ClMTPL1j9lSUxIeNYk

- https://www.investchosun.com/site/data/html_dir/2025/10/27/2025102780256.html

- https://www.businesspost.co.kr/BP?command=article_view&num=417188

- https://drive.google.com/open?id=1_MSB7iNrK3M6AIt-sh8FJ_Pf8GtvsCUhU_OfgPxZHos

- https://www.electimes.com/news/articleView.html?idxno=341167

- https://www.mt.co.kr/industry/2025/08/17/2025081423435139037

- https://www.lscns.co.kr/kr/pr/news_view.asp?brd_id=news1&mode=MOD&idx=118796&lang_cd=kr

- https://energy.ketep.re.kr/globalenergy/site/main/board/energy_plan/16440

- https://www.leeko.com/leenko/news/newsLetterView.do?lang=KR&newsletterNo=2150