DEEP RESEARCH · ENGLEWOOD LAB

Englewood Lab (KOSDAQ 950140): The Moat Proven by Results — A Deep Dive into the 3Q25 Earnings Surprise

Revenue +14% / Operating profit +120% beat — OTC expertise and the 'Two-Track' tariff shield ignite simultaneously at a structural inflection point

0. Bottom Line First

3Q25 preliminary results beat the consensus operating profit (KRW 6.0B) by +120%, posting KRW 13.2B — not a one-off windfall, but a structural event signaling that the economic moat Englewood Lab has built over years has entered its earnings-leverage phase.

Official facts: Revenue KRW 61.8B (consensus 54.0B, +14.4%), operating profit KRW 13.2B (consensus 6.0B, +120.0%), net income KRW 11.0B, OPM 21.4%.

Interpretation: Operating profit growth is over 8x revenue growth — prior investments (automation lines, etc.) are complete, the high-margin OTC mix is exploding, and operating leverage is being maximized. Crucially, this is happening exactly when peers are wobbling under "US tariff risk" — Englewood Lab is the opposite story.

1. 3Q25 Earnings Deep Dive — Operating Leverage Maximized

A. Quantitative Anatomy of 3Q Preliminary Results

Disclosed on Nov 6, 2025, Englewood Lab's 3Q consolidated preliminary results overwhelmed market expectations on every front.

- Revenue KRW 61.8B — vs. consensus KRW 54.0B, +14.4%

- Operating profit KRW 13.2B — vs. consensus KRW 6.0B, +120.0% earnings surprise

- Net income KRW 11.0B

Interpretation: The most striking point is that revenue growth (+14.4%) versus operating profit growth (+120.0%) is abnormally lopsided. This proves the P&L has entered a strong operating leverage regime, beyond the burden of fixed costs. After front-loaded investments such as the automation lines that came online in 1H25 wrapped up, the "harvest phase" — where incremental revenue drops straight to massive profit gains — has begun.

B. Last Five Quarters — Confirming a Structural Growth Trajectory

This did not appear out of thin air in 3Q. Reworking the last five quarters through the lens of operating margin (OPM) shows a fundamental quality improvement starting in 2Q25.

| Metric | 3Q24 | 4Q24 | 1Q25 | 2Q25 | 3Q25 (prelim) |

|---|---|---|---|---|---|

| Revenue (KRW bn) | 40.9 | 42.4 | 42.5 | 58.5 | 61.8 |

| Operating profit (KRW bn) | 4.1 | 3.7 | 4.6 | 10.2 | 13.2 |

| Net income (KRW bn) | 0.5 | 7.8 | 3.2 | 3.0 | 11.0 |

| OPM | 10.0% | 8.7% | 10.8% | 17.4% | 21.4% |

| OP vs. consensus | — | — | −35% | +103% | +120% |

Interpretation: An OPM stuck around 10% executed a first quantum leap to 17.4% in 2Q25 and then jumped to 21.4% in 3Q — exceptional profitability for a manufacturer. This strongly suggests fixed-cost leverage and a high-margin product-mix shift are exploding simultaneously, not just topline growth.

2. Core Drivers of the Surprise — US Indie Brands + OTC Suncare

The secret behind the 21.4% OPM in Chapter 1 lies in the product portfolio and the customer mix. The 3Q beat was driven not by quantitative expansion of generic cosmetics riding the K-beauty wave, but by two qualitative engines: high-margin OTC and validated indie brands.

A. Driver 1 — Explosive Growth and Re-orders from US Indie Beauty Brands

The core background of the 3Q beat is "a surge in re-orders from US indie brands." This is an acceleration in 3Q of the "successful new-product launches and normalized orders from key customers" trend first observed in 2Q25.

The decisive point is that this is re-orders, not new wins. Re-orders mean products designed and manufactured by Englewood Lab were successfully validated by end consumers in the US. It is evidence of a "lock-in effect" — Englewood Lab's results are now synchronized with its customers' growth, not a one-shot revenue event.

B. Driver 2 — Revenue Surge in High-Margin OTC (Over-the-Counter) Sunscreens

The most decisive factor behind the 120% surprise and 21.4% OPM is "the surge in OTC sunscreen revenue." In the US, sunscreens are not regular cosmetics — they are classified as Over-the-Counter (OTC) drugs under strict FDA regulation.

Generic skincare

Englewood Lab 2Q25 mix: 68.0%. Lower entry barrier, ordinary margin profile.

OTC products

Englewood Lab 2Q25 mix: 23.5%. Requires FDA cGMP certification → high entry barrier. Regulatory and clinical costs are baked into ASP → ASP and margin substantially higher than generic cosmetics.

Interpretation: 3Q results reflect the high-margin OTC mix expanding explosively, dragging the whole-company profitability dramatically higher.

C. Successful Fusion of K-Beauty Trend and Localization Strategy

In the US market, K-beauty — especially Korean sunscreens — has seen demand surge thanks to superior quality and feel. Englewood Lab is the maximum beneficiary, combining the R&D strength of K-beauty (Korean entity) with US local production and regulatory compliance (US HQ) to meet that demand perfectly. Formulations developed by parent Cosmecca Korea (e.g., cleansing oils) have become bestsellers on Amazon and TikTok, and the rise of K-beauty indie brands is translating directly into order growth at their core production partner, Englewood Lab.

3. Moat Analysis 1 — FDA-Regulated 'OTC Expertise' (Technology & Speed Moat)

Englewood Lab's core identity is not just another cosmetics ODM — it is an OTC specialist tuned for US FDA regulation. This builds a strong "technology and speed moat" peers cannot easily imitate.

A. Moat 1 — Regulatory Barrier to Entry

To operate in the US, you must comply with FDA's strict guidelines treating sunscreens, acne products, etc., as OTC drugs. Englewood Lab has operated a cGMP-certified manufacturing facility (Totowa, New Jersey) that has passed FDA OTC audits since 2011, accumulating specialized experience and trust. Beyond OEM/ODM, it provides "consulting" for FDA and other export-country regulations and in-house clinical/testing (safety, toxicity, etc.) solutions.

Interpretation: Once an OTC product is registered with the FDA, changing manufacturer or facility is very onerous → this creates high switching costs for customers, making it difficult to walk away from Englewood Lab.

B. Moat 2 — Speed Moat (Time-to-Market)

In indie beauty, trends shift fast — "time-to-market" decides winners and losers. Englewood Lab holds a decisive weapon: the 'Ready To Go (RTG) OTC' solution, co-developed with parent Cosmecca Korea.

RTG offers five "ready" OTC sunscreen formulations that already comply with FDA guidelines and have completed clinicals. Typical OTC development and launch takes about 12–18 months; RTG customers can compress this to about 6 months.

Interpretation: Englewood Lab is not just selling "cosmetics" — it is selling "time", the single most precious resource for indie brands. That is a service moat peers cannot replicate.

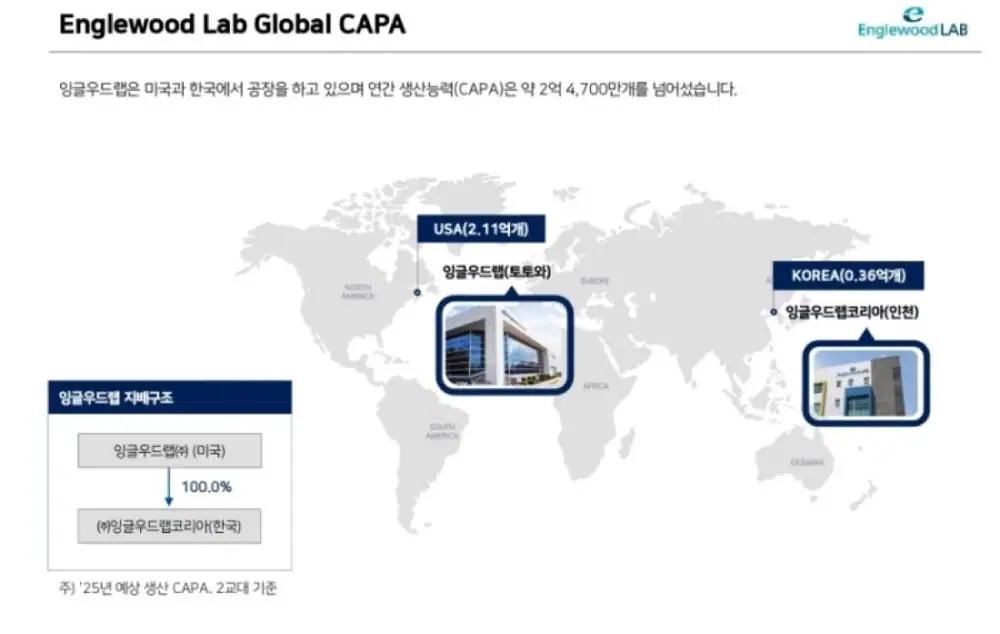

4. Moat Analysis 2 — The 'Two-Track' Supply Chain Neutralizing Tariff Risk (Geopolitical & Cost Moat)

A. The 'Two-Track' Production System

Englewood Lab operates a distinctive dual production system: a US HQ plant in Totowa, New Jersey (Made in USA) and a Korean plant in Incheon (Made in Korea) via subsidiary Englewood Lab Korea. It allocates flexibly between US-local and Korean production according to customer needs, responding nimbly to tariff risk and supply uncertainty.

B. The Decisive Differentiator vs. Peers — US Tariff Risk

The true value of this 'Two-Track' strategy stands out starkly in today's geopolitical risk environment.

| Metric | Englewood Lab | Cosmax | Kolmar Korea |

|---|---|---|---|

| 3Q25 earnings momentum | Earnings surprise (+120%) | Expected to miss consensus | Expected to meet consensus |

| 3Q25 US tariff impact | None (beneficiary) | Negative | Limited (Canada entity) |

| US local OTC production base | Owned (New Jersey) | Limited (NJ / Ohio) | Limited (Canada / PA) |

| OTC R&D / regulatory capability | Best (RTG solution) | Mid-high | Mid-high |

| 'Time-to-Market' solution | Owned (6 months) | — | — |

Interpretation: The 'Two-Track' strategy is not just capacity diversification — it acts as a perfect hedge against US protectionism and geopolitical supply-chain risk (tariffs, logistics): a "Tariff Shield." Beyond defense, it becomes an offensive weapon. As US indie brands accelerate onshoring to escape tariff burdens and logistics instability, Englewood Lab — the only partner delivering both K-beauty R&D and a 'Made in USA' production base — is absorbing the onshoring tailwind exclusively. The 3Q surge is partly the result of peer risk (tariffs) turning into Englewood Lab's opportunity (onshoring wins).

5. Moat Analysis 3 — Operational Efficiency and Synergy

An exceptional 21.4% OPM in 3Q requires not only the "high-margin product" and "supply-chain advantage" already analyzed, but also the operational efficiency to support them physically.

A. Operating Leverage Maximized via Automation

From 1H25, Englewood Lab brought the Totowa plant's automation lines into full operation, maximizing production efficiency. The impact was already visible in 1H25 results — gross profit margin improved from 21.0% (1H24) to 25.2% (1H25), a +4.2pp gain. The 21.4% OPM in 3Q is the result of high-margin OTC revenue surging on top of this newly streamlined cost base, maximizing operating leverage.

The production assets are also built for "accurate scalability" — flexibly handling small-batch, high-mix indie brand orders as well as large-scale runs for major brands. This is the foundation for managing a broad customer portfolio from small indies all the way to 80+ major brands efficiently.

B. Powerful Synergy with Parent Cosmecca Korea

Acquired by Cosmecca Korea in 2018 (44.1% stake), Englewood Lab has become more than a typical subsidiary — it generates powerful strategic synergy.

- R&D synergy: In 2019, the R&D organizations of Englewood Lab Korea and Cosmecca Korea were integrated. The 'RTG OTC' solution is the most successful output of this combined R&D.

- Sales / earnings synergy: Cosmecca Korea supports K-beauty indie brands in their overseas expansion (Amazon, TikTok); Englewood Lab handles US local production and OTC regulation for those brands. As a result, both companies posted record-breaking results simultaneously in 3Q25.

Interpretation: A powerful strategic combination of complementary core capabilities — R&D (Korea) and production/regulation (US). It is hard for other firms to replicate quickly.

6. Wrap-Up and Outlook — Is the Structural Growth Sustainable?

A. The Three Moats Summarized

The 3Q25 earnings surprise is not a one-off — I view it as a structural achievement of three powerful economic moats firing at once after years of strategic build.

(1) Regulatory / Tech Moat

Steep FDA OTC barrier + standout R&D. cGMP-certified since 2011; FDA-registered products are very hard to switch manufacturers → high switching costs.

(2) Speed Moat

RTG OTC compresses time-to-launch by over a year (18 months → 6 months). A business that sells "time" to indie brands.

(3) Supply Chain / Tariff Moat

'Two-Track' + 'Made in USA' → avoids tariff risk and monopolizes the onshoring tailwind.

B. Unique Positioning vs. the Competitive Set

The US indie brand and OTC suncare market is the most important battleground for Korean ODMs. While peer Cosmax faces "tariff" risk and is expected to miss the quarter, Englewood Lab has succeeded in flipping that risk into a shield, accelerating share gain — a uniquely strong positioning.

C. Medium- to Long-Term Sustainability

Short term, I expect the high-margin OTC orders and indie-brand onshoring demand observed in 3Q to persist through 4Q25 and into 1H26. Over the medium-to-long term, three forces should reinforce Englewood Lab's moats further:

- Structural growth of the US indie beauty market

- Continued expansion of K-beauty and Korean sunscreen demand in the US

- The strengthening US protectionist (tariff) regime

D. Potential Risks

Risks exist, of course:

- Failure of a key indie brand customer's hit cycle

- Raw-material price volatility

- Acceleration of competitors' US local OTC capex

As of now, however, the structural growth momentum from the moats appears far stronger than these risks. 3Q25 marks the inflection point where Englewood Lab's structural competitiveness converts into real earnings growth.

Sources

- Cosmecca Korea 3Q OP KRW 27.2B, +78.8% YoY — Daum: https://v.daum.net/v/20251106170426788

- Englewood Lab — '5 US sunscreens deliverable in 6 months' — Yakup News: http://m.yakup.com/news/index.html?mode=view&cat=12&nid=295770

- Cosmax — 3Q to miss on US tariffs / weaker Japan exports (NH) — Infostock Daily: https://www.infostockdaily.co.kr/news/articleView.html?idxno=211288

- 'Two-Track production' Englewood Lab benefits from US indie brand growth — Daily Invest: http://www.dailyinvest.kr/news/articleView.html?idxno=69020

- Englewood Lab — earnings growth visible this year, operating leverage to lift OPM — etoday: https://m.etoday.co.kr/view.php?idxno=2355560&trc=main_section_sf

- Stockeasy — AI stock analysis solution: https://stockeasy.intellio.kr/share_chat/616995c4-c972-4544-a5ff-7a92e394f2ca

- Englewood Lab: Revenue, Competitors, Alternatives — Growjo: https://growjo.com/company/Englewood_Lab

- Englewood Lab IR (2024-07-08) Key management briefing (PDF): alphasquare.co.kr (IR PDF)

- Englewood Lab — tariff-proof, FDA-certified US factory in focus — etoday: https://www.etoday.co.kr/news/view/2458755

- Englewood Lab Korea — History: http://englewoodlab.com/ko/history

- Englewood Lab Korea — R&D: http://englewoodlab.com/ko/rnd

- Englewood LAB — Home (EN): http://www.englewoodlab.com/en/home

- Cosmetic CDMO Market Research Report 2025 — InsightAce Analytic: https://www.insightaceanalytic.com/report/cosmetic-cdmo-market/3164

- LS Securities — note on Korean K-beauty fit — Investing.com KR: https://kr.investing.com/news/stock-market-news/article-1676895

- NH — 'Kolmar Korea 3Q standalone slowdown concerns overdone, buy on weakness valid' — Chosun Biz: https://biz.chosun.com/stock/stock_general/2025/10/13/KSQ5F5TSUFCWJIZZHX7NSDW424/

- Manufacturing — Englewood LAB: http://englewoodlab.com/en/manufacturing

- Englewood Lab Korea — CEO: http://englewoodlab.com/ko/ceo

- Englewood Lab — 3Q revenue +20.5%, OP +262.2% — Cosin Korea: https://www.cosinkorea.com/news/article.html?no=37488