DEEP RESEARCH · YOULCHON CHEMICAL

Youlchon Chemical: Opportunity and Financial Risk in the Battery Pouch-Film Transition

A report on the packaging cash cow, LG Energy Solution partnership, Poseung plant, and pouch-format risk

0. Bottom line first

Youlchon Chemical is shifting its center of gravity from stable packaging materials to battery pouch film. The opportunity lies in LG Energy Solution and supply-chain localization away from Japan; the risks are single-customer dependence, utilization after the Ultium Cells contract cancellation, higher debt, and losses in electronic materials.

1. Business structure: packaging base and electronic-materials growth

Official fact: Youlchon Chemical was founded on May 1, 1973 and is affiliated with Nongshim Group. Its packaging segment produces flexible packaging, BOPP film, and CPP film; the source describes it as holding a leading position in Korean flexible and corrugated packaging.

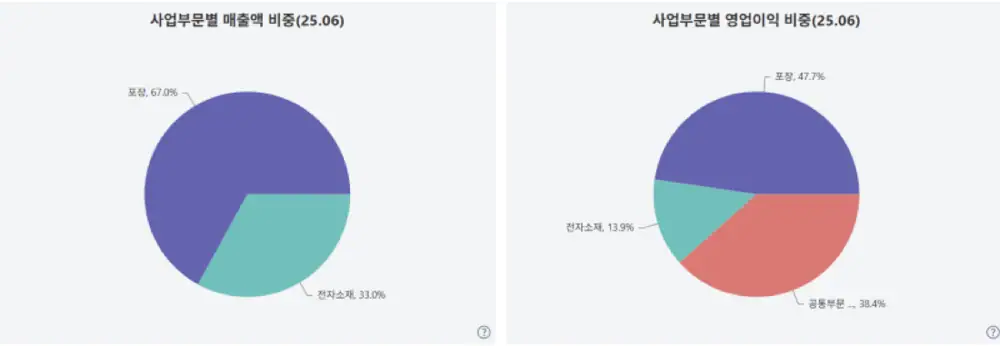

Official fact: The packaging segment accounts for about 77.8% of total revenue, and its 2019 operating margin is cited at 11.2%. The electronic-materials segment accounts for about 22% of revenue, with lithium-ion battery aluminum pouch film (LiBP) as the core product.

Official fact: On January 31, 2024, Youlchon completed the transfer of its paperboard-related packaging business to Tailim Packaging. That business represented about 10% of revenue, and the KRW 43.0 billion sale proceeds were intended for new-business investment.

Interpretation: This is not just a disposal. It is a capital-allocation statement: reduce part of the stable legacy business and redeploy capital into the riskier but larger-upside electronic-materials business.

2. Pouch-film market: large market, high barriers, format risk

US$1.993B in 2024

One forecast sees the market growing to US$12.4B by 2033, a 21.6% CAGR.

DNP and Showa Denko oligopoly

The two firms are cited at 73~90%+ combined share, with DNP alone around 55%.

5~9 multilayer structure

Micron-level uniformity, pinhole-free surfaces, and more than two weeks of clean-room production are required.

Prismatic 69%, pouch 19%

Battery format competition may constrain TAM even if EVs grow.

Official fact: Another market researcher sees the pouch-film market reaching US$3.4247B by 2027, with EVs driving a 20% CAGR. The source also notes that 15 of the top 20 EV models in Europe in 2020 used pouch-type batteries.

Official fact: DNP’s core strength is a proprietary adhesive-free extrusion lamination process, said to achieve adhesion above 10N/15mm. Youlchon may use dry lamination based on its high-performance adhesive development history, but its supply of newly developed pouch film to LG Energy Solution indicates that it met a top-tier customer standard.

Interpretation: Youlchon does not necessarily need to clone DNP perfectly. The strategy is to hit the best balance of performance, cost, and supply-chain stability. Localization away from Japanese suppliers is the strategic tailwind.

3. LG Energy Solution nexus: relationship maintained, concentration risk remains

Official fact: In September 2022, Youlchon signed an aluminum pouch-film supply contract worth about KRW 1.4~1.5 trillion with Ultium Cells, the LG Energy Solution-GM joint venture. In July 2024, Ultium requested contract termination, citing EV-demand slowdown and suspension of its third U.S. plant construction.

Official fact: After the cancellation, Youlchon continued supplying LG Energy Solution directly and expanded into ESS pouch film. It also supplied LG Energy Solution with a lightweight, high-heat-resistant new pouch film developed through a government project.

Official fact: Youlchon invested KRW 83.6 billion to build an aluminum pouch plant in Poseung, Pyeongtaek. Including the existing Ansan plant, it plans to secure annual pouch capacity of 110 million square meters by 2026.

Interpretation: The Ultium cancellation looks more like macro EV headwinds than a technology failure. But nearly every electronic-materials milestone is tied to LG Energy Solution, which is a structural weakness. New contracts with SK On, Samsung SDI, or other customers would be the key quality signal.

4. Financial microscope: a race against time

| Metric | Source figure | Read-through |

|---|---|---|

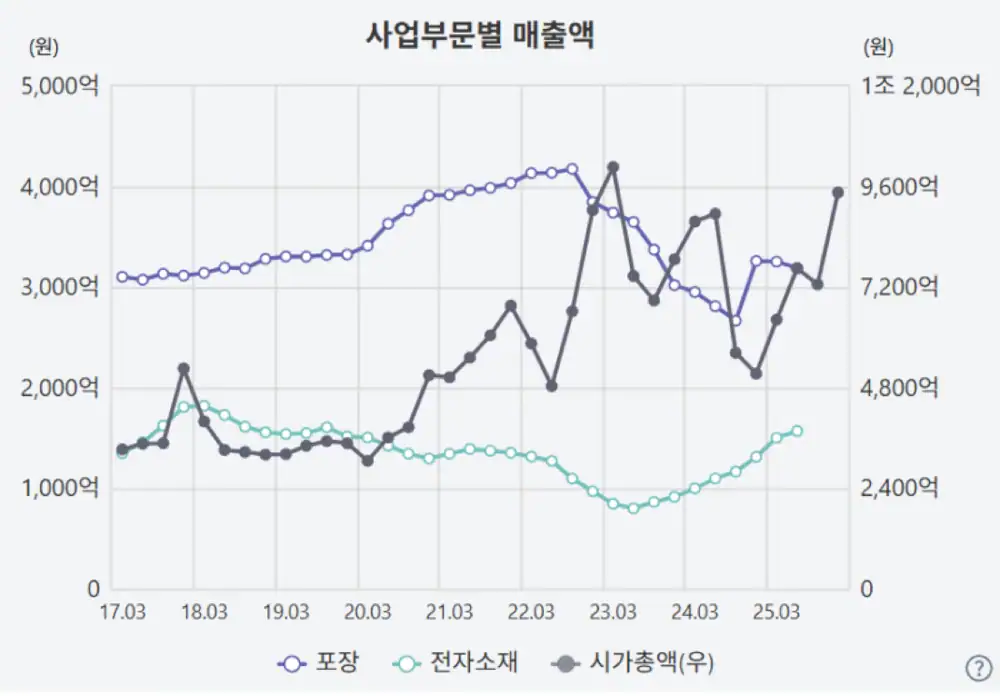

| Revenue | KRW 538.7B in 2021 → KRW 457.9B in 2022 → KRW 414.5B in 2023 | Revenue decline and business-transfer effects |

| Operating margin | 2.05% in 2021, -1.31% in 2022, -3.91% in 2023 | Sharp profitability deterioration |

| 2024 estimate | Operating loss of KRW 18.355B | Electronic-materials investment burden continues |

| Borrowings | KRW 145.1B in 2020 → KRW 248.8B in 2023 | Financial burden from Poseung and other investments |

| ROE | -5.96% in 2023 | Pressure on shareholder value |

Official fact: The source interprets the electronic-materials segment’s operating margin as bottoming at -20% to -30% in 2023~2024, then narrowing losses in 2025 and approaching breakeven in a V-shaped recovery.

Interpretation: The Poseung plant is already fixed cost. The Ultium contract was supposed to accelerate scale economics; after cancellation, Youlchon must fill the gap more gradually through LG ESS and new customers. That can lengthen the cash-burn period.

5. SWOT and strategic path

| Strengths | Weaknesses | |

|---|---|---|

| Opportunities | Use LG Energy Solution partnership and Korean production base to capture ESS and localization demand | Win new customers and scale to reduce LG dependence and financial pressure |

| Threats | Deepen technology cooperation with LG to maintain a gap versus Chinese competitors | Use conservative finance and cost competitiveness against downturns and price competition |

Breaking the Japanese oligopoly

With LG Energy Solution and the Poseung plant, Youlchon can become a key enabler in the global EV/ESS supply chain.

Transition cost too high

Contract cancellation, customer concentration, debt, and electronic-materials losses could combine before scale arrives.

6. Metrics I would track

- Poseung plant utilization and whether 110 million square meters of 2026 capacity is reached

- Supply contracts with customers beyond LG Energy Solution

- Timing of electronic-materials operating breakeven

- Debt-ratio stabilization or decline

- Pouch-battery share and LME aluminum prices

- Next-generation pouch-film announcements that narrow the technology gap with DNP

Sources

- Original Naver Blog post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224045887605

- Source 1: https://www.butler.works/

- Source 2: https://kind.krx.co.kr/common/disclsviewer.do?method=search&acptno=20240318000865&docno&viewerhost&

- Source 3: https://alphasquare.co.kr/home/stock-summary?code=008730

- Source 4: https://www.thecommoditiesnews.com/news/articleView.html?idxno=7695

- Source 5: https://www.catch.co.kr/Comp/AnalysisCompView?ID=2744

- Source 6: https://comp.fnguide.com/SVO2/ASP/SVD_Main.asp?gicode=A008730

- Source 7: https://www.ibtomato.com/mobile/mView.aspx?no=3135&type=1

- Source 8: https://kind.krx.co.kr/common/disclsviewer.do?method=search&acptno=20240516001193&docno&viewerhost&

- Source 9: https://www.businesspost.co.kr/BP?command=article_view&num=401732

- Source 10: https://contents.premium.naver.com/rvs/tbw/contents/250830205558351nu

- Source 11: https://www.businessresearchinsights.com/ko/market-reports/lithium-battery-aluminium-plastic-film-market-104881

- Source 12: https://www.electimes.com/news/articleView.html?idxno=226312

- Source 13: https://www.kier.re.kr/tpp/energy/A/view/232?contentsName=below4_5&menuId=MENU00963

- Source 14: https://www.thelec.kr/news/articleView.html?idxno=15419

- Source 15: https://www.thelec.kr/news/articleView.html?idxno=11429

- Source 16: https://apps.3protv.com/news/view/1159

- Source 17: https://www.dongwon.com/post/1377

- Source 18: https://sbtlam.com/sub/sub03_02.php?mNum=3&sNum=2&boardid=news&mode=view&idx=1

- Source 19: https://www.waterindustry.co.kr/overseas/overseas01.php?ptype=view&idx=120909&page=14&code=overseas01&category=175

- Source 20: https://www.global.dnp/ko/corporate/global-share/

- Source 21: https://smroadmap.smtech.go.kr/TipaCms/cmm/fms/FileDown.do?gubun=userReport&atchFileId=FILE_000000000004084&fileSn=0

- Source 22: https://hanbatech.com/tech-transfer/1916

- Source 23: https://batterydive.com/863556/

- Source 24: https://www.thelec.kr/news/articleView.html?idxno=38424

- Source 25: https://greenium.kr/news/60118/

- Source 26: https://m.ekn.kr/view.php?key=20240614024206087

- Source 27: https://www.thelec.kr/news/articleView.html?idxno=35626

- Source 28: https://biz.chosun.com/stock/stock_general/2024/07/31/JCV5A6EVQFCTNOYBZBU6X6EVPE/

- Source 29: https://www.investchosun.com/site/data/html_dir/2024/07/31/2024073180020.html

- Source 30: https://m.etnews.com/20221123000254?obj=Tzo4OiJzdGRDbGFzcyI6Mjp7czo3OiJyZWZlcmVyIjtOO3M6NzoiZm9yd2FyZCI7czoxMzoid2ViIHRvIG1vYmlsZSI7fQ%3D%3D

- Source 31: https://invest.deepsearch.com/stock/008730/

- Source 32: https://markets.hankyung.com/stock/008730/financial-summary

- Source 33: https://alubase.co.kr/?kboard_content_redirect=8

- Source 34: https://www.mitrade.com/kr/insights/commodities/metal-investment/aluminum-market-in-2024

- Source 35: https://ko.tradingeconomics.com/commodity/aluminum

- Source 36: http://almarket.net/assets/lme.php?bo_table=market

- Source 37: https://www.sunsirs.com/kr/detail_news-22632.html

- Source 38: https://kr.investing.com/commodities/aluminum-historical-data

- Source 39: https://comp.wisereport.co.kr/company/c1030001.aspx?cmp_cd=008730&cn

- Source 40: https://www.thebigdata.co.kr/view.php?ud=202410210427101972cd1e7f0bdf_23