DEEP RESEARCH · TECHWING

Techwing Inc.: Building the Test Infrastructure for the AI Revolution

An investment thesis on the shift from memory test-handler leader to HBM cube-prober growth stock

0. Bottom line first

Techwing is being re-rated from a leading memory test-handler company into an AI infrastructure beneficiary centered on its Cube Prober for HBM testing. The critical question is whether qualification and mass adoption by Samsung Electronics, SK hynix, and Micron turn into real orders.

1. Investment thesis and risks

Interpretation: The source presents Techwing as a sector top pick. If Cube Prober passes qualification at the three major memory makers, it could create a multi-year revenue stream tied directly to the AI supercycle, while a higher-margin product mix could justify re-rating.

- Crown jewel: Cube Prober, an HBM test handler, is the core growth engine.

- Customer CapEx: HBM and AI-memory investment plans from SK hynix and Micron support equipment demand.

- Consumables cushion: recurring C.O.K. sales provide high margin and stable cash flow.

- Main risks: delayed qualification, high customer concentration at SK hynix and Micron, and competitive responses from players such as Advantest.

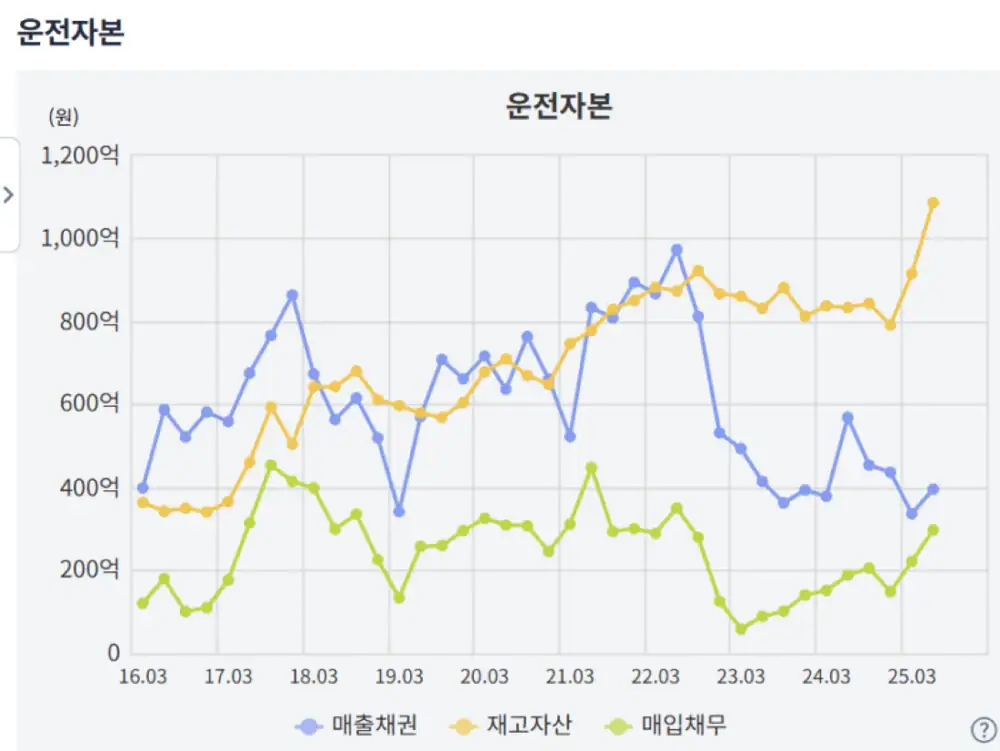

2. Business structure: guardian of backend quality

Official fact: Techwing supplies test handlers for the semiconductor backend process. The handler works with a tester, picks up chips, places them into test sockets under precise temperature conditions, and sorts them by pass/fail/grade.

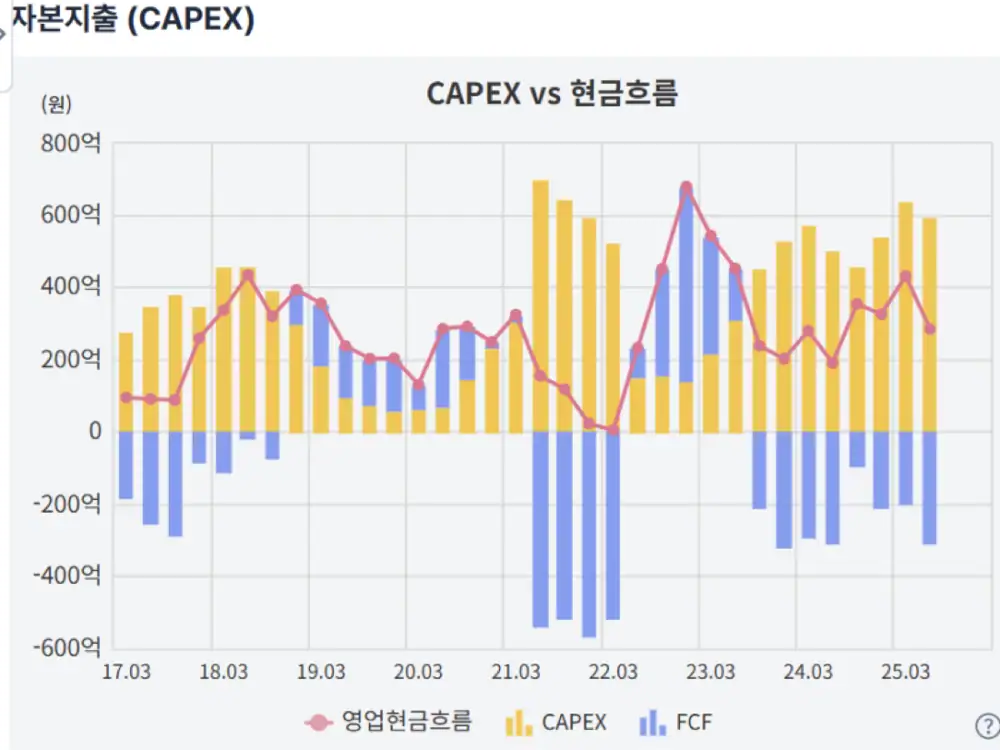

The source acknowledges the company’s historical link to DRAM/NAND cycles and recent weak quarterly results. But the stock’s strength is interpreted as the market looking beyond current earnings toward Cube Prober qualification and production ramp.

3. Product portfolio and re-rating points

| Area | Role | Investment meaning |

|---|---|---|

| Memory test handler | Feeds and sorts semiconductor chips for testing | Legacy core business and global leadership base |

| Cube Prober | New product targeting HBM testing | Potential valuation re-rating if it solves AI memory test bottlenecks |

| C.O.K. | Change Over Kit consumables | Recurring revenue and cash-flow stability |

| R&D | HBM and next-generation test solutions | Current cost burden can become a future growth option |

HBM test bottleneck

As AI memory demand grows, test complexity and throughput become more important.

Memory-maker qualification

Qualification and mass-order conversion are the key events that validate the thesis.

Price ahead of earnings

The gap between current earnings and future expectations makes the stock sensitive to news and order timing.

4. What I will monitor

- Cube Prober qualification results and adoption by customer.

- How much HBM-related sales replace or expand legacy test-handler revenue.

- Whether high-margin product mix shows up in operating margin.

- Whether competitor and customer-concentration risks ease.

- How much recurring C.O.K. sales absorb R&D cost and cycle volatility.

Sources

- Original Naver Blog post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224015933060

- Source link 1: https://www.etoday.co.kr/news/view/2506592?trc=right_hot_news

- Source link 2: https://seo.goover.ai/report/202503/go-public-report-ko-65c7aa09-2889-4420-ab94-33bd7a28522b-0-0.html

- Source link 3: http://www.dailyinvest.kr/news/articleView.html?idxno=63393

- Source link 4: https://zdnet.co.kr/view/?no=20250402155048

- Source link 5: https://www.yna.co.kr/view/AKR20250724057152003

- Source link 6: https://www.newspim.com/news/view/20250612000964

- Source link 7: https://mobile.newsis.com/view/NISX20250613_0003211793

- Source link 8: https://www.myasset.com/sitemanager/upload/2025/0416/070414/20250416070414647_0_ko.pdf

- Source link 9: http://money2.daishin.co.kr/e5/Pagelet/Board/Research/filedownload.aspx?gubun=0&rowid=C8Vnpea1HtHHvA4WvB48JY2djr6Aw00CYcHTz6ZL666e6a4e06j2e5Me6h4x904GT5jJsbXobixFFPIPb2RIGYYtR3mI21ca02jR10&word=6riw7JeF67aE7ISd&searchtype=Research

- Source link 10: https://www.newsway.co.kr/news/view?ud=2024072316025746148

- Source link 11: http://www.dailyinvest.kr/news/articleView.html?idxno=59002

- Source link 12: https://www.bondweb.co.kr/_research/downloadPage.asp?number=816549&gn=1

- Source link 13: https://seo.goover.ai/report/202504/go-public-report-ko-0e413575-3e6e-43dd-a5f3-41f9fec15b0a-0-0.html

- Source link 14: https://ssl.pstatic.net/imgstock/upload/research/company/1629947708998.pdf

- Source link 15: https://www.catch.co.kr/Comp/AnalysisCompView?ID=3154

- Source link 16: https://m.ddaily.co.kr/page/view/2019122213425668011

- Source link 17: https://www.asan.go.kr/naeil/interview/?m_mode=view&pds_no=2017120717103905629&PageNo=6

- Source link 18: https://ssl.pstatic.net/imgstock/upload/research/company/1695338537699.pdf

- Source link 19: https://www.thelec.kr/news/articleView.html?idxno=3871

- Source link 20: https://comp.fnguide.com/SVO2/asp/SVD_Finance.asp?pGB=1&gicode=A089030&cID&MenuYn=Y&ReportGB=B&NewMenuID=103&stkGb=701

- Source link 21: https://comp.fnguide.com/SVO2/ASP/SVD_Main.asp?gicode=A089030&MenuYn=Y

- Source link 22: https://www.yna.co.kr/view/AKR20250714087300527

- Source link 23: https://www.giikorea.co.kr/report/qyr1453656-global-test-handler-market-research-report.html

- Source link 24: https://www.businessresearchinsights.com/ko/market-reports/test-handler-market-107135

- Source link 25: https://ssl.pstatic.net/imgstock/upload/research/company/1689211107376.pdf

- Source link 26: https://file.kdb.co.kr/fileView?groupId=E49EC0E6-F243-5B37-9586-D097FD724BD2&fileId=59D62619-83C0-01EC-F6FC-83BCAAC00856

- Source link 27: https://m.segyebiz.com/newsView/20240515510002

- Source link 28: https://news.skhynix.co.kr/skhynix-ai-memory-2023/

- Source link 29: https://www.asiae.co.kr/article/2024031408180442980

- Source link 30: https://www.joongang.co.kr/article/25330871

- Source link 31: https://www.mordorintelligence.kr/industry-reports/semiconductor-test-equipment-market

- Source link 32: http://snusmic.com/wp-content/uploads/2020/11/171014_%ED%85%8C%ED%81%AC%EC%9C%99_4%ED%8C%80.pdf

- Source link 33: http://snusmic.com/wp-content/uploads/2020/11/150411_%ED%85%8C%ED%81%AC%EC%9C%99_1%ED%8C%80.pdf

- Source link 34: https://securities.miraeasset.com/bbs/maildownload/2014052021191388

- Source link 35: https://kind.krx.co.kr/common/disclsviewer.do?method=search&acptno=20250317000439&docno&viewerhost&

- Source link 36: https://seo.goover.ai/report/202503/go-public-report-ko-d228d9df-0662-4e05-97d2-656e80a75fb0-0-0.html

- Source link 37: https://www.thebigdata.co.kr/view.php?ud=202406250629125184cd1e7f0bdf_23

- Source link 38: https://www.hankyung.com/article/202403279027L

- Source link 39: https://kr.investing.com/news/stock-market-news/article-844916

- Source link 40: https://comp.fnguide.com/SVO2/asp/SVD_shareanalysis.asp?pGB=1&gicode=A089030&cID&MenuYn=Y&ReportGB&NewMenuID=109&stkGb=701

- Source link 41: https://comp.wisereport.co.kr/company/c1070001.aspx?cmp_cd=089030&cn

- Source link 42: https://www.seoulfn.com/news/articleView.html?idxno=210744

- Source link 43: https://www.ibtomato.com/mobile/mView.aspx?no=4033&type=1

- Source link 44: https://core.asiae.co.kr/article/2022071510300874800

- Source link 45: https://money2.creontrade.com/PDF/Out/intranet_data/Product/ResearchCenter/Report/2025/02/52685_MMB_250220.pdf