DEEP RESEARCH · InBody IR Q&A

InBody 2025 Q2 IR Q&A Review

A shareholder inquiry into software revenue, Kort’s capital increase, margins, and operating leverage

0. Bottom line first

The key lines in the IR reply are that the software revenue increase had “no special core factor” and that margins improved in Q3. In other words, software still cannot be called a structural shift, while margin improvement appears to reflect product mix, inventory-cost effects, and lower expenses.

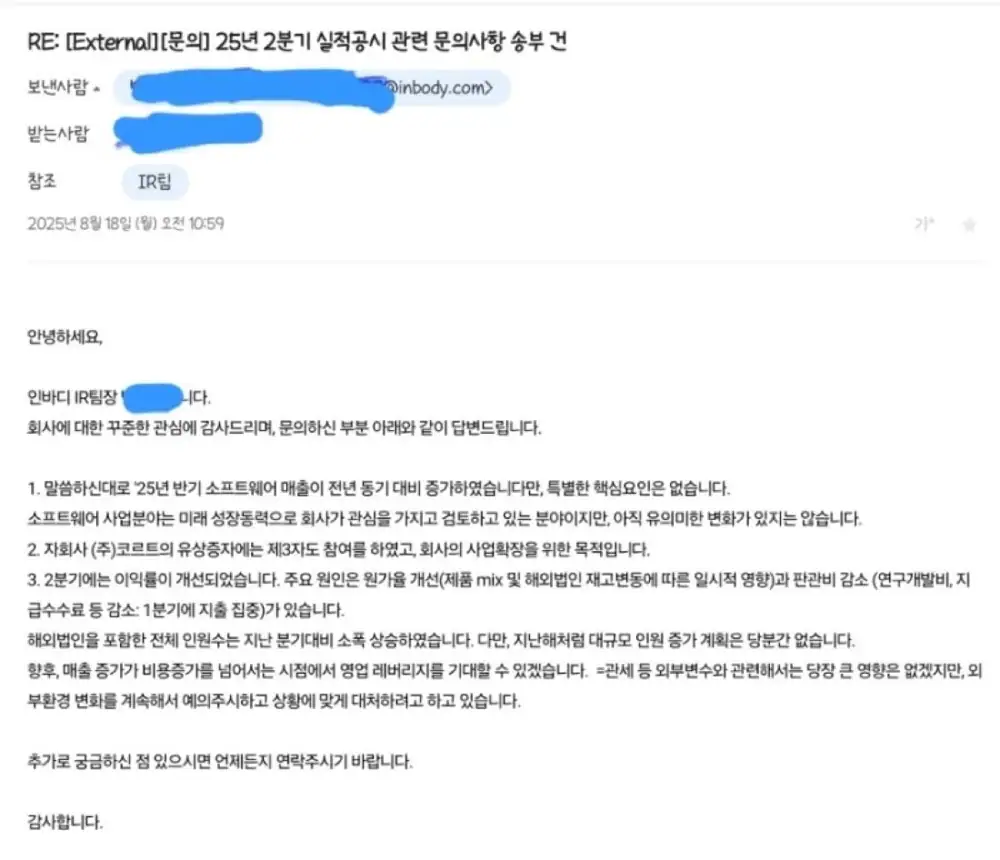

Official fact: The shareholder inquiry was sent to InBody’s IR team at 1:16 PM on August 15, 2025. The attached reply image shows an IR response sent at 10:59 AM on August 18, 2025.

Interpretation: The question is not just growth, but growth quality: whether software becomes recurring revenue, whether external capital for Kort signals scalability, and how headcount, tariffs, and inventory costs affect margins.

1. Software Revenue

Official fact: The shareholder wrote that software revenue had continued growing since Q4 of the prior year, reached new highs, and that Q2 revenue was similar to the prior quarter at about KRW 2.2 billion. The shareholder also asked whether the annual KRW 10 billion target could be achieved.

Official fact: IR replied that first-half 2025 software revenue increased year over year, but there was no special core factor. IR also said software is being reviewed as a future growth driver, but no meaningful change has occurred yet.

Interpretation: I would read this conservatively. The company did not explicitly confirm that subscription models such as Lookin’Body Web or LS Trainer have clearly taken hold, so the next evidence should be revenue persistence, recurring-revenue mix, and customer retention.

Software revenue

The inquiry asked about about KRW 2.2 billion of Q2 revenue and the possibility of reaching the KRW 10 billion annual target.

IR reply

Revenue increased year over year, but IR cited no special core factor and no meaningful change yet.

Watch point

Recurring revenue, subscription-model traction, and quarter-to-quarter durability.

2. Kort Capital Increase

Official fact: The shareholder asked why InBody’s stake in subsidiary Kort fell from 76% to 70% despite InBody contributing KRW 1.7 billion to the capital increase, interpreting this as third-party participation at a larger scale.

Official fact: IR replied that a third party participated in Kort’s capital increase and that the purpose was business expansion.

Interpretation: The stake reduction is dilution, but third-party participation can also be read as external validation of Kort’s business. The answer is short, so investor identity, valuation, and use of proceeds remain follow-up items.

3. Margin And Operating Leverage

Official fact: The shareholder asked whether margin improvement and slight headcount decline suggested the company was entering operating leverage as revenue grows, and how tariffs or other external variables might affect margins.

Official fact: IR replied that Q3 margins improved. The main reasons were gross-margin improvement from product mix and temporary overseas-subsidiary inventory-cost effects, plus lower expenses such as R&D and commissions. Total headcount including overseas subsidiaries rose slightly versus the prior quarter, with no large-scale hiring plan for now. Tariffs and other external variables were not having a large immediate impact, but the company is monitoring the environment.

Interpretation: Operating leverage is possible, but I would not call the margin improvement structural yet. Product mix and overseas inventory costs include temporary elements, so the next check is whether gross margin and SG&A ratios hold.

4. My Follow-Up Questions

- What share of software revenue is subscription revenue, and what is the churn rate?

- Who was the third-party investor in Kort, and at what valuation?

- Which parts of product mix and overseas inventory-cost effects are repeatable?

- If tariff impact is currently limited, what price-pass-through or cost-control policies are prepared?

Sources

- Original Naver Blog post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=223974174181