DEEP RESEARCH · PENSION INVESTING

First-Half Review and Second-Half Investment Strategy

A review of retirement and personal pension management after switching from DB to DC

0. Bottom line first

After switching from DB to DC in March, I traded frequently and now plan to gradually increase U.S. long-duration Treasury exposure into the second half. I am directly managing the DC pension with Samsung Electronics exposure and safe assets, while my personal pension is fully allocated to a VIP Asset Management fund.

1. DC pension: balancing Samsung exposure and safe assets

I currently want more Samsung Electronics exposure, but I do not want to invest in SK Hynix, so I am using a Samsung Group ETF. For the safe-asset sleeve, I am also using bonds that include Samsung Electronics exposure.

I have also added some defense and rechargeable-battery exposure. If those sectors rise and break previous highs, I plan to keep increasing the weights.

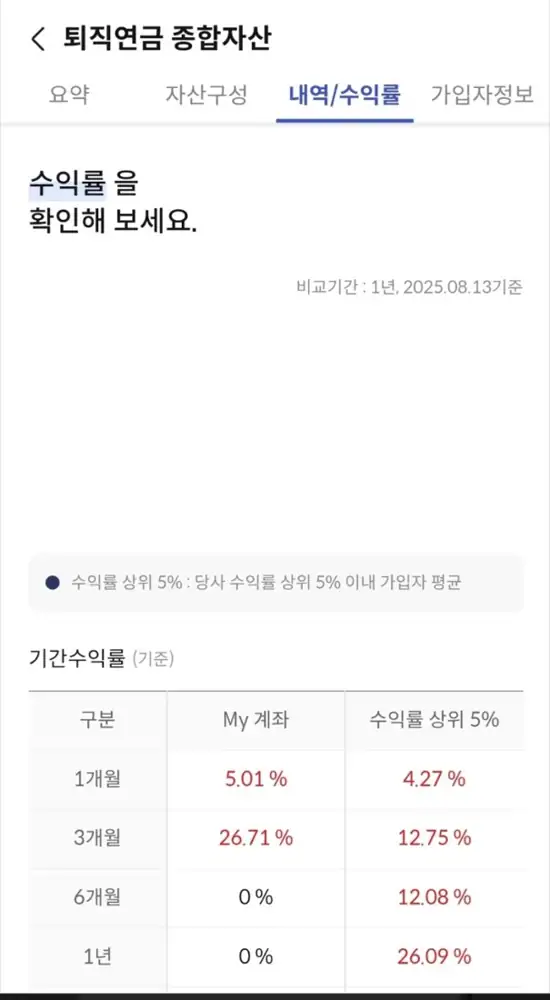

2. Personal pension: all-in VIP fund

My personal pension is 100% allocated to a fund managed by VIP Asset Management. It seems to be doing well versus the market, but I also wonder whether VIP’s past outperformance may have been driven by Samsung Electronics. That is one reason I want a large Samsung Electronics exposure in the DC pension as a hedge.

Of course, I also see a possibility that Samsung Electronics will outperform the market going forward, and it is already a large position in my personal portfolio.

3. Decision rule from here

Interpretation: If VIP continues to outperform my DC pension returns, I plan to move the DC pension to VIP as well. If there are professionals who are better than me, I do not need to manage everything myself.

That said, the DC pension has a 30% bond constraint, so it needs to be viewed differently from the personal pension. A fund is ultimately one of the choices I can select, just like an ETF. As the holder, I need enough sense to review what portfolio the fund owns, because responsibility ultimately sits with the buyer.

VIP Asset Management explains monthly fund status on YouTube. I heard that more than KRW 1 trillion has recently been raised, and I plan to watch whether returns remain strong as assets grow.

Related prior post: All-in VIP Korea Value Investment fund