DEEP RESEARCH · INBODY

InBody 2025 Q2 Earnings Review & Software Revenue

Quarterly checkpoints plus a deep dive on the shift from hardware vendor to SaaS hybrid

0. Bottom line first

The key takeaway from Q2'25 is that InBody is entering the phase where software can plausibly drive the stock. Subscription-based B2B SaaS (LB Trainer, LB Corporate) is in launch prep, the company's data and AI assets are moving from accumulation into monetisation, and the near-term swing factors are the Kort stake change and tariffs.

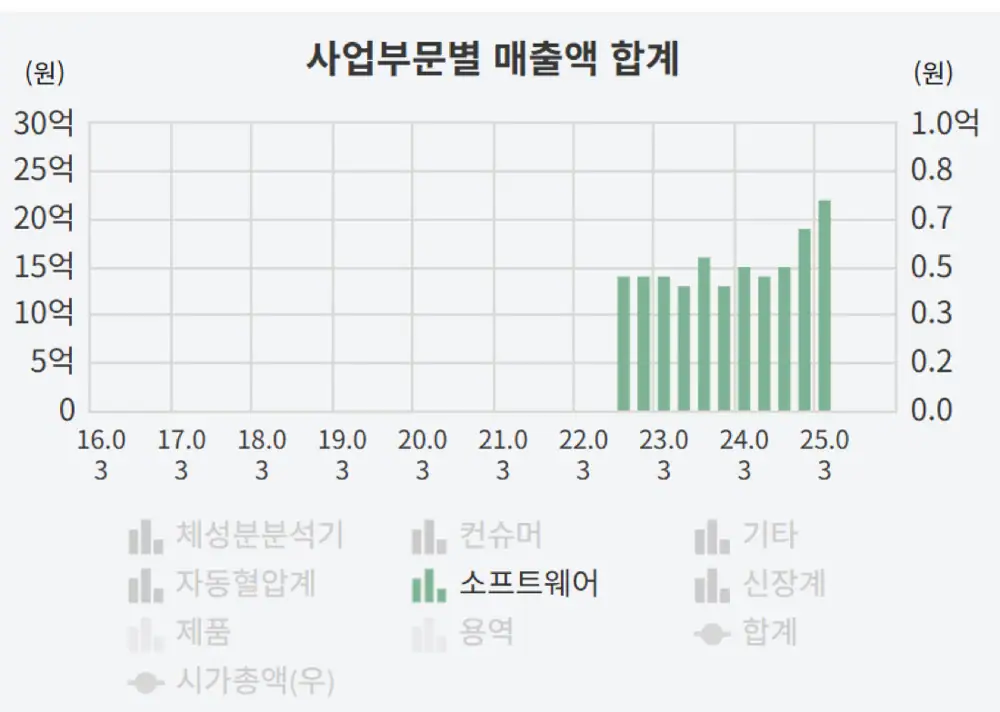

- Software revenue broke a fresh high from Q4'24 onwards; Q2 was again ~KRW 2.2 bn, in line with the full-year ~KRW 10 bn guide. Absent big swings elsewhere, the stock may track software.

- Subsidiary Kort: InBody joined a KRW 1.7 bn capital raise, but its stake fell 76% → 70%, meaning a third party put in even more — motive needs to be clarified (business expansion vs. inheritance planning).

- Margin has turned; with headcount build-out finished, an operating-leverage window is plausible if tariff impact stays contained.

- Headquarter headcount declined.

Q2 ≈ KRW 2.2 bn

Similar to Q1; consistent with the full-year ~KRW 10 bn target.

Stake 76% → 70%

Despite joining the raise, InBody's share fell — a third party took the larger slug. Disclosure clarity needed.

Turn confirmed

Post hiring build-out, possible op-leverage window. Tariffs remain the swing factor.

HQ headcount down

Slimmer overall structure.

1. Strategic summary — from latent potential to active monetisation

Subscription revenue is still small in the P&L today, but the company is at a clear inflection point — an intentional move from a hardware-led model toward a hybrid model that fuses high-margin, recurring software revenue.

- Current state: software ≈3% of revenue, mostly hardware-bundled or one-time licences.

- Catalyst: launch of 'LB Trainer' and 'LB Corporate' — InBody's first formal SaaS push.

- Financial target: brokerage research targets KRW 10 bn in software revenue by 2025–26.

- Foundation: an "unreplicable" body-composition dataset of 100 million+ records, plus a dedicated AI Lab.

- Implication: potential re-rating from a medical-device maker to a data-driven digital-healthcare solutions company.

2. The current software ecosystem — foundation for what's next

Today's software portfolio doesn't lead with explicit subscriptions, but it has been doing three strategic jobs: maximising hardware value, locking users into the ecosystem, and accumulating data.

2.1 Professional B2B: LookinBody Web & iManager

Official fact: LookinBody Web is a cloud-based member/result management platform letting gyms and clinics manage all InBody data from any PC. iManager is a PC-based solution sold as one-time licence / hardware bundle (InBody USA, Mediana).

Interpretation: LookinBody Web is essentially "persistent remote access to customer data" — the core value proposition of B2B SaaS. InBody has been running a proto-SaaS for years; LB Trainer isn't a leap, it's the logical step that monetises the existing cloud layer directly.

2.2 Consumer engagement: InBody app

Official fact: Free consumer app. MAU ~1.4 million; total dataset has crossed 100 million records (Newswire).

Interpretation: No direct revenue, but the funnel that turns one-time hardware buyers into long-term data contributors. The cost of running the app is not a cost centre — it's customer/data acquisition spend for the future SaaS business.

2.3 BodyInsight (hospital solution)

Patient-management software built on InBody outputs, sold bundled with high-end medical devices like the BWA series — a high-value, low-volume model distinct from the broader fitness market.

2.4 Portfolio comparison

| Software | Target market | Core features | Current revenue model (est.) | Strategic role |

|---|---|---|---|---|

| LookinBody Web | Gyms, clinics, pros | Cloud member mgmt, result analysis | HW bundle or one-time licence | Pro ecosystem, data central, base for SaaS |

| InBody app | Home device users (consumers) | Personal tracking, pro linkage | Free | Data funnel, lock-in, brand |

| BodyInsight | Hospitals | Patient health mgmt, nutrition guide | Medical device bundle / institutional licence | Clinical penetration, data, lineup |

| iManager | Pros (PC) | PC-based mgmt & result printing | HW bundle / one-time licence | Legacy PC support |

| InBodyFit+ | Home users | AI personalised health solution | Built into home device | Home-device value add, personalisation |

3. The inflection — explicit subscription launches

3.1 New B2B SaaS: LB Trainer & LB Corporate

Per brokerage reports, InBody is readying 'LB Trainer' (for personal trainers) and 'LB Corporate' (for corporate wellness) as subscription-based B2B apps. These are positioned not as data viewers but as high-value analytics tools that turn raw measurements into actionable insight.

3.2 Numerical targets

| Broker | Date | Year | Est. SW revenue | Driver |

|---|---|---|---|---|

| Kyobo Securities | 2024-01-17 | 2026 | KRW 10 bn | Subscription B2B (LB Trainer / Corporate) launch |

| Shinhan Securities | 2024-06-14 | 2025+ | KRW 10 bn target | Fast growth at SW division (LookinBody) |

Interpretation: The most concrete details (LB Trainer, KRW 10 bn target) appear only in broker reports, while press releases focus on hardware and data. This asymmetry looks like an intentional "investor-first" narrative build before the formal launch.

4. Why software / services

4.1 The "unreplicable" data moat

100 million+ body-composition records; +155% growth 2021→2023; ~85,000 new records/day. The data can only be generated through InBody's market-leading hardware, creating a HW → data → SW → HW-value flywheel.

4.2 AI Lab

Existing AI team elevated to a formal 'AI Lab' working on ML/DL for personalised health management and early disease prediction — covering biosignal processing, computer vision, and NLP. It's the bridge between the raw "100 million data points" and the monetised subscription product (InBody recruiting).

4.3 The industry shift to recurring revenue

Med-tech and digital health are moving from one-off device sales to subscription/service models, which markets reward with higher multiples (KIS: valuation upside).

5. Valuation implications and KPIs

5.1 The re-rating path

Forward 12-month P/E ≈ 9× — the market still treats InBody as a mature hardware company. As software approaches the KRW 10 bn mark, especially as recurring subscription revenue, SOTP valuation or an outright multiple expansion become realistic.

5.2 KPIs to track

SW quarterly growth

Most direct read on execution vs. the KRW 10 bn target.

SW share of total

How fast it expands from ~3%.

SW margin disclosure

Segment-margin breakouts would be the key tell.

Subs / data / hiring

LB Trainer subscribers, data growth beyond 100M, AI-lab hiring.

Conclusion

InBody is at a pivotal moment. Global hardware dominance and a powerful data moat are already in place; the next chapter depends on executing the software / subscription strategy. The next 24 months will be decisive.

Sources

- Original Naver Blog post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=223970954549

- InBody research PDF: ssl.pstatic.net

- Shinhan InBody (041830): static.roa.ai

- Kyobo report briefing (Newspim): newspim.com

- 100M data milestone (Newswire): newswire.co.kr

- 100M data (MedicalTimes): medicaltimes.com

- InBody recruiting: inbodyrecruit.com

- InBody press release (KRW 200 bn): inbody.co.kr

- KIS valuation upside (Yonhap): yna.co.kr

- LookinBody site: lookinbody.com

- LookinBody Web Asia: inbodyasia.com

- LookinBody Web USA: inbodyusa.com

- Sportsmaster InBody guide: sportsmaster.no

- iManager (Mediana): mediana.co.kr

- InBody software download: inbody.co.kr download

- LookinBody Web NL: nl.inbody.com

- InBody home store: inbodyathome.com

- InBody USA: inbodyusa.com

- BodyInsight app: Google Play

- SNUSMIC report: snusmic.com

- InBody KR: inbody.co.kr

- InBody Fit+ launch (K-Health): k-health.com

- Hankyung column: hankyung.com

- KRW 200 bn revenue release: inbody.co.kr

- 100M data (HitNews): hitnews.co.kr

- 100M data (ZDNet Korea): zdnet.co.kr

- Fixed cost / overseas direct sales (HitNews): hitnews.co.kr