DEEP RESEARCH · ASSET ALLOCATION

U.S. Debt Reduction Scenario: Watching for Financial Repression and Tax Shock

A reading of the postwar U.S. debt reduction playbook as a current asset-allocation risk.

0. Bottom line first

The scenario I am most worried about is a government response to high debt that combines higher taxes, tariffs, regulation, suppressed interest rates, and elevated inflation: a new form of financial repression.

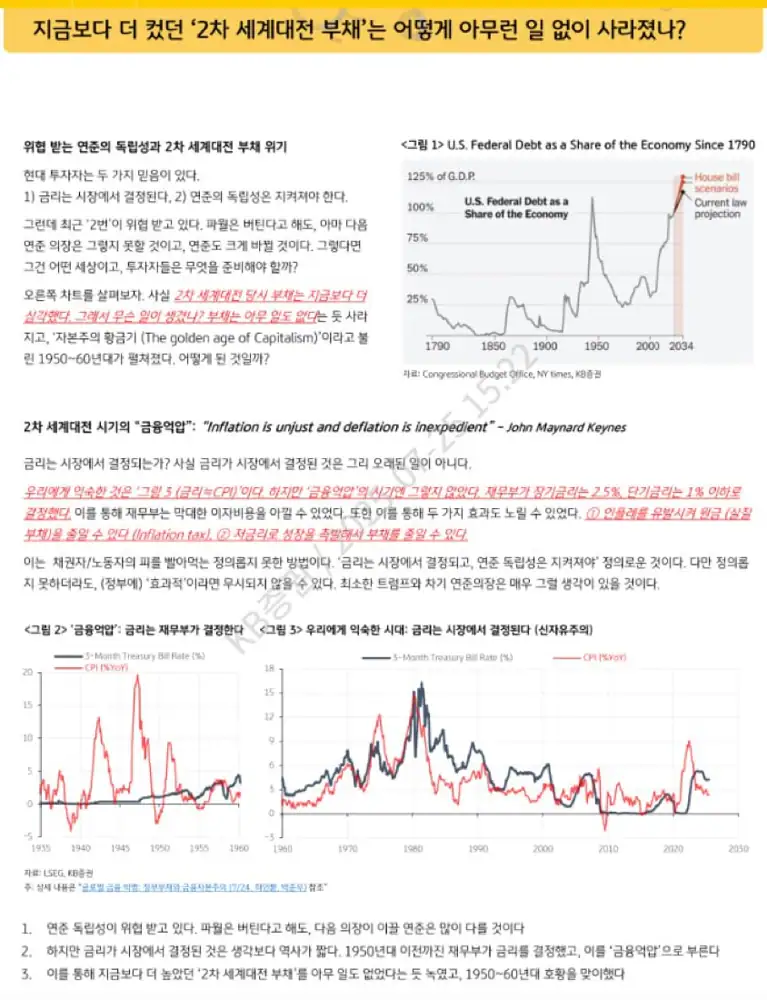

- The KB Securities note links pressure on Fed independence with the pre-1950s history of rate control. Original link: https://bit.ly/3IPfOVn

- For individuals, holding only savings or bonds with yields below inflation may become dangerous.

- The alternative is to review lower exposure to nominal assets and higher exposure to assets that can move with inflation: real estate, commodities, firms with pricing power, TIPS, and long-term fixed-rate debt.

1. Postwar debt did not disappear through growth alone

Official fact: The source notes that U.S. public debt rose from 42% of GDP in 1941 to 106% in 1946, then fell from 106% to 23% between 1946 and 1974.

Official fact: A simulation assuming balanced budgets and no distortion of market interest rates would have reduced the debt ratio only to 74%; the 51 percentage-point gap is attributed to active policy intervention.

Interpretation: The simple r<g story misses the core. Suppressed rates, high nominal growth, inflation, and regulated demand for Treasuries worked together.

2. Tools of financial repression

Official fact: The source discusses the pre-1951 U.S. regime, including a 2.5% long-bond rate peg and the 1951 Treasury-Fed Accord as a key turning point.

| Goal | Post-WWII method | Modern method |

|---|---|---|

| Suppress rates | Explicit Fed rate peg | QE and YCC-style market operations |

| Create captive demand | Regulation Q and capital controls | Basel III, Solvency II, macroprudential rules |

| Direct savings | Direct instructions to banks and pensions | Regulatory and tax incentives for government bonds |

| Policy justification | Postwar government control | Financial stability and market operations |

3. Why the present rhymes

Official fact: The post says U.S. government debt exceeded 120% of GDP after the 2008 crisis and COVID-19, above the WWII peak.

Official fact: It cites IMF work suggesting that when advanced-country government debt exceeds 100% of GDP, banks tend to absorb almost 100% of subsequent incremental debt issuance.

Interpretation: Old repression was explicit. Modern repression is wrapped in stability, regulation, and market operations. The end result can still be lower government borrowing costs and lower real returns for savers.

Nominal assets

If yields are kept below inflation, deposits and long-duration bonds can lose real purchasing power.

Real assets and pricing power

Firms that can pass through costs, real estate, and commodities may offer better defense.

TIPS and debt structure

TIPS provide inflation linkage, while long-term fixed-rate debt can be helped by inflation.

4. My investment note

I am not sure governments will simply allow individuals to avoid the burden. The strategy therefore cannot stop at buying inflation-sensitive assets; it also has to watch tax and regulatory direction.

Attached audio: Audio file on U.S. debt and financial repression

Sources

- Source 1: https://bit.ly/3IPfOVn

- Source 2: https://download.blog.naver.com/open/e87df44f506362d6fd137d4b7198e29230679b1a/EFsQaLdNxrrO9dNRLuoSggWaFwbSq-1Zdlk8M2U90m0pHo-9Vnku6P6-A4hh6ktXohCReWjy-FPzZdetitDY-6dhTWoG8XU5/%EB%AF%B8%EA%B5%AD%20%EB%B6%80%EC%B1%84%EC%9D%98%20%EB%B9%84%EB%B0%80_%20%EA%B8%88%EC%9C%B5%20%EC%96%B5%EC%95%95%EA%B3%BC%20%EB%8B%B9%EC%8B%A0%EC%9D%98%20%EC%9E%90%EC%82%B0%EC%9D%84%20%EC%A7%80%ED%82%A4%EB%8A%94%20%EB%B2%95.mp3

- Source 3: https://cepr.org/voxeu/columns/reassessing-fall-us-public-debt-after-world-war-ii

- Source 4: https://en.wikipedia.org/wiki/History_of_the_United_States_public_debt

- Source 5: https://budget.house.gov/press-release/the-consequences-of-debt

- Source 6: https://www.imf.org/-/media/Files/Publications/WP/2024/English/wpiea2024005-print-pdf.ashx

- Source 7: https://www.wolterskluwer.com/en/expert-insights/whole-ball-of-tax-historical-income-tax-rates

- Source 8: https://inequality.org/article/tax-the-rich-we-did-that-once/

- Source 9: https://taxfoundation.org/data/all/federal/taxes-on-the-rich-1950s-not-high/

- Source 10: https://www.econlib.org/how-did-we-get-good-growth-in-the-1950s-despite-high-marginal-tax-rates/

- Source 11: https://city-countyobserver.com/did-people-really-pay-91-tax-rates-in-the-1950s-if-not-what-was-the-reality-compared-to-today-the-claim-that-the-top-1-of-earners-in-the-1950s-paid-a-91-tax-rate-is-based-on-the-statutory-top-marg/

- Source 12: https://www.federalreservehistory.org/essays/treasury-fed-accord

- Source 13: https://www.imf.org/external/pubs/ft/wp/2015/wp1507.pdf

- Source 14: https://www.weforum.org/stories/2025/03/financial-repression-debt-management/

- Source 15: https://en.wikipedia.org/wiki/Financial_repression

- Source 16: https://www.investopedia.com/terms/m/monetary-accord-1951.asp

- Source 17: https://www.richmondfed.org/publications/research/econ_focus/2021/q1/economic_history

- Source 18: https://d-nb.info/1326277189/34

- Source 19: https://academic.oup.com/book/51884/chapter/420658365/chapter-pdf/52039725/isbn-9780195300727-book-part-6.pdf

- Source 20: https://fraser.stlouisfed.org/timeline/treasury-fed-accord

- Source 21: https://www.levyinstitute.org/pubs/wp_747.pdf

- Source 22: https://www.richmondfed.org/publications/research/goodfriend/plosser

- Source 23: https://www.exploros.com/summary/The-Post-War-Economy-1945-1960

- Source 24: https://library.fiveable.me/key-terms/apush/post-world-war-ii-economic-boom

- Source 25: https://www.thoughtco.com/the-post-war-us-economy-1945-to-1960-1148153

- Source 26: https://www.mercatus.org/research/policy-briefs/economic-recovery-lessons-post-world-war-ii-period

- Source 27: https://www.exploros.com/summary/Economy-in-the-1950s

- Source 28: https://www.cato.org/cato-journal/spring/summer-2018/exit-strategies-monetary-expansion-financial-repression

- Source 29: https://www.pgpf.org/national-debt-clock/

- Source 30: https://cepr.org/voxeu/columns/financial-repression-then-and-now

- Source 31: https://www.chicagobooth.edu/review/how-quantitative-easing-actually-works

- Source 32: https://www.cato.org/sites/cato.org/files/serials/files/cato-journal/2017/5/cj-v37n2-4.pdf

- Source 33: https://river.com/learn/what-is-financial-repression/

- Source 34: https://www.elibrary.imf.org/downloadpdf/journals/022/0048/002/article-A008-en.pdf

- Source 35: https://www.boj.or.jp/en/about/press/koen_2017/data/ko170111a1.pdf

- Source 36: https://www.tcer.or.jp/wp/pdf/e208.pdf

- Source 37: https://medium.com/@girivasishta07/yield-curve-control-the-bank-of-japans-unconventional-monetary-policy-dc04f81e95af

- Source 38: https://www.boj.or.jp/en/research/wps_rev/wps_2024/data/wp24e09.pdf

- Source 39: https://www.imf.org/-/media/Files/Conferences/2024/25th-jacques-polak-annual-research-conference/session-3-jeanne.ashx

- Source 40: https://www.imf.org/-/media/Files/Conferences/2024/Fiscal-Policy-Tokyo/balint-szoke-convenience-yields-and-financial-repression.ashx

- Source 41: https://www.investopedia.com/terms/f/financial-repression.asp

- Source 42: https://www.researchaffiliates.com/publications/articles/542_negative_rates_are_dangerous_to_your_wealth

- Source 43: https://smartasset.com/investing/best-investments-for-inflation

- Source 44: https://www.rbcroyalbank.com/en-ca/my-money-matters/money-academy/investing/investment-strategies-making-the-most-of-lower-interest-rates/

- Source 45: https://treasurydirect.gov/marketable-securities/tips/tips-negative/

- Source 46: https://www.youtube.com/watch?v=ccTinj2DVvg

- Source 47: https://www.investopedia.com/articles/investing/070915/how-negative-interest-rates-work.asp

- Source 48: https://russellinvestments.com/us/blog/impact-low-interest-rates-investors