DEEP RESEARCH · U.S. NATURAL GAS UPSTREAM

The Hidden Trap in the Gas Golden Age: Finding Winners Beyond the Bottleneck

A review of upstream bottleneck control amid LNG, AI power demand, and OBBB tailwinds

0. Bottom line first

Natural gas demand is strengthening through LNG exports and AI data-center power demand, but the winner is not simply the company that produces the most gas. Upstream companies that can control bottlenecks in pipelines, turbines, and capital, and move gas to the final market, are better positioned.

Graphics by Gemini

Official fact: The source says that in the 2025 energy market, energy security after the Russia-Ukraine war made U.S. LNG an essential energy source for Europe and Asia, while AI data-center power demand created new U.S. energy demand.

1. A new energy era and the hidden bottleneck

The 2025 energy market combines energy security, LNG exports, and AI data-center power demand. The OBBB, or One Big Beautiful Bill, is presented as a tailwind for natural gas. The source says the repeal of IRA methane emissions fees reduced production costs and regulatory risk, while early termination of wind and solar tax credits made natural gas-fired power more economically attractive.

Interpretation: At first glance, the whole energy value chain may look like a beneficiary. But the real investment question is the bottleneck. If produced gas cannot move reliably to high-value markets, demand exists but value stays trapped.

2. Bottlenecks: pipelines, turbines, and capital

Geographic constraint

Appalachian gas needs pipeline capacity to reach Gulf Coast LNG terminals and Southeast data-center markets.

Equipment shortage

Gas turbines, critical for gas-fired plants, are described as backed up for years, with deliveries possible only in 2028 or later if ordered now.

Credit and scale

Long-term transport contracts and infrastructure investment require large capital and strong credit ratings.

The Appalachian Basin, especially the Marcellus and Utica shales, is a major U.S. natural gas production region, but it is inland. To move that gas to Gulf Coast LNG export terminals or data-center-heavy Southeast markets, sufficient pipeline capacity is essential. New pipelines require years of permitting and major capital, while existing pipelines can approach saturation.

The bottleneck is not only transportation. Gas-fired plants needed for data-center power demand can also run into gas turbine shortages. The source says global demand has left major turbine manufacturers with years of order backlog, and that orders placed now may not be delivered until 2028 or later. This can delay LNG export or power-plant construction plans.

The final barrier is capital. Long-term pipeline capacity leases and new infrastructure require high credit ratings and large funding capacity. Companies with weak balance sheets may have to sell gas at a discount or cut production.

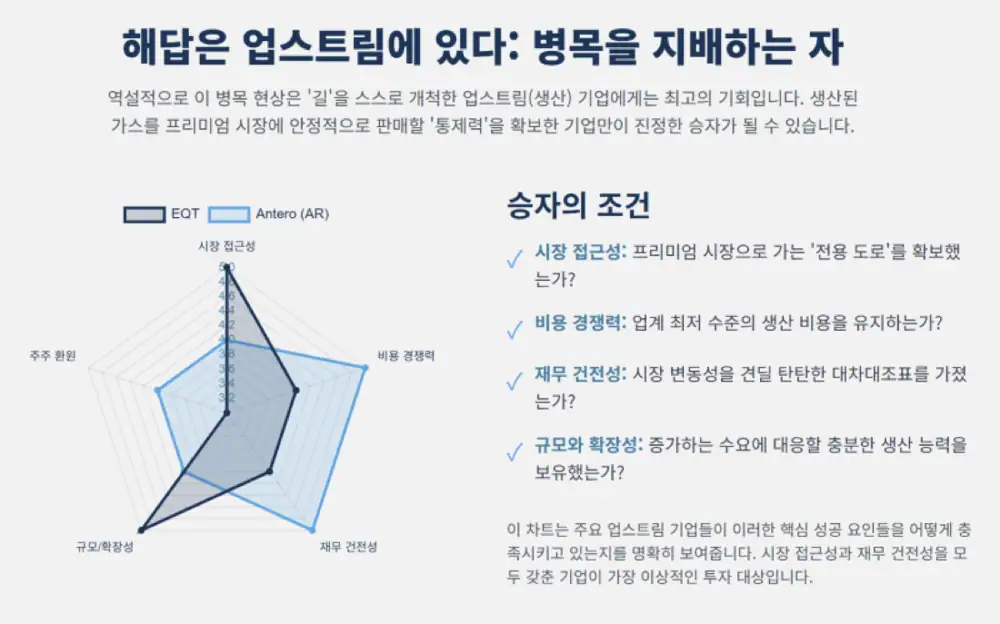

3. Upstream companies that control the bottleneck

Multilayered bottlenecks can become opportunities for certain upstream companies. The winners may be those that control how produced gas is transported and sold into final markets, not simply those with the highest production volume.

| Company | Bottleneck solution | Core logic |

|---|---|---|

| EQT | Physical integration | Equitrans acquisition vertically integrates production and transportation; MVP gives access to premium Southeast markets |

| Antero Resources | Contractual integration | Long-term firm transportation to Gulf Coast LNG export terminals; S&P BBB- investment-grade rating lowers letter-of-credit cost |

| Expand Energy | Scale and diversification | Created by the Chesapeake-Southwestern merger, with assets in both Appalachia and Haynesville |

| Range Resources / CNX Resources | Operating efficiency and financial discipline | Low production costs, free cash flow, debt reduction, and buybacks help withstand volatility |

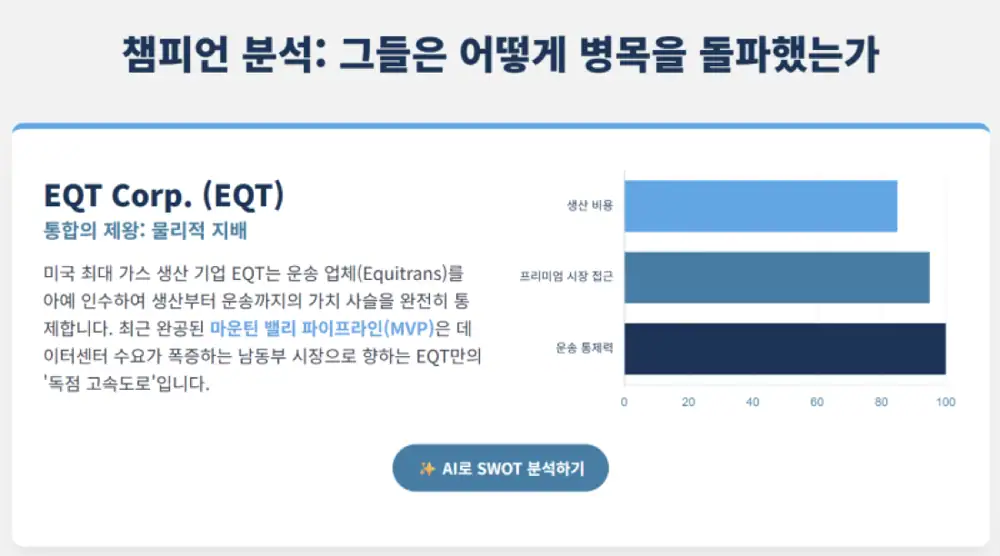

EQT: king of integration

EQT is the largest U.S. natural gas producer and completed vertical integration across production and transportation by acquiring midstream company Equitrans. This reduces dependence on third-party pipelines and lets EQT move its own gas to preferred markets more efficiently and reliably.

The recently completed Mountain Valley Pipeline, or MVP, gives EQT an important advantage. It gives direct access to the premium U.S. Southeast market, where data-center demand is expanding. The source views this as a competitive advantage that solves the geographic bottleneck and maximizes the value of production.

Antero Resources: master of contracts

Antero Resources uses contractual integration. It has secured pipeline capacity to Gulf Coast LNG export terminals through long-term firm transportation contracts, creating a dedicated highway for its gas and NGLs to reach premium markets.

Official fact: The source says Antero recently received an investment-grade BBB- rating from S&P. This is a financial bottleneck solution because it lowers letter-of-credit costs needed to maintain large transport contracts and reduces overall financing cost.

Strong alternatives: EXE, RRC, and CNX

Expand Energy, created by the merger of Chesapeake and Southwestern, is positioned around scale and diversification. It owns core assets not only in Appalachia but also in Haynesville, near the Gulf Coast LNG export hub, reducing exposure to a single region’s pipeline problem. The source also points to investment-grade ratings from all major credit agencies as a financial strength.

Range Resources and CNX Resources compete through operating efficiency and financial health. They use free cash flow generated from low production costs for debt reduction and share buybacks. The source specifically records that CNX has generated free cash flow for 21 consecutive quarters.

4. Final judgment

The natural gas golden age opened by the OBBB is attractive, but the fruits of the opportunity are more likely to accrue to companies that have secured routes to deliver value to final markets, not just companies that produce value.

The point is not to buy the LNG or data-center theme in the abstract. I need to focus on upstream companies with the strategy and execution capability to overcome pipeline bottlenecks, infrastructure shortages, and capital barriers.

Interpretation: EQT’s physical integration and Antero Resources’ contractual integration look like the clearest alternatives. Expand Energy has scale and diversification, while Range Resources and CNX Resources have financial discipline and efficiency. In the end, the winner in the new energy era may not be the company that produces the most gas, but the one that knows the most reliable route.

Sources

- Reference 1 · m.blog.naver.com: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=223929284175

- Reference 2 · eenews.net: https://www.eenews.net/articles/3-questions-answered-on-the-ukraine-wars-impact-on-energy/

- Reference 3 · iea.org: https://www.iea.org/topics/russias-war-on-ukraine

- Reference 4 · eastdaley.com: https://eastdaley.com/burner-tip/data-centers-could-add-6-bcf-d-to-gas-demand-eda-forecast#:~:text=Infrastructure%20%E2%80%93%20The%20data%20center%20industry,GW%20of%20new%20power%20capacity.

- Reference 5 · eastdaley.com: https://eastdaley.com/media-and-news/data-centers-voracious-power-demand-drives-gas-renaissance

- Reference 6 · eastdaley.com: https://eastdaley.com/burner-tip/data-centers-could-add-6-bcf-d-to-gas-demand-eda-forecast

- Reference 7 · utilitydive.com: https://www.utilitydive.com/news/artificial-intelligence-doubles-data-center-demand-2030-EPRI/717467/

- Reference 8 · news.oilandgaswatch.org: https://news.oilandgaswatch.org/post/congress-repeals-oil-and-gas-methane-pollution-fee-costing-taxpayers-7-2-billion

- Reference 9 · instituteforenergyresearch.org: https://www.instituteforenergyresearch.org/regulation/summary-of-key-provisions-in-the-one-big-beautiful-bill-act/

- Reference 10 · akingump.com: https://www.akingump.com/en/insights/alerts/significant-cuts-to-ira-clean-energy-tax-credits-included-in-enacted-reconciliation-bill

- Reference 11 · stoel.com: https://www.stoel.com/insights/publications/the-one-big-beautiful-bill-modifies-renewable-energy-tax-credits

- Reference 12 · rinnovabili.net: https://www.rinnovabili.net/business/utilities/gas-turbine-supply-chain-under-pressure/

- Reference 13 · woodmac.com: https://www.woodmac.com/press-releases/despite-surging-power-demand-gas-fired-power-faces-manufacturing-constraints-that-could-limit-near-term-growth/

- Reference 14 · heatmap.news: https://heatmap.news/ideas/natural-gas-turbine-crisis

- Reference 15 · turbomachinerymag.com: https://www.turbomachinerymag.com/view/wtui-2025-spotlights-uptick-in-gas-turbine-orders

- Reference 16 · kunc.org: https://www.kunc.org/news/2025-07-06/after-coal-a-debate-in-colorado-over-proposed-new-natural-gas-electricity-generation

- Reference 17 · anteroresources.com: https://www.anteroresources.com/investors/press-releases/detail/237/antero-resources-receives-investment-grade-credit-rating

- Reference 18 · ir.eqt.com: https://ir.eqt.com/investor-relations/overview/default.aspx

- Reference 19 · prnewswire.com: https://www.prnewswire.com/news-releases/antero-resources-receives-investment-grade-credit-rating-302146878.html