DEEP RESEARCH · REFINING/CHEMICALS/COAL

Is the U.S. Coal Era Returning? OBBB, AI Power Demand, and METC

Why U.S. energy-dominance policy and data-center electricity demand put coal back on the watchlist

0. Bottom line first

The source view is clear: after OBBB, the U.S. is moving toward domestic energy foundations such as oil, coal, gas, and nuclear rather than renewables dependent on non-U.S. supply chains. AI data-center power demand is pushing that shift. Among coal names, Ramaco Resources (METC) stands out because it combines coal with a rare-earth/critical-minerals option.

1. Policy Background: Shift to Energy Dominance

Official fact: The source says OBBB became law on July 4, 2025 and frames it as a shift away from IRA-style green incentives toward an energy-dominance policy.

Interpretation: The author's read is that renewables without U.S. value chains will receive less support, while oil, coal, gas, and nuclear receive more policy backing. The goal is to exclude China-linked materials while still mobilizing any available energy source for AI data centers.

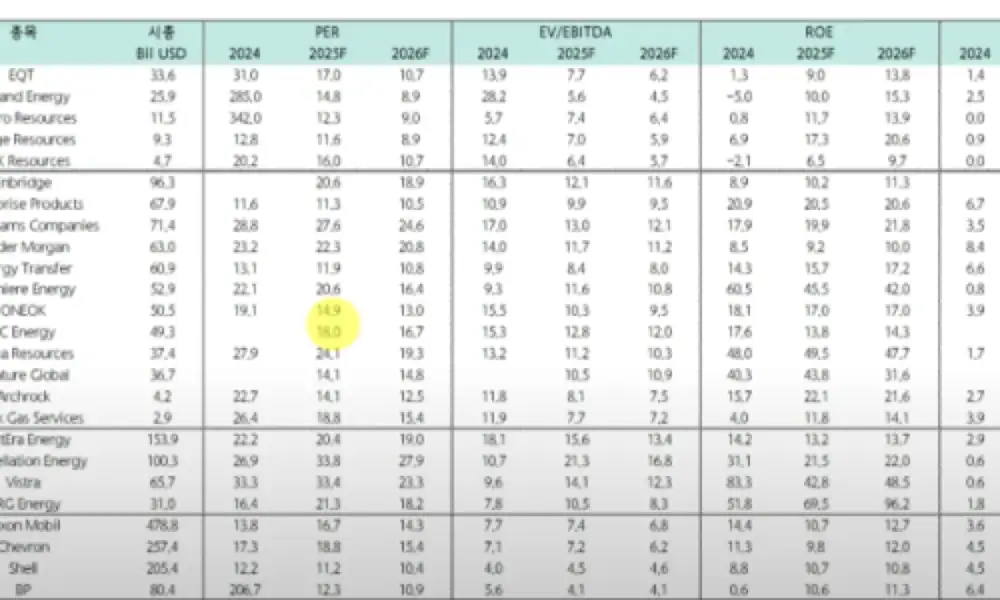

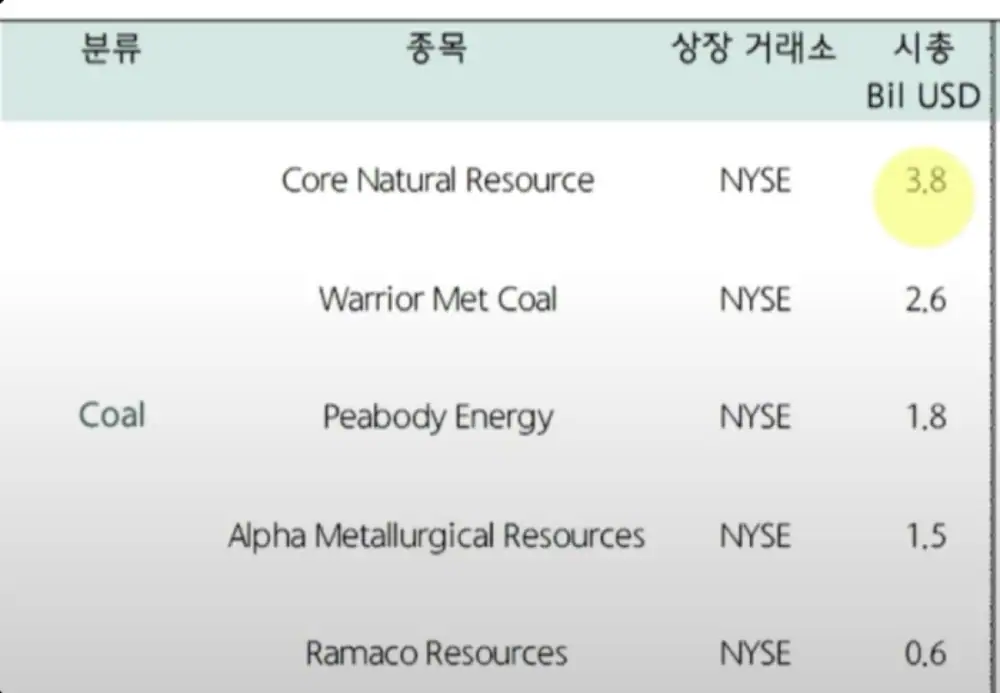

2. Comparison Set: Five U.S. Coal Producers

Official fact: The source compares Core Natural Resources (CNR), Warrior Met Coal (HCC), Peabody Energy (BTU), Alpha Metallurgical Resources (AMR), and Ramaco Resources (METC).

| Company | Source positioning | Key question |

|---|---|---|

| CNR | Large coal-based company | Scale and export exposure |

| HCC | Metallurgical coal focus | Price sensitivity and cost structure |

| BTU | Traditional large coal producer | Policy upside and asset mix |

| AMR | Metallurgical coal producer | Steel cycle and cash flow |

| METC | Coal plus rare-earth dual play | Brook Mine critical-minerals option |

3. Why METC

Official fact: The source concludes that Ramaco Resources (METC) is the most attractive candidate because it combines a low-cost metallurgical coal business with a strategically important rare-earth and critical-minerals project.

Interpretation: METC is not just a coal-price bet. It is a dual play on industrial raw-material demand and U.S. national-security priorities. Among long-declining U.S. coal names, the attached emerging-minerals and rare-earth project is the differentiator.

Cash-flow base

Metallurgical coal provides the operating foundation.

Asymmetric option

Brook Mine's critical-minerals project acts as a separate catalyst.

Supply-chain security

Aligned with U.S. critical-minerals independence.

4. Risks and Checks

- Whether OBBB policy direction turns into real subsidies and demand.

- Whether AI data-center power demand is strong enough to support coal-fired power retention or expansion.

- How long gas and nuclear bottlenecks persist.

- Whether METC's rare-earth project advances from preliminary assessment to commercialization.

- Whether investors can bear coal-price cycles and environmental/regulatory risk.

Official fact: The source includes a related Naver Blog link and a Gemini audio file: U.S. manufacturing revival note, U.S. coal company investment audio.

Sources

- Original/reference link 1: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=223929188231

- Original/reference link 2: https://m.blog.naver.com/star_of_self/223928964677

- Original/reference link 3: https://download.blog.naver.com/open/c055dc6f7c2d24f8d5355a645ebec3be1d40bf5c02/EFsQaLdNxb_O8NI2E-QRigSVEg-Y7dtnemsQLWUj_gMvHIi_V3gk7_e7CIIOzyQjqwirblrvu365EgOlh8vZpCJ2_Yi8nZw/%EB%AF%B8%EA%B5%AD%20%EC%84%9D%ED%83%84%20%EA%B8%B0%EC%97%85%20%ED%88%AC%EC%9E%90_%20OBBB%20%EB%B2%95%EC%95%88%2C%20AI%20%EC%A0%84%EB%A0%A5%EB%82%9C%2C%20%EA%B7%B8%EB%A6%AC%EA%B3%A0%20%EB%9D%BC%EB%A7%88%EC%BD%94%EC%9D%98%20%27%ED%9D%AC%ED%86%A0%EB%A5%98%2B%EC%84%9D%ED%83%84%27%20%EB%93%80%EC%96%BC%20%EC%97%94%EC%A7%84%20%EB%B6%84%EC%84%9D.mp3

- Original/reference link 4: https://www.whitehouse.gov/articles/2025/07/president-trumps-one-big-beautiful-bill-is-now-the-law/

- Original/reference link 5: https://www.calt.iastate.edu/blogpost/one-big-beautiful-bill-implements-significant-tax-package

- Original/reference link 6: https://frostbrowntodd.com/one-big-beautiful-bill-act-cuts-the-power-phase%E2%80%91outs-foreign%E2%80%91entity-restrictions-and-domestic-content-in-clean%E2%80%91energy-credits/

- Original/reference link 7: https://www.instituteforenergyresearch.org/regulation/summary-of-key-provisions-in-the-one-big-beautiful-bill-act/

- Original/reference link 8: https://timesofindia.indiatimes.com/world/us/biggest-bill-ever-signed-donald-trumps-first-comments-after-big-beautiful-bill-passes-us-congress/articleshow/122238190.cms

- Original/reference link 9: https://www.kbkg.com/feature/house-passes-tax-bill-sending-to-president-for-signature

- Original/reference link 10: https://www.nerdwallet.com/article/taxes/ev-tax-credit-electric-vehicle-tax-credit

- Original/reference link 11: https://apnews.com/article/congress-clean-energy-climate-environment-trump-tax-bill-19b13a47fbb671218ee59ab9da136478

- Original/reference link 12: https://www.irs.gov/credits-deductions/credits-for-new-clean-vehicles-purchased-in-2023-or-after

- Original/reference link 13: https://www.energysage.com/news/congress-passes-bill-ending-residential-solar-tax-credit/

- Original/reference link 14: https://www.utilitydive.com/news/senate-house-ira-cuts-tax-credits-budget-bill-wind-solar-trump/751032/

- Original/reference link 15: https://www.greenlancer.com/post/solar-tax-credit-going-away

- Original/reference link 16: https://www.solar.com/learn/trump-and-the-fate-of-the-30-solar-tax-credit/

- Original/reference link 17: https://www.energystar.gov/about/federal-tax-credits

- Original/reference link 18: https://www.akingump.com/en/insights/alerts/significant-cuts-to-ira-clean-energy-tax-credits-included-in-enacted-reconciliation-bill

- Original/reference link 19: https://www.projectfinance.law/publications/2025/july/effects-of-one-big-beautiful-bill-on-projects/

- Original/reference link 20: https://www.huschblackwell.com/newsandinsights/energy-tax-credit-framework-undergoes-further-changes-in-senate-approved-version-of-obbb-act

- Original/reference link 21: https://theicct.org/pr-ira-repeal-threatens-130000-american-jobs-by-2030/#:~:text=Since%20the%20passage%20of%20the,law%27s%20key%20provisions%20were%20repealed.

- Original/reference link 22: https://www.americanprogress.org/article/chaos-reigns-gambling-the-future-of-american-manufacturing/

- Original/reference link 23: https://e2.org/releases/100000-clean-energy-manufacturing-jobs-announced-since-ira-companies-add-1500-new-jobs-in-april/

- Original/reference link 24: https://theicct.org/publication/how-the-ira-is-driving-us-job-growth-across-the-electric-vehicle-industry-apr25/

- Original/reference link 25: https://theicct.org/pr-ira-repeal-threatens-130000-american-jobs-by-2030/

- Original/reference link 26: https://www.opb.org/article/2025/06/27/cutting-tax-credits-could-threaten-american-solar-manufacturing/

- Original/reference link 27: https://nationalinterest.org/blog/energy-world/how-the-united-states-can-outcompete-china-in-energy-dominance-and-environmental-progress

- Original/reference link 28: https://www.energypolicy.columbia.edu/events/impact-russia-ukraine-war-global-commodity-markets-and-energy-transition/

- Original/reference link 29: https://www.brickergraydon.com/insights/publications/Inflation-Reduction-Act-IRA-Advanced-Manufacturing-Product-Credit-A-cheat-sheet

- Original/reference link 30: https://iratracker.org/programs/ira-section-13502-advanced-manufacturing-production-credit-for-solar-and-wind-manufacturers/

- Original/reference link 31: https://www.congress.gov/crs-product/IF12809

- Original/reference link 32: https://www.barr.com/Insights/Insights-Article/ArtMID/1344/ArticleID/454/The-Inflation-Reduction-Act-Manufacturing-focus

- Original/reference link 33: https://www.irs.gov/credits-deductions/advanced-manufacturing-production-credit

- Original/reference link 34: https://www.irs.gov/newsroom/treasury-irs-issue-final-regulations-for-the-advanced-manufacturing-production-credit

- Original/reference link 35: https://heatmap.news/ideas/natural-gas-turbine-crisis

- Original/reference link 36: https://www.rcrwireless.com/20250612/energy/eia-power-ai-data

- Original/reference link 37: https://www.epri.com/about/media-resources/press-release/q5vu86fr8tkxatfx8ihf1u48vw4r1dzf

- Original/reference link 38: https://www.prnewswire.com/news-releases/epri-study-data-centers-could-consume-up-to-9-of-us-electricity-generation-by-2030-302157970.html

- Original/reference link 39: https://www.eia.gov/todayinenergy/detail.php?id=65564

- Original/reference link 40: https://onlocationinc.com/news/2025/07/aeo-2025-trends-growing-electricity-demand-from-data-centers/

- Original/reference link 41: https://www.utilitydive.com/news/artificial-intelligence-doubles-data-center-demand-2030-EPRI/717467/

- Original/reference link 42: https://www.semafor.com/article/03/17/2025/gas-turbine-manufacturers-bet-ai-boom-trump

- Original/reference link 43: https://rmi.org/gas-turbine-supply-constraints-threaten-grid-reliability-more-affordable-near-term-solutions-can-help/

- Original/reference link 44: https://www.kunc.org/news/2025-07-06/after-coal-a-debate-in-colorado-over-proposed-new-natural-gas-electricity-generation

- Original/reference link 45: https://www.turbomachinerymag.com/view/wtui-2025-spotlights-uptick-in-gas-turbine-orders

- Original/reference link 46: https://www.turbomachinerymag.com/view/gas-turbine-market-report-2024-posts-highest-units-mws-in-22-years

- Original/reference link 47: https://gasturbinehub.com/the-growing-backlog-of-gas-turbine-orders-implications-for-customers/

- Original/reference link 48: https://www.woodmac.com/press-releases/despite-surging-power-demand-gas-fired-power-faces-manufacturing-constraints-that-could-limit-near-term-growth/

- Original/reference link 49: https://www.rinnovabili.net/business/utilities/gas-turbine-supply-chain-under-pressure/

- Original/reference link 50: https://bipartisanpolicy.org/explainer/unpacking-the-feoc-provisions-in-the-senate-finance-reconciliation-bill/

- Original/reference link 51: https://legal-planet.org/2024/09/24/understanding-chinas-national-energy-security-strategy/

- Original/reference link 52: https://www.iiss.org/online-analysis/online-analysis/2025/07/from-national-security-to-strategic-leverage/

- Original/reference link 53: https://www.scielo.br/j/cint/a/6sVgMgTtdYJqHPH88fytnXx/?lang=en

- Original/reference link 54: https://www.mercomindia.com/chinas-dominance-in-critical-minerals-supply-and-refining-continues-iea

- Original/reference link 55: https://timesofindia.indiatimes.com/business/international-business/iea-warns-of-growing-global-dependence-on-few-nations-for-critical-minerals-highlights-chinas-dominance/articleshow/121319416.cms

- Original/reference link 56: https://www.thirdway.org/memo/fully-fueled-strengthening-americas-nuclear-toolkit

- Original/reference link 57: https://www.iaea.org/bulletin/fuelling-the-future-building-fuel-supply-chains-for-smrs-and-advanced-reactors

- Original/reference link 58: https://www.youtube.com/watch?v=TmcBA4o_Yqs

- Original/reference link 59: https://www.stimson.org/2024/disruption-and-the-nuclear-industry/

- Original/reference link 60: https://www.ans.org/news/2025-05-29/article-6956/filling-technical-gaps-and-fueling-the-advancing-nuclear-supply-chain-at-srnl/

- Original/reference link 61: https://ramacoresources.com/investors/

- Original/reference link 62: https://www.prnewswire.com/news-releases/update-on-independent-preliminary-economic-assessment-report-from-fluor-corporation-302500549.html

- Original/reference link 63: https://corenaturalresources.com/

- Original/reference link 64: https://www.stocktitan.net/sec-filings/CNR/

- Original/reference link 65: https://investors.corenaturalresources.com/2025-02-20-Core-Natural-Resources-Reports-Fourth-Quarter-2024-Results

- Original/reference link 66: https://investors.corenaturalresources.com/2025-02-20-Core-Natural-Resources-Reports-Fourth-Quarter-2024-Results?asPDF

- Original/reference link 67: https://quartr.com/companies/warrior-met-coal-inc_3753

- Original/reference link 68: https://www.alphaspread.com/security/nyse/hcc/investor-relations

- Original/reference link 69: https://www.webull.com/news/12306614043244544

- Original/reference link 70: https://www.investing.com/equities/warrior-met-coal-inc

- Original/reference link 71: https://www.alphaspread.com/security/nyse/btu/investor-relations

- Original/reference link 72: https://www.tradingview.com/news/tradingview:5be524cff8079:0-peabody-energy-corp-sec-10-k-report/

- Original/reference link 73: https://minedocs.com/28/Peabody-Energy-10-K-2024.pdf

- Original/reference link 74: https://www.prnewswire.com/news-releases/peabody-reports-results-for-the-quarter-and-year-ended-december-31-2024-302369546.html

- Original/reference link 75: https://quartr.com/companies/alpha-metallurgical-resources-inc_6378

- Original/reference link 76: https://www.tradingview.com/news/tradingview:5ab4124e97484:0-alpha-metallurgical-resources-inc-sec-10-k-report/

- Original/reference link 77: https://www.publicnow.com/view/B1BE6AAF6688AFA1BD1F401DBFFB8E654CA67D13?1740750381

- Original/reference link 78: https://investors.alphametresources.com/investors/default.aspx

- Original/reference link 79: https://ramacoresources.com/wp-content/uploads/2022/05/Annual-Report-2021-Final.pdf

- Original/reference link 80: https://www.tradingview.com/news/tradingview:5e0d207418193:0-ramaco-resources-inc-sec-10-k-report/

- Original/reference link 81: https://www.peabodyenergy.com/