DEEP RESEARCH · OIL/CHEMICALS & ENERGY POLICY

The Revival of U.S. Manufacturing Is Coming: Energy Policy and Oil/Chemicals Ideas

A note connecting China’s cleantech production dominance, U.S. IRA tax changes, refining margins, and carbon capture

0. Bottom line first

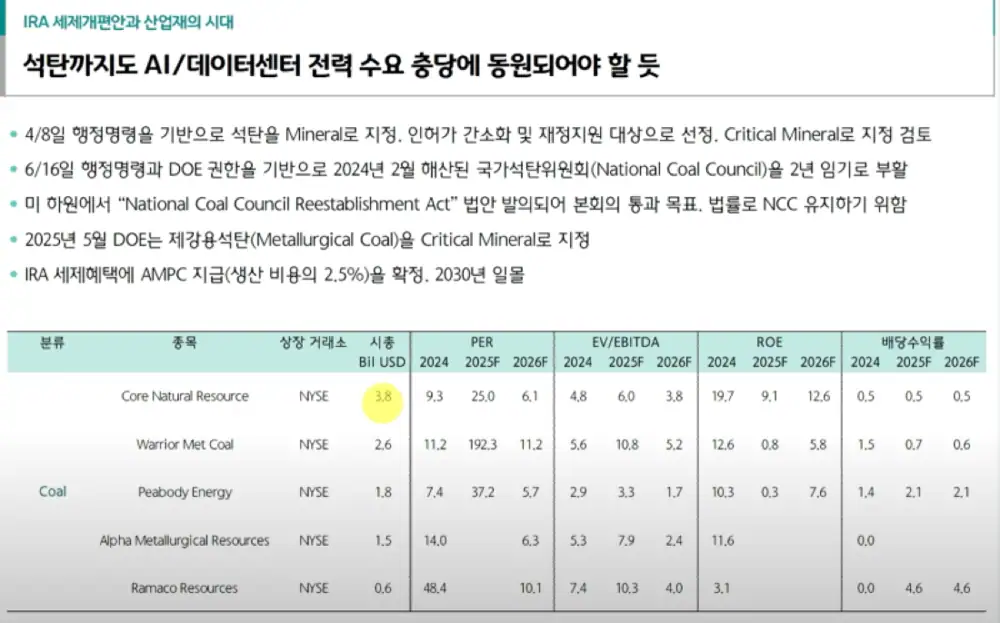

My conclusion is that the next investment ideas may lead toward Chinese solar and U.S. coal/refining names. The two-track strategy matters: the U.S. keeps its fossil-fuel base while expanding nuclear and carbon capture, while China has to push renewables to reduce coal dependence.

The reference video is https://youtu.be/OwUOP8MsL3A?si=bfj1KSxoY5TzGMbY.

1. China’s dominant cleantech production share

Official fact: According to the source summary, China accounts for 74% of solar, 55% of wind, 64% of batteries, and 64% of electrolyzers in cleantech production. The U.S. production share is described as very low.

Solar 74%

The largest China production share mentioned in the post.

Wind 55%

China is also described as holding more than half of wind production.

Batteries 64%

A core production base for the EV and ESS value chains.

Electrolyzers 64%

Linked to hydrogen and clean-fuel infrastructure.

Interpretation: For the U.S., expanding renewables still leaves an energy-security question if the core equipment production base sits in China. This is more about supply-chain restructuring than a simple green-policy debate.

2. Meaning of IRA tax changes

The post divides the IRA tax changes into benefit cuts, partial easing, maintained benefits, and expanded benefits. The end of EV tax credits and the sunset of residential solar installation credits are categorized as cuts, while AMPC production credits and nuclear credits are maintained.

| Category | Content | Investment view |

|---|---|---|

| Reduced | End of EV tax credit, sunset of residential solar installation credit | Potentially weaker support for EV and residential solar demand |

| Maintained | AMPC production credit, nuclear tax credit | Policy support for battery/solar factories and nuclear power |

| Expanded | Favoring U.S.-based supply chains, stopping producer subsidies to Chinese firms | A signal toward building supply chains excluding China |

| Added | Carbon capture, clean fuel, special deductions for oil/gas/coal companies | A combination of fossil fuels and low-carbon technology |

Interpretation: The nuclear tax credit sunset in 2036 shows U.S. intent to secure long-term power supply. The end of subsidies for Chinese firms also favors companies with U.S. supply chains.

3. The three-week window and the energy two-track

The three-week period in President Trump’s letter may signal willingness to negotiate. But the post also warns that if no strategic agreement is reached within that window, the global economy could cool, using Germany’s sharp drop in exports to the U.S. as a cautionary example.

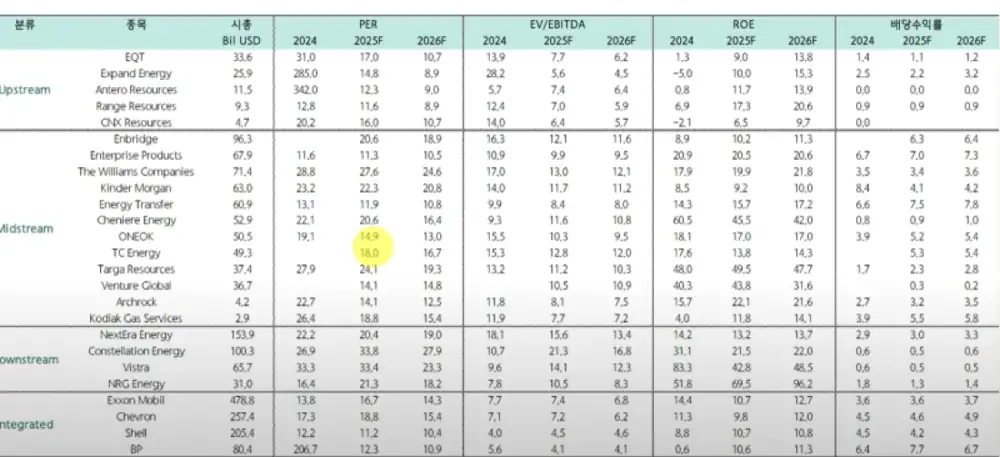

4. Investment ideas: solar, nuclear, refining, carbon capture

For the U.S. market, solar is described as necessary in the short term, while nuclear investment is attractive over the longer term. The post suggests building an energy portfolio that combines stable dividend names with higher-growth names.

For China, solar stocks could rise as EV companies grow. Top-tier solar companies that survive restructuring may become competitive investment candidates.

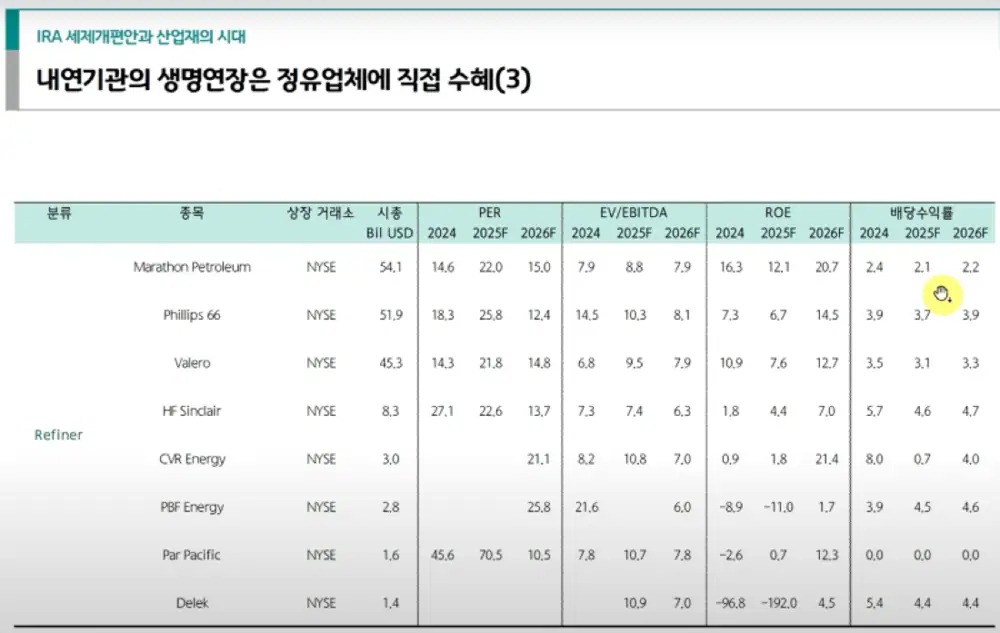

Official fact: The post says U.S. refinery utilization is at 95%, effectively full operation; inventories are at a 20-year low; and both U.S. and Asian refining margins are at one-year highs.

Interpretation: If refinery expansion is difficult while utilization and inventories are tight, refining margins can stay high. Even EV investors may consider adding internal-combustion-related refiners as a portfolio complement.

Carbon capture is framed as an essential technology supporting the Trump administration’s energy policy because it can capture carbon dioxide from gas power plants and oil production processes.

Sources

- Original Naver Blog post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=223928964677

- Video: https://youtu.be/OwUOP8MsL3A?si=bfj1KSxoY5TzGMbY