DEEP RESEARCH · PARK SYSTEMS (KOSDAQ 140860)

Park Systems — A Company With a Moat, and Its Recent Capex Moves

The global AFM #1's 'technological trinity' moat and the Gwacheon–Yongin–Uiwang R&D/production triangle — what 2025 Q1 +98% YoY really means

0. Bottom Line First

Park Systems has been aggressively scaling — not only via organic capex but also through international M&A, which is rare for a Korean mid-cap. Dominant tech, a strong outside-director bench, and the savvy to acquire foreign technology leaders. The current semis cycle is light on front-end capex (so equipment exposure is thin), but back-end packaging keeps expanding, and metrology/inspection capex continues. My H2 watchlist: Leeno Industrial, Park Systems, Samsung (already invested).

- 2025 Q1 revenue ₩50.9B (+98% YoY), operating profit ₩13.2B (+2,540% YoY), OPM 25.9% — operating leverage in full effect.

- 2023 global AFM share 20.3% — #1 (vs Bruker 18.8%); industrial AFM share ~80% — effectively a monopoly.

- EUV mask repair (NX-Mask) + hybrid-bonding CMP metrology (NX-Hybrid WLI) — management guides hybrid-bonding revenue to exceed 40% of sales within 3 years.

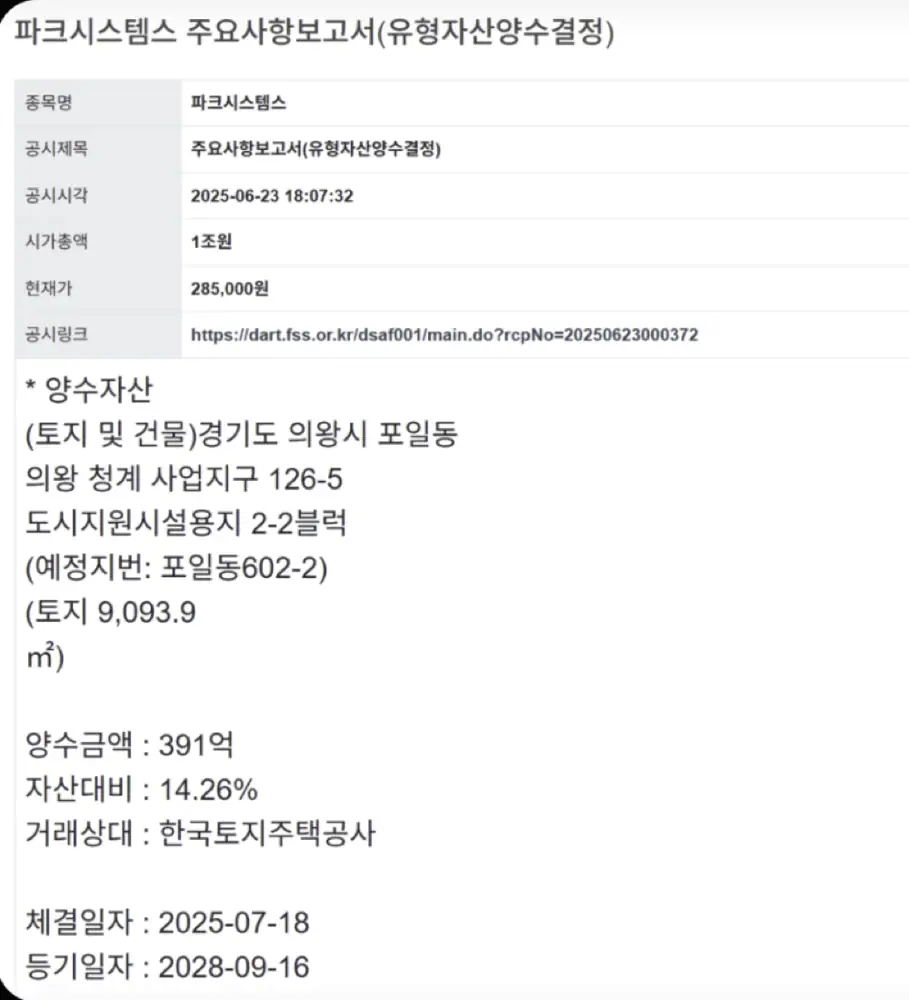

- On 2025-06-23 the company disclosed an acquisition of a 9,093.9 ㎡ land plot in Uiwang for ₩39.1B from LH — completing the 'Gwacheon–Yongin–Uiwang R&D/production triangle' (Gwacheon HQ ₩64.1B, occupancy H1 2026; Yongin inside SK hynix's 120T+ KRW cluster).

Author's earlier write-up — [Park Systems] Primer #1.

1. Company Overview — A 'National Core Technology' Holder, Global AFM Leader

- Founded 1997 by Sang-il Park, originally a member of the Stanford applied-physics group that invented the AFM. He later founded Park Scientific Instruments in Silicon Valley — the world's first commercial AFM company.

- KOSDAQ-listed in 2015 with the top tech-evaluation grade 'AA.'

- AFM manufacturing technology is designated a 'National Core Technology' by Korea's MOTIE.

- Overtook Bruker for #1 global AFM share in 2022. 2023 share 20.3%, industrial AFM ~80%.

2. The Moat — A 'Technological Trinity'

What competitors cannot copy quickly is not a single feature but physics + mechanical design + AI software bound into a system-level moat.

True Non-Contact™

Tip and sample never touch; the tool maintains a few-nm gap and reads van der Waals attraction via Z-servo feedback. Eliminates tip wear and sample damage → lower TCO, and delivers 72 hours of continuous imaging with no parameter re-tuning.

Decoupled XY-Z Scanner

Removes 'scanner bow' and XY-Z crosstalk that plague traditional single-tube AFMs. A flat 2D flexure XY scanner + independent Z scanner deliver flat, accurate 3D images without software correction, plus fast Z response.

SmartScan™ — Switching-Cost Lock-In

QR-coded automatic tip swap, FastApproach™ (<10 s tip approach), AdaptiveScan™ (speed varies with topography). Customer recipes and analysis workflows are deeply integrated — switching to a competitor means rebuilding everything.

Official fact: True Non-Contact™ is the only commercialized non-contact AFM mode worldwide; Bruker's flagship PeakForce Tapping™ is an advanced contact technique, but still contact-based.

Interpretation: Competition has shifted from 'which mode is best' to 'platform-wide accuracy, automation, and reproducibility,' creating a system moat. ~80% industrial share is the visible result.

3. Product Lineup & End Markets

3.1 Revenue Mix (2025 Q1, ₩50.9B total)

- Industrial ₩36.4B (72%) — higher ASP and margins, the core profit pool.

- Research ₩12.4B (24%); services ₩2.1B (4%).

- Geography — Greater China (CN+TW) ₩24.3B (48%). Park's flagship products are not on the US export-control list — net beneficiary so far.

- Backlog at Q1 end ₩89.3B (vs prior ₩85.3B) — 2–3 quarters of visibility.

3.2 Industrial Lineup & Applications

| Process | Core Problem | Park Solution | Customer Value |

|---|---|---|---|

| EUV Lithography | 13.5 nm light; photomask defect repair without damage | NX-Mask | Reuse multi-million-dollar EUV masks; direct yield uplift |

| Advanced packaging (HBM, hybrid bonding) | Post-CMP planarity and dishing at nm/Å scale | NX-Hybrid WLI + NX-Wafer | Bond yield and reliability |

| Front-end defect review | Wafer particle and defect analysis | NX-Wafer | Root-cause analysis, process improvement |

| Large-area display | Pixel uniformity for next-gen displays | NX-TSH | MicroLED/QD-OLED inspection |

Official fact: NX-Mask was developed and is being supplied at the request of the world's #1 foundry (commonly understood to be TSMC). Management told the Korea Economic Daily that hybrid-bonding-related revenue is expected to top 40% of sales within three years.

3.3 M&A — Becoming a Platform

- 2022 — acquired Accurion (Germany): imaging spectroscopic ellipsometry (ISE) for thin-film thickness and refractive index.

- Early 2025 — acquired Lyncée Tec (Switzerland): digital holographic microscopy (DHM) for high-speed 3D shape measurement.

- Goal: a hybrid metrology platform combining AFM accuracy and optical speed — Sang-il Park's stated 'Korea's KLA' vision.

4. Financials — A Virtuous-Cycle Growth Model

| (KRW B) | 2022 | 2023 | 2024 | 2024 Q1 | 2025 Q1 |

|---|---|---|---|---|---|

| Revenue | 124.5 | 144.8 | 175.1 | 25.7 | 50.9 |

| OP | 32.6 | 27.6 | 38.5 | 0.5 | 13.2 |

| OPM (%) | 26.2 | 19.1 | 22.0 | 1.9 | 25.9 |

| Net income | 28.0 | 24.6 | 42.8 | 2.7 | 15.0 |

| OCF | 31.3 | 34.7 | — | 11.6 | 9.7 |

| FCF | 17.0 | 17.1 | 26.8 | — | — |

Sources: company IR, FnGuide, KRX KIND disclosure, Q1 cash-flow statement PDF.

- Gross margin 65.2% (2024); OPM 22.0% (2024) → 25.9% (Q1 2025) — operating leverage steepens with scale.

- Debt-to-equity 46.0%, current ratio 304% at year-end 2024 — growth funded internally.

- 2020–2024 revenue CAGR 20–30%; 2024 FCF ₩26.8B — positive even after R&D, capex, and dividends.

Interpretation: Q1 OCF dipped modestly versus the prior year due to higher receivables and inventories — a working-capital effect, not a degradation of cash generation. The big picture is that moat → margin → OCF → R&D + capex → stronger dominance is cycling cleanly.

5. Competitor Comparison — Bruker, Oxford (WITec)

| Item | Park Systems | Bruker | Oxford (WITec) |

|---|---|---|---|

| Core AFM mode | True Non-Contact™ | PeakForce Tapping™ | Digital Pulsed Force Mode |

| Strength | Data accuracy; no tip/sample damage | Quantitative nano-mechanics (QNM) | Easy Raman integration |

| Strategy | Platformization (AFM + ISE + DHM) | Deepening AFM modes | Correlative (AFM + Raman) |

| Main market | Industrial (semi/display) + research | Research-centric (materials/biology) | Research (materials/chemistry/geology) |

| Share (overall) | #1 (20.3%) | #2 (18.8%) | ~9.1% |

| Share (industrial) | ~80% (de facto monopoly) | — | — |

Sources: QYResearch 2023; industrial share per TheElec, DigitalToday, YeleC.

Interpretation: Bruker drills deeper into AFM, Oxford specializes in optical-AFM correlation, while Park acquires complementary metrology and folds it into one workflow. As semiconductors move further into 3D structures and heterogeneous integration, single-method analysis loses, and Park's platform play strengthens.

6. The Uiwang Land Purchase — A Gwacheon–Yongin–Uiwang Triangle

Official fact: 2025-06-23 disclosure — Uiwang Cheonggye Public Housing District urban-support zone 2-2 block, 9,093.9 ㎡, ₩39.1B (14.26% of 2024 year-end assets), from LH (Korea Land & Housing Corp.). (Maeil Business, Seoul Finance)

- Gwacheon (R&D HQ): groundbreaking 2023-09, occupancy H1 2026, total ₩64.1B, 15F above / B5 — group's brain. (official news)

- Yongin (customer-adjacent production): a tenant inside SK hynix's 120T+ KRW Yongin semiconductor cluster — a forward base for the key customer.

- Uiwang (flexible production/R&D): urban-support zoning allows R&D centers and urban factories; adjacent to Gwacheon HQ for synergies; can host future battery/bio specialty R&D or extra production capacity.

7. Putting It Together & Risks

① Hard-to-copy moat (the trinity) → ② Beneficiary of the EUV / HBM / hybrid-bonding paradigm shift → ③ Platformization via M&A ('Korea's KLA') → ④ Self-funded preemptive capex (the triangle). All four firing at once.

Risks

- Semiconductor cycle — industrial sales track customer capex.

- US–China tech friction — 48% of Q1 sales were Greater China. Today's flagship products are not export-controlled, but rule expansion is a real swing.

- Short-term cost of simultaneous capex — depreciation/fixed-cost step-up post-occupancy could pressure near-term margins.

Sources

- Original Naver Blog post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=223924083247

- Author's prior post — Park Systems Primer #1: link

- Korea Economic Daily — Atomic microscopes in the chip nano-war: link

- Park Systems EN news: link

- FnGuide A140860 financials: link

- InfoStockDaily — record results & new HQ: link

- DigitalToday — interview on AFM in fine-process era: link

- Brunch — Park Systems global AFM #1: link

- TheElec — Why semi makers adopt Park AFM: link

- YeleC — Hybrid-bonding metrology beneficiary AFM Park: link

- Bruker — Industrial AFM / PeakForce Tapping: product · PeakForce

- Park Systems KR — Research AFM / how AFM works: link · link

- Park Systems webinar (YouTube): link

- True Non-Contact™: link · PDF

- Park NX-TSH brochure: PDF

- Park NX-Mask: PDF · EN · PR Newswire

- NX-Hybrid WLI: EN · mobile

- Park FX40/FX200: FX40 · AZoM FX200

- Park SmartScan™: link · PDF

- Wiley Analytical Science — Choosing an AFM / Automatic next-gen AFM: article1 · article2

- Sisajournal-e — Defending #1 with EUV mask tool: link

- SemiAnalysis — Hybrid Bonding Process Flow: link

- 3D InCites — Hybrid Bonding Challenges: link

- etnews — Park leaps to integrated metrology: link

- Maeil Business — ₩39.103B asset acquisition: link

- Seoul Finance — June 24 disclosures: link

- Newsis — Uiwang Wolam/Cheonggye corporate recruitment: link

- Kyeongin — Uiwang urban-support zone enterprises: link

- SK hynix newsroom — Yongin cluster Fab 1 groundbreaking: link

- DigitalDaily — Yongin cluster tenants confirmed: link

- BusinessPost — CEO Sang-il Park profile: link

- Korea JoongAng Daily — Washington tightens chip export rules: link

- KRX KIND disclosure (Park Systems annual report): link

- Park Systems Q1 cash-flow PDF: PDF