DEEP RESEARCH · S-OIL

S-Oil — The Five-Year Bottom Cycle and Conviction BUY Thesis

An energy research memo tying together an oil-price bottom, stronger refining margins, and historically low valuation

0. Bottom line first

This is a saved summary of a Hana Securities report. The core claim is that S-Oil shares have tended to form major bottoms roughly every five years, and the current setup combines an oil-price bottom, improving refining margins, and historically low valuation into a Conviction BUY thesis.

Official fact: The report maintains BUY and a target price of KRW 80,000, and presents S-Oil as a sector Top Pick. Current 12M forward PBR is cited at a historical low of 0.68x.

Interpretation: If 1.0x PBR held as a floor even during the 2014 and 2020 oil-price crashes, the current valuation can be read as already reflecting both structural concerns from EV penetration and concerns over the Shaheen project.

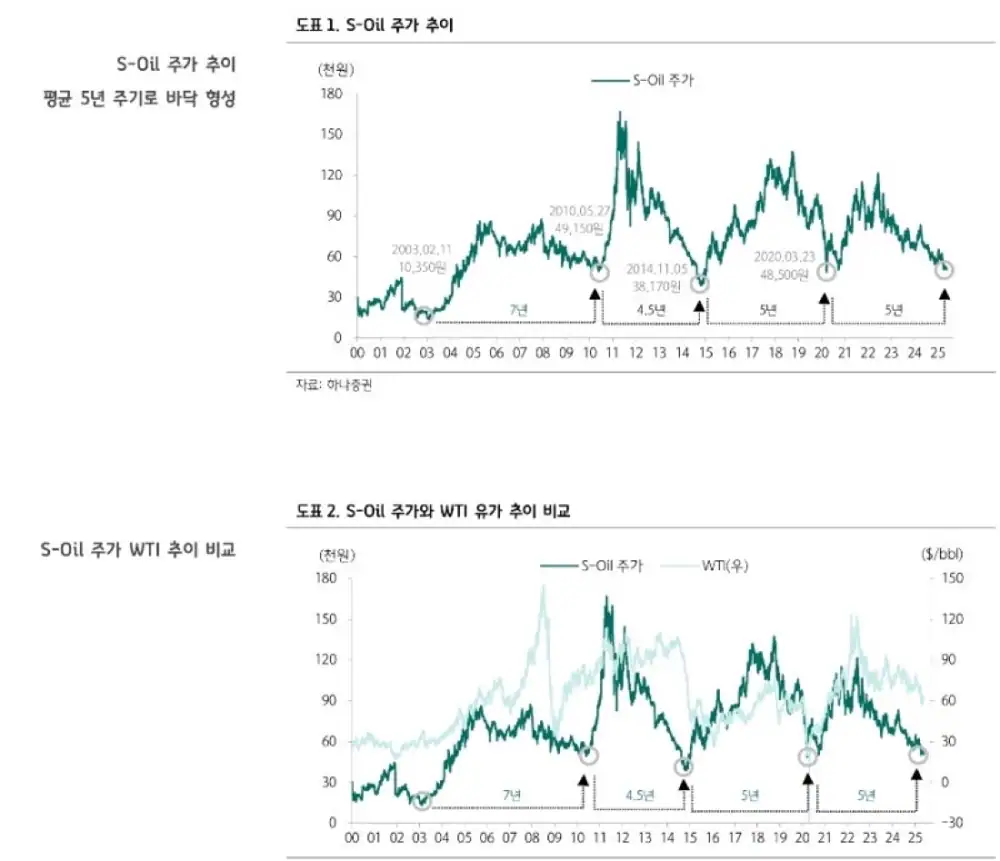

1. A major bottom about every five years

The report identifies S-Oil share-price bottoms in 2010, late 2014, early 2020, and the current period. It frames these as major bottoms roughly every five years, usually coinciding with oil-price or economic troughs.

The current level is viewed as an oil-price bottom. The report notes growing expectations that U.S. crude production will peak out in 2027, because more North American producers say they will cut CapEx and production when WTI is below $60.

2. Stronger refining margins and export expansion

Global net refining-capacity additions are said to have peaked in 2023-2024 and then decline sharply. The report cites YoY -64% in 2025 and none after 2027, which it expects to support stronger refining margins.

The U.S., the world’s No. 2 refining-capacity holder with 18% market share, is expected to close refining capacity. At the same time, the early repeal of EV tax credits under Trump could extend the life of internal-combustion vehicles to 2029, raising the possibility that petroleum-product inventories fall to a 25-year low. This would ultimately reduce U.S. petroleum-product exports.

The report argues that the benefit from reduced U.S. and Chinese exports should go to Korean refiners, because Korea is No. 5 globally in refining capacity and exports half of its capacity. Refining margins are already close to $10, the highest level this year, and further strength cannot be ruled out.

Slower net refinery additions

The cited YoY -64% in 2025 and no additions after 2027 drive the margin-upside thesis.

Potential U.S. export decline

The chain is U.S. 18% market share, closures, longer ICE life, and possible inventory decline.

Korean refiners’ export upside

Korea is cited as No. 5 in global refining capacity and exports half of its capacity.

3. Historically low valuation

The report maintains BUY and a KRW 80,000 target price for S-Oil. Valuation is cited at a historical low of 0.68x 12M forward PBR.

Given that 1.0x PBR acted as a floor even during the 2014 and 2020 oil-price crashes, the current valuation is framed as a de-rating that reflects both 1) structural industry concerns from rising EV penetration and 2) concerns over the large Shaheen project, including higher debt and lower dividends.

The report argues that Trump’s policies are becoming favorable to traditional energy companies: early EV tax-credit repeal, preservation of IRA tax credits 45Q/45Z, and efforts to remove EPA greenhouse-gas emission limits on thermal power plants. It also argues that Shaheen can generate meaningful earnings even in the current petrochemical environment, so the valuation discount of the past five years may soon narrow.

| Item | Report figure/view | Meaning |

|---|---|---|

| Rating | BUY maintained | Positive stance retained |

| Target price | KRW 80,000 | First target framed around 1.0x PBR |

| 12M forward PBR | 0.68x | Cited as a historical low |

| Refining margin | Near $10 | Highest level of the year |

4. Checkpoints

- Whether North American producers actually cut CapEx and production when WTI stays below $60

- Whether weaker net global refining-capacity additions translate into stronger refining margins after 2025

- Whether reduced U.S. and Chinese petroleum-product exports create export opportunities for Korean refiners

- Whether Shaheen project concerns ease through reported earnings

- Whether the valuation discount can narrow toward 1.0x PBR, around KRW 80,000

Sources

- Original Naver blog post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=223878550318

- Hana Securities report: https://bit.ly/43N4ukE

- Hana Securities energy/chemicals Jaesung Yoon Telegram: https://t.me/energy_youn