DEEP RESEARCH · INBODY

InBody: Do Not Forget This Is a Medical-Device Company

A memo on Q1 2025 results and the valuation-frame shift from PER to EV/EBITDA

0. Bottom line first

The biggest change I noticed in this InBody Q1 2025 report is the shift in valuation metric from PER to EV/EBITDA. As the report title says, I read this as treating InBody as a medical-device company and valuing it against future cash-generating ability.

The source material is a Mirae Asset Securities InBody report written by Kim Choong-hyun, CFA, and one co-author. I keep the link here as the Mirae Asset corporate research report.

1. Q1 2025 results: sales were strong, operating profit was pressured

Official fact: Based on the link preview, Q1 2025 revenue rose 15% YoY to KRW 55.6 billion, beating market expectations and setting a fifth consecutive record-high result.

Official fact: The same preview says operating profit fell 30% YoY to KRW 7.0 billion, missing market expectations. Operating margin was 12.6%, down 8.0 percentage points YoY.

KRW 55.6bn

Q1 2025 revenue rose 15% YoY and beat market expectations.

5th straight high

The link preview describes this as the fifth consecutive record-high result.

KRW 7.0bn

Operating profit fell 30% YoY and missed market expectations.

12.6%

Operating margin declined by 8.0 percentage points YoY.

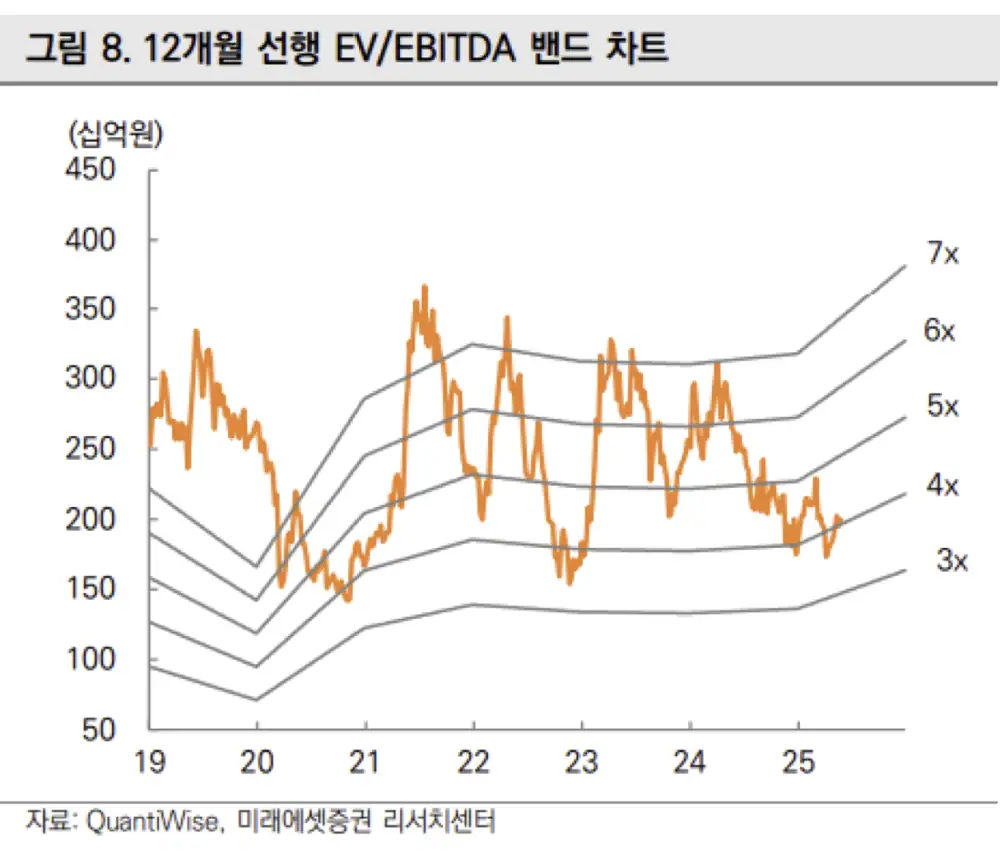

2. Key change: from PER to EV/EBITDA

Usually, this kind of report comes out the day after earnings are announced, but this one came a little late. For a moment I wondered whether coverage was being dropped. The main feature of this report, however, was the valuation metric changing from PER to EV/EBITDA.

Interpretation: I understand this as an attempt to look at cash-generating ability, similar to how other medical-device companies are valued. If depreciation, taxes, and interest expenses are added back to operating profit, labor costs are probably the major cost item. The point seems to be comparing how much cash the company can generate after labor costs have increased.

3. Why EBITDA matters

Official fact: The source defines EBITDA as Earnings Before Interest, Taxes, Depreciation, and Amortization. It is calculated by adding interest expense, taxes, and depreciation/amortization to pre-tax operating profit, or more commonly by adding depreciation/amortization back to operating profit.

Interpretation: Because depreciation and amortization are non-cash expenses, adding them back gives a more direct view of cash generated through operations. That is why the valuation change connects with the report title: “InBody is a medical-device company.”

| Frame | Meaning I read from the source |

|---|---|

| PER | Centered on accounting profit or earnings multiples |

| EV/EBITDA | Comparison closer to operating cash-generating ability |

| Investment check | Whether cash generation holds up after labor costs have risen |

4. My checklist

- Q1 2025 revenue growth and the fifth consecutive record-high result are positive.

- The decline in operating profit and operating margin requires a closer look at the cost structure.

- I understand the use of EV/EBITDA as a way to compare cash generation as a medical-device company.

- This memo is an interpretation of the report, not a buy or sell recommendation.

Sources

- Original Naver Blog post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=223874683710

- Mirae Asset Securities corporate research report: https://securities.miraeasset.com/bbs/board/message/view.do?messageId=2332353&messageNumber=1294&messageCategoryId=0&startId=zzzzz%7E&startPage=1&curPage=1&searchType=2&searchText=&searchStartYear=2024&searchStartMonth=05&searchStartDay=22&searchEndYear=2025&searchEndMonth=05&searchEndDay=22&lastPageFlag=&vf_headerTitle=&categoryId=1800