DEEP RESEARCH · INBODY

InBody Q1 2025 Results Review

A results note focused on SG&A, labor-cost growth, and cash generation that still appears intact

0. Bottom line first

Overall SG&A continues to rise, and I think the increase may continue through Q2 this year. The company hired a lot of people from the second half of last year and is still adding staff, so I am not expecting much from this year's earnings. Still, despite the higher payroll, the actual cash the business generates does not look very different from usual, so I think these results are fairly impressive.

1. The Core Cost Increase Is Headcount

The number of people hired since the second half of last year is very large, and the company is still hiring this year. Taking that into account, I am not expecting much from this year's earnings.

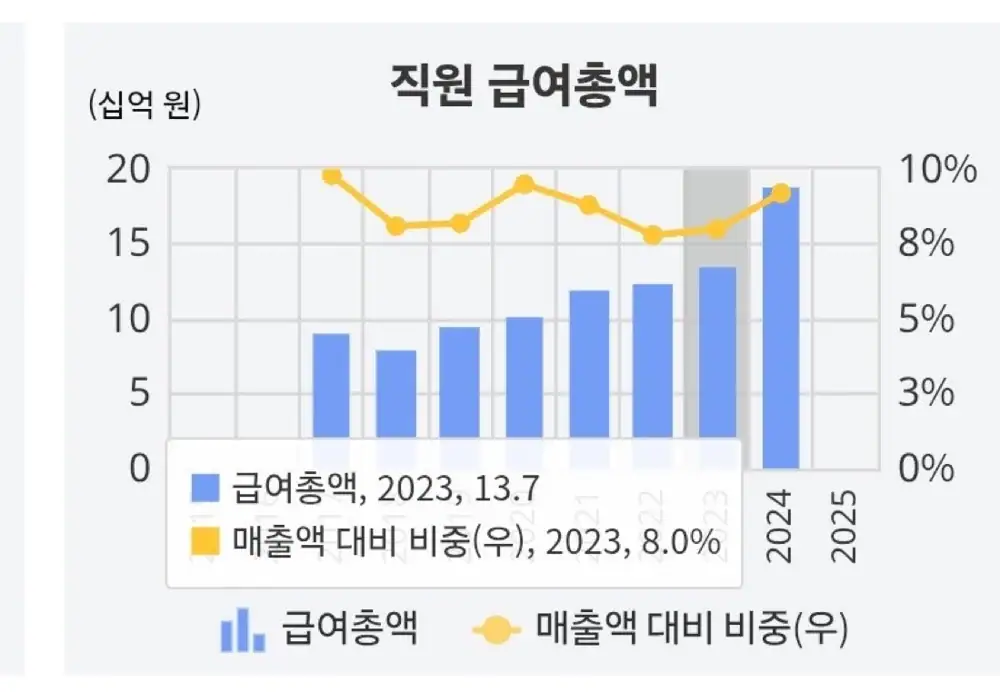

Official fact: In the source, labor costs are summarized as increasing by KRW 5 billion, from KRW 13.9 billion in 2023 to KRW 18.9 billion in 2024.

| Item | 2023 | 2024 | Change |

|---|---|---|---|

| Labor cost | KRW 13.9 billion | KRW 18.9 billion | Increase of KRW 5.0 billion |

SG&A increase

With continued hiring, the SG&A burden may persist for a while.

Salesforce expansion

This is a period of waiting for the people hired since last year's second half to enter actual sales activity.

Step-up timing

I am waiting for the point when the added staff begin producing results and lift earnings to another level.

2. Related Memo and Source Link

The earlier memo on additional hiring can be found at [InBody] InBody continues additional hiring.

3. What Still Looks Positive

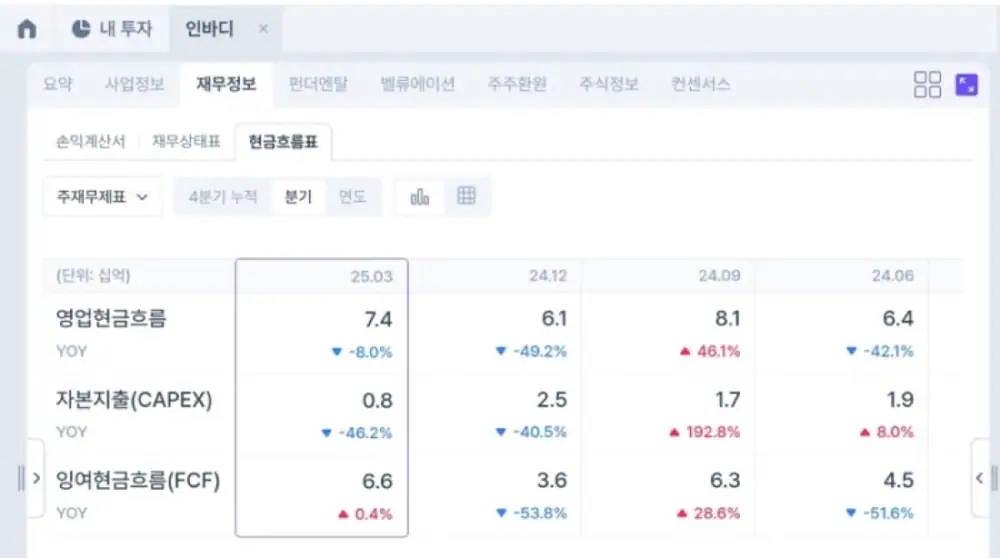

Interpretation: In addition, cash flow is not bad. Despite the salaries for the larger workforce, the actual cash the company earns does not look different from usual. From that perspective, I think these results are fairly impressive.

For now, I am waiting for the people hired last year to begin sales activity in earnest in the second half and produce results.

Sources

- Original Naver Blog post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=223867774512

- Related post: https://m.blog.naver.com/star_of_self/223816405628