DEEP RESEARCH · INCAR FINANCIAL SERVICE/GA GROWTH STOCK

[Incar Financial Service] Why Incar Financial Service?

An investment-idea memo connecting rapid earnings growth, planner-network expansion, structural advantages of independent GAs, and post-IFRS17 insurer sales incentives

0. Bottom line first

This is not a buy or sell recommendation; I am writing it down for myself. With the market cap in the mid-KRW 300 billion range in the source note, I view Incar Financial Service as a real growth stock whose revenue and earnings grew rapidly from 2021 to 2024. The key drivers are planner-network expansion, the product and commission flexibility of independent GAs, and insurers’ stronger incentive to win new contracts after IFRS17.

1. Recent four-year consolidated results

Official fact: The source mentions Incar Financial Service’s market capitalization as in the mid-KRW 300 billion range and summarizes consolidated revenue, operating profit, and net income from 2021 to 2024.

| Year | Revenue | Operating profit | Net income | Memo |

|---|---|---|---|---|

| 2021 | About KRW 268.5bn | About KRW 21.1bn | About KRW 16.4bn | Estimate |

| 2022 | About KRW 401.5bn, +49% YoY | About KRW 27.4bn, about +30% YoY | About KRW 20.8bn | Continued growth |

| 2023 | KRW 556.8bn, +38.7% YoY | KRW 46.6bn, +70.1% YoY | KRW 29.87bn | Record-high results |

| 2024 | KRW 832.2bn, +49.4% YoY | KRW 86.3bn, +85.2% YoY | About KRW 62.0bn, about +110% YoY | Revenue in the KRW 800bn range, operating profit in the KRW 80bn range |

Interpretation: Results jumped especially in 2023 and 2024. Net income is estimated to have roughly doubled from KRW 29.8bn in 2023 to the KRW 60bn range in 2024. Revenue and profitability improved together over four years, with high growth continuing after the 2022 KOSDAQ transfer and the 2023 adoption of IFRS17.

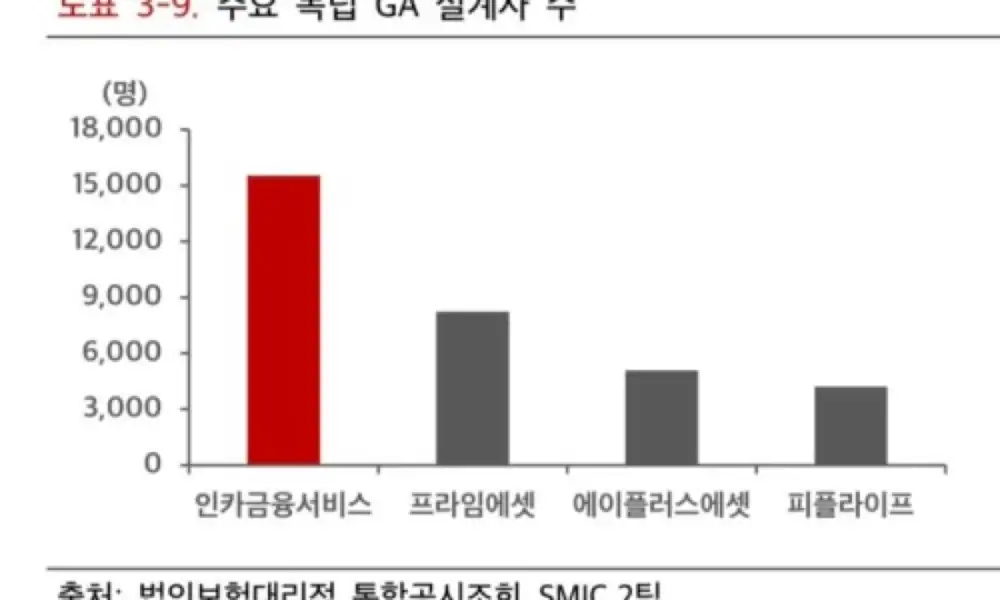

2. Incar Financial Service vs. Aplus Asset

Incar Financial Service and Aplus Asset are both listed independent GA companies in Korea, and their business structures are similar, but their recent growth speeds differed sharply.

| Item | Incar Financial Service | Aplus Asset |

|---|---|---|

| Exclusive planners | About 18,000 at end-2024 | About 6,000 |

| 2023 revenue | KRW 556.8bn | About KRW 400bn, roughly 70% of Incar |

| 2024 revenue | KRW 832.2bn, +49.4% YoY | Expected about KRW 446.1bn |

| 2024 operating profit | KRW 86.3bn, +85.2% YoY | Expected KRW 29.3bn |

| Strategy | Aggressive planner recruitment, entrepreneur-type branch strategy, IT-based sales support | Stable operation based on capital strength, with M&A in parallel |

Planner recruitment and organization expansion

Incar rapidly expanded its planner organization, driving fast growth in new-contract revenue.

IT support after IPO

Productivity improvement through IT-based sales support after securing IPO proceeds is cited as a growth factor.

External-growth sensitivity

Incar’s high sensitivity to new-contract revenue made its top-line growth stand out, while Aplus Asset appears to follow a more profitability-centered, stable growth curve.

Official fact: The source notes that Shinhan Securities had highlighted both “Incar, which rapidly expands its planner organization,” and “Aplus Asset, which has comparatively stronger capital.”

3. Structural strengths of independent GAs

At the current point, the structural advantages of independent general agencies over insurer-owned GA subsidiaries come from product supply, commission and compensation systems, and scale and expertise.

Comparison across insurers

Independent GAs can compare and sell products from multiple life and non-life insurers in one place, increasing consumer choice and planner sales efficiency. The source says planners can propose portfolios from about 30 insurers.

Flexible commission allocation

They can negotiate higher acquisition commissions with insurers and distribute them competitively to planners.

Large scale and internal control

Listed large independent GAs can use capital to invest in IT systems, customer management, compliance, education, and acquisitions of smaller GAs.

Interpretation: Insurer-owned GAs may have commission rates controlled by the parent company and restrictions on selling external products, leaving planners with fewer income opportunities. Independent GAs can benefit from a virtuous cycle of attracting strong planners and improving sales power.

In short, independent GAs have competitive advantages from broad product handling, flexible commission policies, and active talent acquisition. The fact that insurers have become more dependent on external GA channels after IFRS17 also supports the structural advantage of independent GAs.

4. How IFRS17 changed insurer sales strategies

Official fact: IFRS17 changed insurers’ management indicators and strategies. Under IFRS4, writing more new contracts increased first-year acquisition costs such as commissions and could damage short-term earnings.

Official fact: Under IFRS17, applied from 2023, revenue and costs are recognized over the period in which insurance service is provided. Profit generated from new contracts is calculated as contractual service margin, or CSM, and recognized gradually over the coverage period; first-year acquisition costs are also capitalized and amortized over time.

Interpretation: As CSM became a core measure of insurers’ long-term profit-generation capacity, insurers focused on increasing CSM. Since new contracts are the only way to increase CSM, the logic is that insurers have to pursue much more aggressive new-contract sales strategies than before.

This change also affected product and sales strategies. In 2023, multiple products such as short-pay whole-life insurance, children’s insurance, and nursing-care insurance were launched at the same time, and insurers tried to create demand by lowering premiums or expanding coverage. In short, IFRS17 reorganized insurance accounting around accrual recognition and CSM, making new contracts a store of future profit, or profit backlog.

5. Late-2024 GA insurance-distribution regulation

I do not know whether it was because of overheating, but in December 2024 financial authorities pursued new legal and institutional changes to reform insurance distribution. At the 5th Insurance Industry Innovation Council on December 16, 2024, the direction for reforming sales-commission systems to improve GA sales practices was discussed, and related legal amendments were later announced.

| Reform | Core point | Expected effect/risk |

|---|---|---|

| Advance disclosure of sales commissions | Consumers would be shown planner commission information when buying insurance | Reduce bias toward high-commission products and improve consumer choice |

| Installment payment of acquisition commissions | Commissions concentrated in year one would be gradually restructured to be paid over up to seven years | Better post-sale management, but lower first-year planner income in the short term |

| Maintenance/service commissions | Maintenance and management commissions after year two would be newly added or expanded | Stronger incentive for customer retention |

Official fact: The source explains that under the existing system, up to 1200% of annualized premium could be prepaid in year one, while the reform proposal would divide payments over multiple years and add or expand maintenance/management commissions after year two. According to a Financial Services Commission simulation cited in the source, if about 1.0% of monthly premium is paid each month as a maintenance commission, planner income becomes equal to the current system from year five; at 1.5%, it can normalize from year four.

Interpretation: In the short term, installment commissions will likely reduce first-year planner income and may slow the inflow of strong new planners. There is also concern that consumers may judge products only by commission information and simply choose lower-commission products.

6. Possible GA industry restructuring after regulation

The likely impact on the GA industry is faster restructuring and consolidation. If installment commission payments weaken GA short-term cash flow, smaller GAs with weaker capital may struggle to operate.

Interpretation: Large GAs with capital capacity, such as Incar Financial Service and Aplus Asset, may use this as an opportunity to acquire smaller GAs and increase market power. This could accelerate concentration among top-tier GAs, while consumers may benefit from stronger brand trust and more standardized internal controls at larger GAs.

The late-2024 proposed insurance-distribution amendments center on improving GA commission transparency and payment structure. They may create significant short-term growing pains, but the medium- to long-term view is that they could improve the industry’s fundamentals and trust.

7. Reference reports and linked materials

The source cites Shinhan Securities reports, “Insurance Basics (Part 1),” and a neighboring blogger’s post as reference materials. It also includes the Shinhan insurance/securities Telegram link by Hee-yeon Lim: https://t.me/heeyeonlim

Neighboring blogger’s Incar Financial Service investment-idea post: https://m.blog.naver.com/hamboogii/223821293927

Sources

- Original post: Naver Blog original

- Shinhan insurance/securities Telegram by Hee-yeon Lim: https://t.me/heeyeonlim

- Neighboring blogger reference: Incar Financial Service investment idea