DEEP RESEARCH · INBODY

[InBody] 4Q24 Earnings Review Since 2020

Reviewing revenue, overseas growth, home devices, staffing investment, and shareholder returns since 2020

0. Bottom line first

InBody has grown both revenue and shareholder returns since 2020. I want to focus on two points: rapid growth in emerging Asia, including Southeast Asia, and fast growth in home body-composition analyzers.

Interpretation: 2024 looks like a year of higher cost burden from overseas direct-sales networks and headcount expansion, but the revenue base became more global and home-device contribution grew meaningfully. The key is whether this investment translates into revenue growth and larger shareholder returns.

1. Revenue trend by device

Official fact: The original post says professional body-composition analyzer revenue was about KRW 143.8bn in 2024, accounting for 70% of total revenue. Compared with around 70% of total 2020 revenue of about KRW 107bn, the category nearly doubled.

| Product group | 2024 figure | Change |

|---|---|---|

| Professional body-composition analyzers | About KRW 143.8bn, 70% of total | Nearly doubled versus 2020. The 2024 InBody 380/580 launches contributed to growth. |

| Home/consumer analyzers | About KRW 24.5bn, 12% of total | Grew more than 4x from the KRW 6bn range and 6% revenue share in 2020. |

| Automatic blood-pressure monitors | About KRW 9.6bn, 5% of total | Showed moderate growth. |

| Stadiometers, software, others | Remaining 10%-plus | Revenue increased broadly across product groups. |

Professional remains central

Professional devices, at 70% of revenue, remain InBody’s base business.

Home share expands

Home-device share rose from 6% to 12%, and revenue grew from the KRW 6bn range to KRW 24.5bn.

BIA-adjacent products

Blood-pressure monitors, stadiometers, software, and services can attach around the core technology.

2. Regional revenue shift

Official fact: Overseas revenue share rose from about 75-80% in the early 2020s to 81% in 2024, while Korea declined to 19%. 2024 domestic revenue was KRW 39.1bn, up 5% YoY, while overseas revenue was KRW 165.3bn, up 24% YoY.

| Region | 2024 revenue/share | Growth |

|---|---|---|

| U.S. | KRW 64.4bn, 32% of total | +23% |

| Europe | 13% of total | +21% |

| China | 8% of total | +26% |

| Other emerging Asia | Share rose from 6% to 8% | +46% |

| Japan | KRW 19.5bn, 10% of total | +7% |

| Korea | KRW 39.1bn, 19% of total | +5% |

Interpretation: The U.S. remains the largest market, but 46% growth in emerging Asia is a meaningful new growth driver. Double-digit growth across most overseas regions also reinforces the shift toward a more overseas-dependent revenue structure.

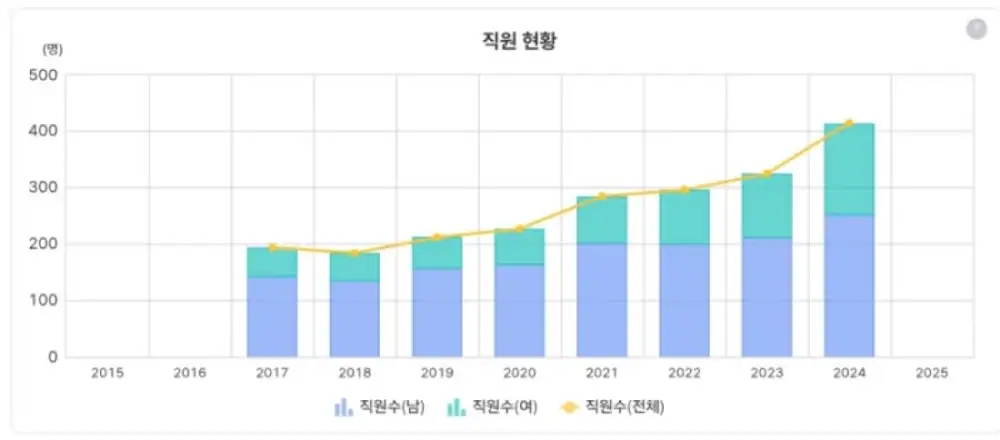

3. Hiring and cost structure

Headcount expanded from about 800 globally around 2020 to about 1,100 in 2024. At headquarters, the year-end 2024 employee count was 415, with 254 men and 161 women.

Official fact: The original post says InBody expanded sales staff significantly to strengthen overseas direct-sales capability, and SG&A increased 29% YoY as a result. It also says roughly 20-30% of total employees are maintained as R&D staff.

Interpretation: 2024 cost growth can be read less as a simple negative and more as upfront investment in overseas subsidiaries, direct sales, and new product development. Still, the added hiring must translate into revenue growth; otherwise margin pressure can intensify.

4. Treasury shares and dividends

Official fact: As of end-2024, InBody held 970,775 treasury shares, equal to about 7.1% of total shares outstanding. The treasury-share ratio rose from around 5% a few years earlier to more than 7%, and the large buyback/cancellation action announced at end-2024 showed a more active shareholder-return stance.

| Item | Figure | Meaning |

|---|---|---|

| DPS | KRW 140 in 2020, KRW 200 in 2021, KRW 300 in 2022, KRW 350 for 2023, KRW 400 for 2024 | Dividend per share increased nearly threefold over the recent four-year period. |

| Total dividends | About KRW 1.8bn in 2020 to about KRW 5.07bn in 2024 | Total dividend amount expanded with earnings growth. |

| Payout ratio | Generally low-teens, about 14% for 2023 | There may still be room for higher dividends. |

| Dividend yield | About 1.5% in 2022 | Not high versus the market, but attractiveness has improved with dividend increases. |

| 2025 | Possible quarterly dividend | The original post says quarterly dividends look likely in 2025 based on the AGM agenda. |

2024 consolidated net income is estimated at about KRW 32.7bn, up around 20% YoY. Adding about KRW 5.07bn of dividends and KRW 5bn used for buybacks gives roughly KRW 10bn of direct shareholder return, or around 25% of net income.

Interpretation: Through 2022, shareholder return was only in the high-single-digit to low-teens range, but dividend increases and share cancellation lifted 2024 shareholder return into the 20% range. From an investor perspective, I still wish it were higher.

5. Upside factors and risks

Global healthcare

Aging, obesity, and the shift toward treating and preventing obesity as a disease are favorable for body-composition analysis demand.

Portfolio expansion

The 2024 InBody 380/580 models received good responses, and development of BIA-based medical and healthcare devices continues.

A larger market

The home healthcare-device market is estimated at about KRW 1.5tn, roughly seven times the professional market, and CEO Cha Ki-chul has targeted more than 50% annual growth in home-product sales.

Asia, India, Middle East

As shown by 46% growth in emerging Asia, low-penetration markets still offer growth potential.

| Risk | Detail |

|---|---|

| Market-development cost | In some overseas regions, body-composition analysis is still unfamiliar, so education and direct-sales costs are required. Building an owned sales network rather than relying on dealers can hurt near-term profitability. |

| New-business execution | Blood-pressure spin-off plans, startup investments, and adjacent businesses may dilute resources if they fail to create synergy with the core business. |

| Competing technology | InBody leads in medical BIA, but AI healthcare devices or alternative technologies could change the market structure. |

6. Management direction and expansion risk

CEO Cha Ki-chul’s interviews and external activity suggest an expansion of the existing philosophy rather than an abandonment of it. InBody historically built a niche around accurate body-composition measurement, and it is now widening that strategy into larger markets such as home devices.

Official fact: The original post notes that InBody data has been used in more than 5,000 papers and that InBody was selected for Forbes Asia’s 200 Best Under a Billion in 2024.

Interpretation: The underlying management philosophy still appears to emphasize technology and measurement accuracy. The change is a strategic widening of the market scope. Although 2024 operating profit declined slightly due to overseas direct-sales buildout and large-scale hiring, the original post says the company described this as expected upfront investment for long-term growth.

The key message from Cha’s interview is that managers deal with unknown problems. I read this as saying management is about responding to hard-to-predict changes in competition, technology, and markets, rather than only handling obvious issues.

The linked Forbes Korea interview post is below.

[InBody] Forbes Korea interview - The road no one has taken

7. Overall view

Over the last four to five years, InBody has achieved both steady growth and business expansion. Revenue grew from KRW 107.1bn in 2020 to KRW 204.5bn in 2024, alongside product diversification and global expansion.

Interpretation: Profitability weakened temporarily in 2023 and 2024, but the original post views that as the effect of investment for future growth. A debt ratio around 20%, healthy cash flow, dividend increases, and share cancellation support the expansion strategy.

Near term, the main risks are lower margins from higher costs and uncertainty over whether rapid headcount growth will produce revenue growth. For now, I would focus less on short-term earnings and more on the long-term growth story, management execution, and whether shareholder returns keep rising alongside growth.

Sources

- Original post: Naver Blog original

- Related Forbes Korea interview post: https://m.blog.naver.com/star_of_self/223797485194

- Original note: the main analysis says it is based on the 4Q24 business report, disclosures, extracted data from those documents, and foreign media reports.