DEEP RESEARCH · EASY BIO/FEED ADDITIVES

[Easy Bio] Will U.S. Pork Supply Increase in 2025?

A combined review of 4Q24 results, shareholder returns, U.S. M&A, and the feed-industry logic from Trump’s first term

0. Bottom line first

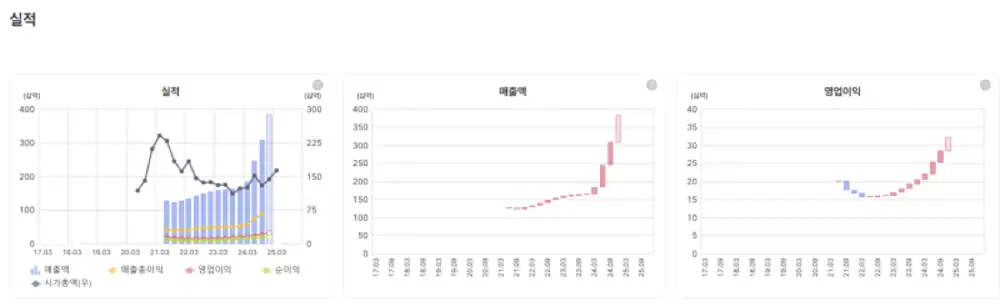

Easy Bio’s 4Q24 results were quite strong, and shareholder returns appear to have changed materially. The core issues are the U.S. feed and hog environment, the Devenish Nutrition acquisition, dividends and share cancellation, and the direction of the professional management structure.

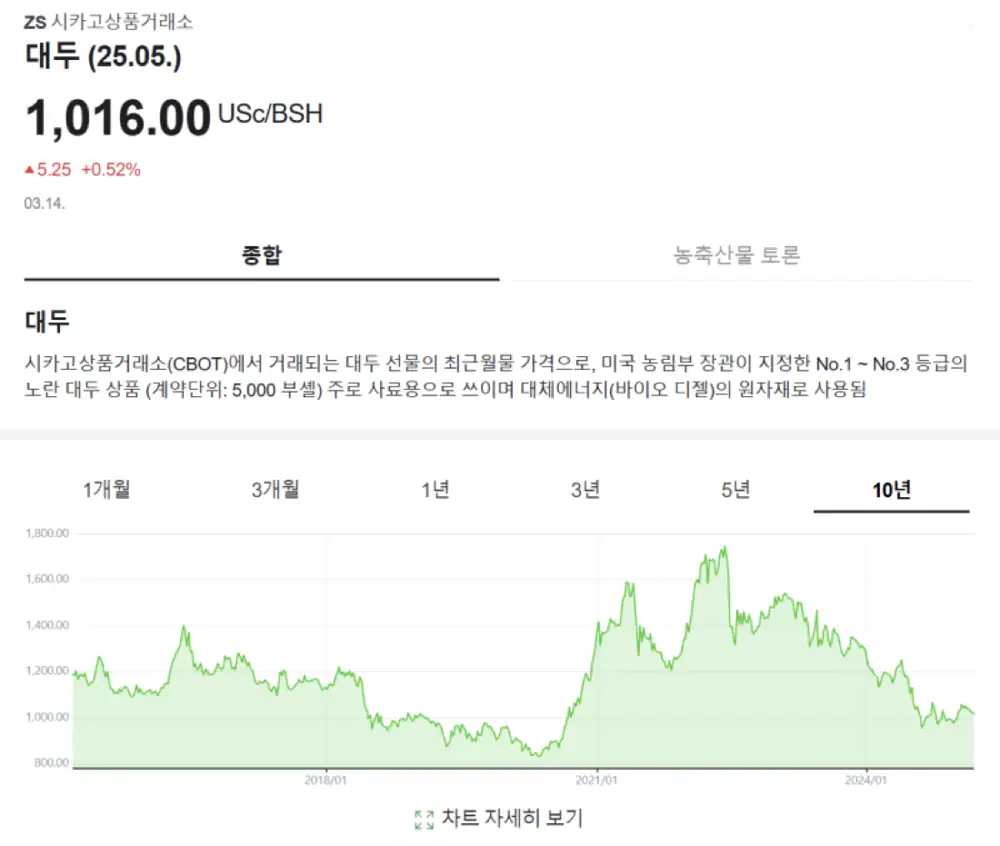

I am looking at Easy Bio, a subsidiary of Easy Holdings Group, because it belongs to the feed business. Feed should be affected mainly by grain prices, and soybean prices appear to be stabilizing from the wartime spike, even if part of that may already be priced in.

1. Trump’s first term and the hog-feed logic

Official fact: The Eugene Investment & Securities report referenced is Easy Bio company analysis - record earnings expected in a favorable environment.

The claim that hog-feed companies benefited from the U.S.-China trade dispute during Trump’s first term (2017-2020) is somewhat simple, but from a feed-company perspective it has some logic. In the tariff war that began in 2018, China imposed a 25% tariff on U.S. soybeans, raising feed costs in China, especially soybean meal as a protein source for hog feed, and hurting hog farms.

Official fact: In the U.S., reduced Chinese soybean imports left more domestic soybean supply and partly lowered soybean-meal prices for feed. The original post notes that USDA analyzed that the soybeans not imported by China actually reduced feed costs for U.S. hog farmers.

Interpretation: It is hard to say the hog-feed industry enjoyed one-way prosperity during the trade dispute. Conditions differed by region. Still, I think U.S. hog inventory could increase. The U.S. may ask others to buy pork as well as LNG.

2. Devenish Nutrition acquisition and the U.S. market

Official fact: Easy Bio entered the U.S. market in March 2024 by acquiring U.S. feed-additive manufacturer Devenish Nutrition for about KRW 88.3 billion.

The U.S. is the world’s largest hog and feed market. It is also a market where trade-dispute effects highlighted feed-formulation changes and demand for alternative additives. A company with advanced feed-additive technology, like Easy Bio, can address weaknesses in conventional feed or supply alternatives.

Interpretation: When feed supply chains are disrupted by policy shifts such as those under the Trump administration, China and others tried to fill gaps with additives and alternatives. Easy Bio’s technology and global network could stand out in a similar environment. If future policy turns favorable for U.S. agricultural and livestock products, Easy Bio’s local U.S. base could benefit from higher production and exports.

3. Changes in shareholder returns over four years

| Item | Change noted in the original post | Meaning |

|---|---|---|

| Dividend yield | From low 1-2% range around 2019 to about 2.8% in 2022; recent year also around 2.8% | Nearly doubled versus the past |

| Payout ratio | About 20% as of 2023 | About one-fifth of net income returned |

| Treasury shares | About KRW 4 billion bought back and cancelled in 2024 | Additional capital return beyond dividends |

| Total return ratio | Estimated mid-30% range of 2024 net income | Well above the prior year’s 20% dividend-return level |

At the end of 2024, Easy Bio approved transferring capital reserves into retained earnings through an extraordinary shareholder meeting. This was to expand dividend capacity. The original post notes that a capital-reserve reduction dividend is a special dividend not taxed to shareholders under Korean tax rules, implying an effective tax-free yield of about 3.05%.

Interpretation: The higher shareholder-return ratio seems linked to governance changes and management turnover. After the 2020 holding-company transition, Easy Holdings came to own about 50% of Easy Bio, giving the parent an incentive to receive stable dividends from the subsidiary.

4. Management philosophy and leadership changes

A top-tier bio-resource company

Since the 1999 KOSDAQ listing, the company emphasized high-value products using biotechnology, future-oriented value creation, principled management, and global expansion.

Aggressive growth through M&A

Chairman Ji Won-cheol pursued vertical integration across feed, hogs, poultry, and food, including the 2011 acquisition of Maniker.

Selection & Focus

The current team combines core-capability strengthening with selective M&A. The original post notes that the 2024 Devenish acquisition more than doubled sales and raised overseas-sales exposure from 10% to 60%.

Since the 2020 holding-company split, Easy Bio has maintained a co-CEO structure centered on professional managers. The company moved to three co-CEOs after appointing Hwang Il-hwan in late 2021, and in 2024 Kim Choong-seok reportedly joined, leaving the current structure as Ji Hyun-wook and Kim Choong-seok as co-CEOs.

Future plans include strengthening North America, expanding sales networks into Europe and South America, using Devenish’s network, aiming to become a global top-20 feed company, building synergies with life-science affiliates such as Optipharm, and investing in cultured meat, animal pharmaceuticals, and bacteriophage-based feed additives.

Sources

- Original post: Naver Blog original

- Eugene Investment & Securities/Naver Pay Securities report: Easy Bio company analysis

- Sources as listed in the original post: U.S. Reuters and Economist reports; brokerage analyst reports; company filings/news; 1999 agriculture/livestock interview; Business Post and other press interviews/analysis.

- Original data-link URL: https://finance.naver.com/research/company_read.naver?nid=79988&page=1&searchType=keyword&keyword=%C0%CC%C1%F6%B9%D9%C0%CC%BF%C0