DEEP RESEARCH · CHINA BATTERY

[Battery] China Battery Industry Visit Notes - Mirae Asset Report

A memo summarizing leading-company opportunities and restructuring in China's battery industry based on a Mirae Asset field-visit report

0. Bottom line first

China's battery industry appears to be entering a restructuring phase after excessive fragmentation. I think it is better to focus on No. 1 and leading players. Chinese battery stocks have also moved differently from Korean peers since around September 2024, breaking above a prior box range, so they are worth watching.

Official fact: The original post linked the Mirae Asset report here: Microsoft PowerPoint - 250306_2차전지 중국 탐방기_F.pptx

Interpretation: If oversupply eases and restructuring proceeds, I see more upside in leading companies such as CATL, EVE Energy, and Yunnan Energy New Material than in weaker followers.

1. Investment points

China EV demand upgrade

The 2025 China EV sales forecast was raised 11%, from 12.05 million units to 13.49 million units, implying YoY growth of 17%.

ESS acceleration

China ESS battery shipments were described as growing 70%, above the EV battery growth rate of 20%, helped by Tesla Megapack operations.

Oversupply easing

The thesis is that oversupply eases around leading companies and weaker players are cleaned up from the second half.

Robot and drone batteries

Battery adoption is expected to expand in humanoid robots, eVTOL, and other robot and drone applications.

Battery metal prices also need to be watched for bottoming, because lithium and nickel downside is described as limited with some recovery potential.

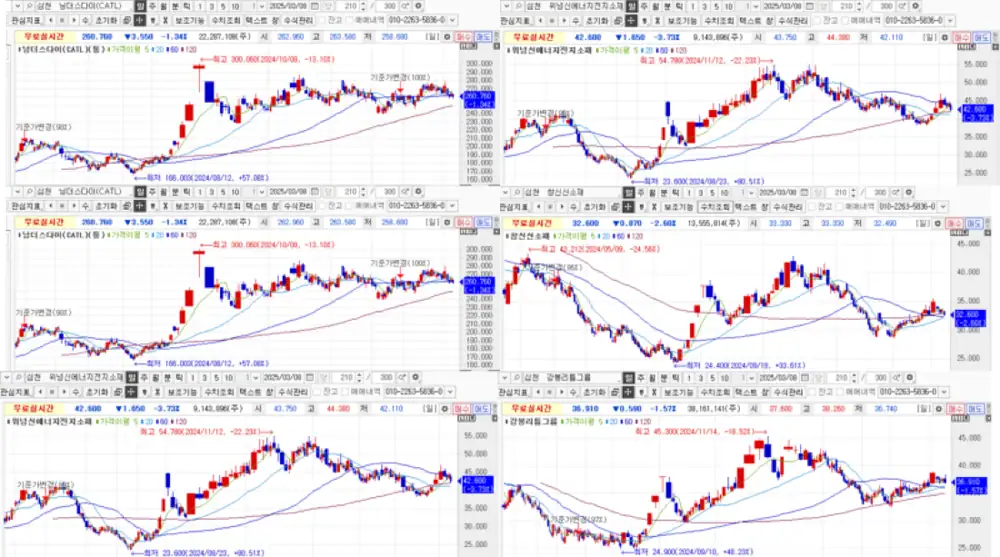

2. Top-pick companies and ideas

| Company | Main business | Investment point | Risk |

|---|---|---|---|

| CATL (300750) | Battery cells | Global No. 1 battery maker, new Tesla ESS and Model Y supply expansion, faster Europe/North America expansion | Protectionism risk |

| EVE Energy (300014) | Battery cells, cylindrical and ESS | Tesla Megapack orders, No. 2 ESS player, aggressive pricing | Protectionism and weak profitability from low-price orders |

| Yunnan Energy New Material (301358) | LFP cathode materials | Major CATL and BYD supplier, global No. 1 share of 27% | Protectionism |

| Shenzhen Senior Technology Material (002812) | Separator | Global No. 1, expected M&A and restructuring among followers | High near-term inventory |

| Huayou Cobalt (603799) | Precursors/battery metals | Nickel and cobalt price stabilization, impact from Congo cobalt export limits | Weak ternary battery demand |

| Ganfeng Lithium Group (002460) | Lithium concentrate and processing | Cost advantage, vertical integration, lower capex | Protectionism |

| Tianqi Lithium (002466) | Lithium compounds | Greenbushes mine production growth of +32% YoY and increasing lithium-compound output | Protectionism |

Interpretation: Chinese battery stocks have moved differently from Korean names since September 2024. If restructuring among Chinese makers continues, the stock performance of No. 1 players could improve, so I want to keep watching them.

3. Comparison with Korean peers

| Chinese company | Korean competitors | Strengths | Weaknesses |

|---|---|---|---|

| CATL | LG Energy Solution, SK On, Samsung SDI | Upstream/downstream bargaining power and full-scale overseas expansion | Stronger protectionism in the U.S., Europe, and other major markets |

| EVE Energy | LG Energy Solution, SK On, Samsung SDI | Expansion centered on cylindrical batteries and ESS | Protectionism and weak profitability from low-price orders |

| Yunnan Energy New Material | EcoPro BM, POSCO Future M | Stable utilization from strong downstream customers and overseas business ramp-up | Protectionism in major markets |

| Shenzhen Senior Technology Material | SK IE Technology, WCP | Wider utilization gap versus followers and overseas expansion in wet separators | Weak results expected through the first half due to high inventory and protectionism |

| Huayou Cobalt | Korea Zinc, LS MnM | Stabilizing price indicators and ternary battery demand recovery | Continued weak demand in ternary battery lines |

| Ganfeng Lithium Group | POSCO Holdings | Continued upstream resource expansion, cost advantage, low capex | Protectionism in major markets |

| Tianqi Lithium | POSCO Holdings | Increasing lithium concentrate and compound output, continued resource access through partnerships | Protectionism in major markets |

| Londian Wason | SK Nexilis | Top-tier utilization gap versus industry utilization, customer portfolio including Samsung, SK, and LG as well as Chinese customers | Weak results expected through the first half and protectionism |

4. Investment strategy

- Build a portfolio around leading players as China's battery market recovers.

- For ESS acceleration, focus on Tesla Megapack-related names such as EVE Energy and CATL.

- For robot and drone battery expansion, watch humanoid and eVTOL-related opportunities.

- For battery-metal bottoming, review entry timing in lithium, nickel, and cobalt-related companies.

The secondary-battery market appears to be entering an oversupply-easing phase, with restructuring centered on leading players. In that process, investing around likely share gainers such as CATL, EVE Energy, and Yunnan Energy New Material looks more favorable to me.

Sources

- Original Naver Blog post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=223788394220

- Mirae Asset China secondary-battery visit report: https://securities.miraeasset.com/bbs/download/2134901.pdf?attachmentId=2134901