DEEP RESEARCH · GEOSOFT/OASIS MARKET

[Geosoft] Analysis of Oasis Market's Conditional TMON Acquisition

A review of the stalking-horse structure, TMON's value and creditor burden, and Oasis Market's synergy and additional investment needs

0. Bottom line first

Oasis Market's potential TMON acquisition could quickly expand its member base and transaction volume, but restoring trust after TMON's settlement crisis and competing with Coupang and Naver would likely require substantial additional investment. The key issues are the acquisition terms and whether funding through an IPO is possible.

Interpretation: Oasis Market needed a clear new growth driver because its recent sales growth had slowed, and it had been reviewing M&A for some time. Still, whether it can survive after heavy post-acquisition investment remains a separate question.

1. Merger terms and pricing frame

Official fact: According to the source, Oasis Market adopted a stalking-horse strategy for the TMON acquisition. In this structure, a conditional buyer is selected first, then an open competitive bidding process follows. If another company offers better terms, Oasis Market can still acquire TMON by matching those terms.

| Item | Source figure/detail | Meaning |

|---|---|---|

| Proposed acquisition price | Not disclosed due to NDA; industry estimate around KRW 20bn | Exact terms are the key issue |

| TMON liquidation value | KRW 13.6bn | One reference point for creditor consent |

| TMON going-concern value | KRW -92.9bn | Continuing-business value was assessed as negative |

| TMON assets | KRW 70.3bn | Small relative to rehabilitation claims |

| Rehabilitation claims | KRW 1.0091tn | Creditor persuasion and rehabilitation planning are difficult |

| Wemakeprice | EY Hanyoung plans to continue a separate sale | Separate sale variable remains |

Related article: Oasis gets chance to acquire TMON cheaply - DealSite

2. Oasis Market versus TMON

Oasis Market specializes in fresh-food early-morning delivery and combines offline stores with an online platform. TMON is an open-market platform selling a broad range of products. Oasis Market has operated profitably for 12 consecutive years, while TMON suffered a large settlement failure and lost trust.

Profit and fresh food

Fresh-food early-morning delivery, offline-store integration, and a 2 million member base are its strengths.

Scale and brand

TMON has strong brand awareness, 4-5 million active members, and categories including manufactured goods, travel, and cultural products.

Trust recovery

TMON must repair damaged trust after the settlement crisis and address weak profitability.

Platform assets

TMON has platform assets such as the AI-based advertising solution SmartAI.

| Strengths | Weaknesses |

|---|---|

| High brand awareness | Lower trust after settlement failure |

| 4-5 million active members | Weak profitability |

| AI-based ad solution | Seller attrition risk |

3. Customer base and GMV synergy

Official fact: The source gives Oasis Market membership of 2 million and TMON active members of 4-5 million. Combined, the member base could reach about 7 million, comparable to Gmarket and 11st.

Oasis focuses on fresh food, while TMON sells a broader range including manufactured goods, travel, and cultural products. After a merger, Oasis could use TMON's platform and seller network to expand toward a broader e-commerce platform.

| Item | Source figure | Comparison |

|---|---|---|

| TMON 2022 transaction volume | KRW 3.8tn | 11.7x Oasis Market online revenue of KRW 323.3bn |

| Expected Oasis Market valuation | KRW 1.5tn range if pursuing IPO next year | Core variable for acquisition funding and valuation |

| TMON past valuation | KRW 2tn | Expectations have fallen sharply during rehabilitation |

| Oasis Market current-year outlook | Revenue KRW 350bn and operating margin 48.1% | Preserved from source; definition and sustainability need verification |

4. Expected synergy and execution tasks

- Economies of scale: TMON could expand online transaction volume and help reduce unit costs through bulk purchasing, logistics efficiency, and lower marketing cost per customer.

- Product diversification: Oasis can expand beyond fresh food using TMON's platform and seller network.

- Brand awareness: The acquisition could raise Oasis Market's recognition and strengthen its e-commerce position.

- Online-offline linkage: Oasis could sell TMON products in offline stores or allow pickup of TMON orders at offline locations.

- IPO retry: The enlarged scale could support a renewed IPO attempt.

The execution tasks are clear. Oasis must apply its early-morning delivery system to TMON, integrate logistics, expand delivery regions, and manage delivery quality. It also needs to repair TMON's damaged image and compete against dominant platforms such as Coupang and Naver.

5. Additional investment and financial view

After the merger, additional investment may be needed in business expansion, technology development, and marketing. Restoring trust in TMON and strengthening platform competitiveness seem likely to require substantial spending. Possible funding sources include IPO proceeds, additional investment, and internal funds.

- Business expansion: Broaden categories through TMON and invest in logistics infrastructure to expand early-morning delivery.

- Technology development: Upgrade TMON's platform and develop AI and big-data services.

- Marketing: Improve TMON's brand image and expand the customer base.

- Risks: Weak synergy, intensifying competition, and management failure are the key investment risks.

6. Overall view

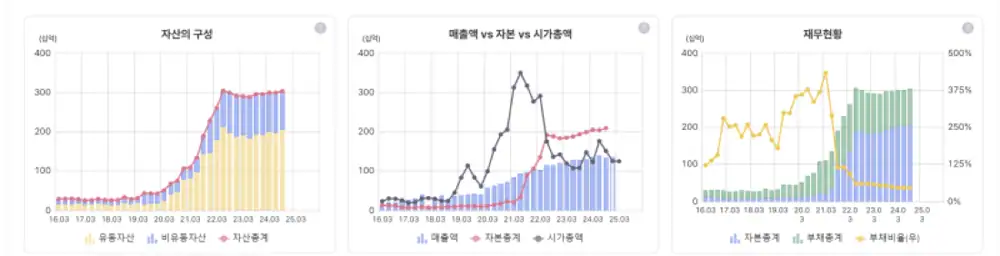

According to the source, Geosoft has current assets, especially cash-like assets, around KRW 200bn and a debt ratio in the 40% range. If the merger happens, I think the likely picture is funding the TMON acquisition through an Oasis Market IPO.

Oasis Market currently operates early-morning delivery in some regions, and its track record in fresh food deserves recognition. But additional investment after acquiring TMON would be substantial, and whether it can survive against Coupang and Naver remains an open question. Next, I need to research the manager in more detail.

Sources

- Original Naver Blog post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=223787299096

- Oasis and TMON acquisition related blog: https://m.blog.naver.com/healtouch/223787882847

- DealSite article: https://dealsite.co.kr/articles/137688