DEEP RESEARCH · UTI

[UTI] Cash Analysis

A review of cash flow, financing, and debt risk before UTG revenue becomes visible after Corning's equity investment

0. Bottom line first

UTI's key investment point is Corning's equity investment and the UTG business. But until UTG results appear, cash flow looks risky. The existing business does not seem to be generating enough cash while the company is betting heavily on a new business, so I think only a very small monitoring position is appropriate for now.

Interpretation: In this kind of period, I would trust the share-price trend more than management's words. Corning, the private-placement investors, and CB investors provide some basis for confidence, but I still do not think the position deserves a large weight yet.

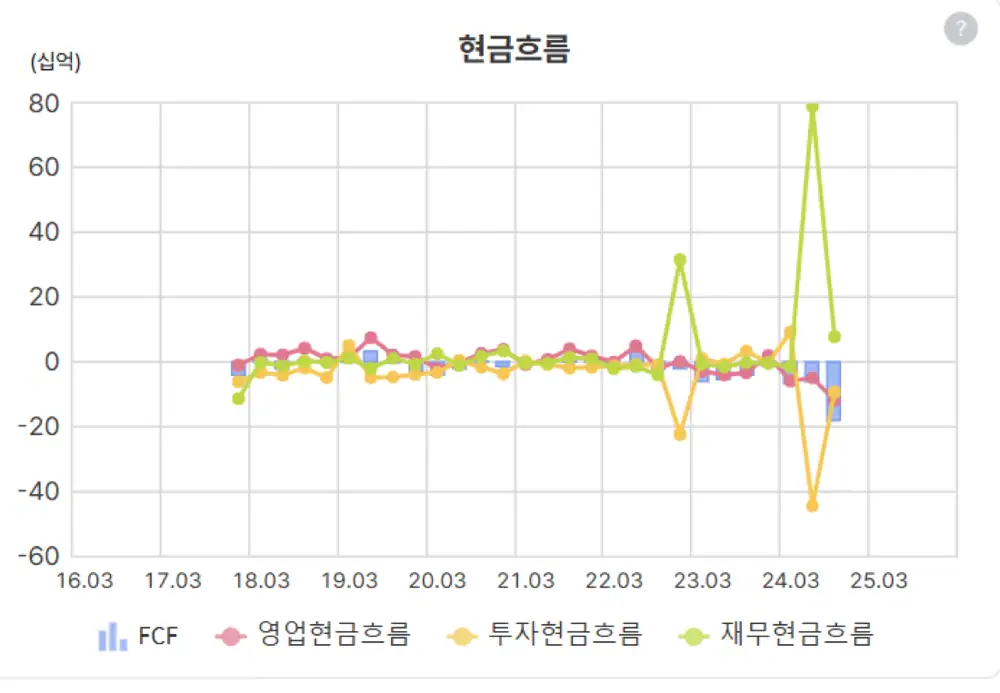

In 2024, UTI raised a large amount of cash through equity issuance and bonds, then quickly invested in the Vietnam plant. Since then, FCF has continued to flow out and operating cash flow has not looked good. Before the 2024 funding is consumed, UTG-based deliveries and revenue need to start.

1. Financing timeline

Official fact: According to the source, 2020-2021 saw management stock-option exercises but no large external financing. Major financing began after 2022.

| Timing | Financing method | Size/terms | Meaning |

|---|---|---|---|

| October 2022 | Third-party placement to Corning, convertible preferred shares | About KRW 35.9bn, 1:1 conversion right, issue price KRW 21,450, conversion claim period from 2024-10-15 to 2028-10-15 | Strategic collaboration with Corning |

| May 2024 | Convertible preferred shares and first CB | Preferred shares about KRW 25.8bn and CB KRW 54.15bn, total about KRW 80bn. Preferred shares 707,052 shares at KRW 36,559. Five-year CB maturing in June 2029 with 0% coupon and 0% maturity interest | Funding for the Vietnam plant and operating needs |

| June 26, 2024 | Additional preferred shares and second CB | Preferred shares KRW 2.7bn, 88,078 shares at KRW 30,654. CB KRW 6.3bn, conversion price KRW 30,654, expected conversion shares 205,519 | Additional facility and working-capital funding |

| Total | CPS and CB | KRW 35.9bn in 2022 + KRW 80bn in 2024 + KRW 9bn in 2024 = about KRW 124.9bn | Capital that buys time for the new business |

2. Use of funds and cash level

Official fact: The 2022 KRW 35.9bn Corning investment was used for facility investment and operating funds for foldable-phone ultra-thin glass. For the 2024 KRW 80bn raise, about KRW 38bn was planned for the Vietnam new plant and other facilities, and about KRW 16.15bn for R&D and operating funds. Of the KRW 25.8bn preferred-share proceeds, about KRW 17bn was allocated to production equipment and about KRW 8.8bn to operating funds. The additional KRW 9bn raised in June 2024 was also split into items including KRW 4bn for facilities and KRW 2.3bn for operating funds.

Cash and cash equivalents increased from about KRW 10.6bn at end-2023 to about KRW 27.6bn at the end of 3Q 2024. Still, much of the raised capital is being put into plant construction and related investment, so remaining pure cash may be smaller than the headline financing amount.

3. Interest expense and operating burden

Official fact: The first and second CBs issued in 2024, totaling KRW 60.45bn, are zero-coupon bonds with 0% coupon and 0% maturity interest. Direct coupon burden from these CBs is limited.

Past interest expense rose to about KRW 3.5bn in 2022, more than quadrupling year on year, then fell to about KRW 0.7bn in 2023 after some debt repayment. In 2024, financial-cost pressure may remain limited because some short-term debt was repaid and the new CBs are zero-coupon. But with operating profit in the red, even modest interest expense remains a burden when viewed through the interest-coverage ratio.

4. Future cash flow and debt-repayment scenario

Interpretation: UTI is aiming for a turnaround in foldable-phone UTG through the Corning partnership and Vietnam plant investment. Some securities-market commentary mentioned the possibility of more than KRW 20bn in 2024 operating profit or explosive growth with foldable product launches, but the real test is whether that converts into operating cash flow.

If cash flow improves, debt repayment becomes the top priority. The KRW 54.15bn CB maturing in 2029 is especially important. If the stock price rises sufficiently above the first CB conversion price of KRW 36,559 and the second CB conversion price of KRW 30,654, investors may convert to shares, turning debt into equity and improving the balance sheet. If business performance and the share price remain weak, UTI must separately secure repayment funds at maturity.

5. Financial soundness and liquidity risk

| Item | Source figure | Interpretation |

|---|---|---|

| Equity | KRW 60.7bn at end-2021 → KRW 47.3bn in 2022 → KRW 17.2bn in 2023 | Equity has shrunk quickly due to weak results |

| Debt ratio | 485.68% in 2023 | Far above the 200% level often treated as risky |

| Simple 2024 debt-ratio estimate | KRW 25.8bn preferred shares partly reflected as equity, while KRW 54.2bn CB is recognized as debt, implying a possible 800% level | Leverage remains burdensome if CBs do not convert |

| Partial capital impairment risk | At end-2024, equity may fall below stated capital of about KRW 8bn; consensus-based equity around KRW 5bn and impairment ratio of 37.5% were noted | Further losses could raise full capital-impairment concerns |

| Current ratio | About 79% at end-3Q 2024 | Current liabilities exceed current assets |

Ultimately, the UTI investment depends on whether UTG revenue appears while the newly raised capital buys time. I need to check in the detailed annual report whether the large operating loss is due to temporary investment or inventory growth.

If the loss is temporary because of investment or inventory buildup, I may increase the position. Otherwise, I would rather wait for additional equity financing or bank loans before putting more weight on it.

6. Foldable glass references

The original post also attached related posts on Apple's expected 2026 foldable-phone mass production, Korean component suppliers, and Korean versus Chinese UTG and hinge technology.

Sources

- Original Naver Blog post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=223779498265

- Numbers KRW 2.7bn private placement: https://www.numbers.co.kr/news/articleView.html?idxno=5294

- DealSite KRW 35.9bn private placement: https://dealsite.co.kr/articles/92682/103125

- Daily Invest UTG revenue outlook: http://www.dailyinvest.kr/news/articleView.html?idxno=48315

- IB Tomato KRW 80bn financing and financial risk: https://www.ibtomato.com/Mobile/mView.aspx?no=12233&type=1

- Edaily KRW 6.3bn convertible bond: https://m.edaily.co.kr/News/Read?newsId=02614166638925656&mediaCodeNo=257

- FnGuide UTI financial statements: https://comp.fnguide.com/SVO2/asp/SVD_Finance.asp?pGB=1&gicode=A179900&cID=&MenuYn=Y&ReportGB=&NewMenuID=103&stkGb=701

- WiseReport UTI company monitor: https://comp.wisereport.co.kr/company/c1010001.aspx?cn=&cmp_cd=179900

- Foldable glass related post 1: https://m.blog.naver.com/star_of_self/223753928410

- Foldable glass related post 2: https://m.blog.naver.com/star_of_self/223754164000

- Original detailed link 1: https://www.numbers.co.kr/news/articleView.html?idxno=5294#:~:text=%EC%9C%A0%ED%8B%B0%EC%95%84%EC%9D%B4%EB%8A%94%20%EC%8B%9C%EC%84%A4%EC%9E%90%EA%B8%88%2029%EC%96%B5%EC%9B%90%20%EB%B0%8F%20%EC%9A%B4%EC%98%81%EC%9E%90%EA%B8%88,8%EB%A7%8C8078%EC%A3%BC%EB%A5%BC%20%EB%B0%9C%ED%96%89%ED%95%98%EB%8A%94%20%EC%A0%9C3%EC%9E%90%EB%B0%B0%EC%A0%95%EC%A6%9D%EC%9E%90%EB%A5%BC%20%EA%B2%B0%EC%A0%95%ED%96%88%EB%8B%A4%EA%B3%A0

- Original detailed link 2: https://dealsite.co.kr/articles/92682/103125#:~:text=%EC%9C%A0%ED%8B%B0%EC%95%84%EC%9D%B4%EB%8A%94%20%EC%8B%9C%EC%84%A4%EC%9E%90%EA%B8%88%EA%B3%BC%20%EC%9A%B4%EC%98%81%EC%9E%90%EA%B8%88%20%EB%A7%88%EB%A0%A8%EC%9D%84%20%EC%9C%84%ED%95%B4,Corning%20Hungary%20Data%20Services%20LLC%27%EB%8B%A4

- Original detailed link 3: http://www.dailyinvest.kr/news/articleView.html?idxno=48315#:~:text=%EA%B8%80%EB%A1%9C%EB%B2%8C%20%EB%94%94%EC%8A%A4%ED%94%8C%EB%A0%88%EC%9D%B4%20%EA%B8%80%EB%9D%BC%EC%8A%A4%20%EC%8B%9C%EC%9E%A5%EC%A0%90%EC%9C%A0%EC%9C%A8%201%EC%9C%84,%EA%B9%8C%EC%A7%80%20%EB%81%8C%EC%96%B4%EC%98%AC%EB%A0%B8%EB%8B%A4%E2%80%9D%EA%B3%A0%20%EB%B6%84%EC%84%9D%ED%96%88%EB%8B%A4

- Original detailed link 4: https://www.ibtomato.com/Mobile/mView.aspx?no=12233&type=1#:~:text=%EC%9C%A0%EC%83%81%EC%A6%9D%EC%9E%90%C2%B7%EC%A0%84%ED%99%98%EC%82%AC%EC%B1%84%EB%A1%9C%20800%EC%96%B5%EC%9B%90%20%EC%A1%B0%EB%8B%AC%ED%95%B4%20%EC%8B%9C%EC%84%A4%C2%B7%EC%9A%B4%EC%98%81%20%EC%9E%90%EA%B8%88,%EB%AA%A8%EC%A7%91

- Original detailed link 5: https://www.ibtomato.com/Mobile/mView.aspx?no=12233&type=1#:~:text=22%EC%9D%BC%20%EA%B8%88%EC%9C%B5%EA%B0%90%EB%8F%85%EC%9B%90%20%EA%B3%B5%EC%8B%9C%EC%8B%9C%EC%8A%A4%ED%85%9C%EC%97%90%20%EB%94%B0%EB%A5%B4%EB%A9%B4%20%EC%9C%A0%ED%8B%B0%EC%95%84%EC%9D%B4%EB%8A%94,%EB%8B%AC%ED%95%98%EB%A9%B0%20%EC%A0%84%ED%99%98%EA%B0%80%EC%95%A1%EC%9D%80%20%EC%A3%BC%EB%8B%B9%203%EB%A7%8C6559%EC%9B%90%EC%9C%BC%EB%A1%9C%20%EC%A0%95%ED%95%B4%EC%A1%8C%EB%8B%A4

- Original detailed link 6: https://www.ibtomato.com/Mobile/mView.aspx?no=12233&type=1#:~:text=3%EB%A7%8C6559%EC%9B%90%EC%9C%BC%EB%A1%9C%20%EC%A0%95%ED%95%B4%EC%A1%8C%EB%8B%A4

- Original detailed link 7: https://m.edaily.co.kr/News/Read?newsId=02614166638925656&mediaCodeNo=257#:~:text=%EC%9C%A0%ED%8B%B0%EC%95%84%EC%9D%B4%2C%2063%EC%96%B5%EC%9B%90%20%EA%B7%9C%EB%AA%A8%20%EC%A0%84%ED%99%98%EC%82%AC%EC%B1%84%EA%B6%8C%20%EB%B0%9C%ED%96%89,%EC%A0%84%ED%99%98%EC%B2%AD%EA%B5%AC%EA%B8%B0%EA%B0%84%EC%9D%80%202025%EB%85%84%206%EC%9B%94%2028%EC%9D%BC%EB%B6%80%ED%84%B0

- Original detailed link 8: https://www.numbers.co.kr/news/articleView.html?idxno=5294#:~:text=%EC%9C%A0%ED%8B%B0%EC%95%84%EC%9D%B4%EB%8A%94%20%EC%9C%A0%EC%83%81%EC%A6%9D%EC%9E%90%20%EC%86%8C%EC%8B%9D%EA%B3%BC%20%ED%95%A8%EA%BB%98%2063%EC%96%B5%EC%9B%90,%EB%94%B0%EB%9D%BC%20%EB%B0%9C%ED%96%89%ED%95%A0%20%EC%A3%BC%EC%8B%9D%20%EC%88%98%EB%8A%94%2020%EB%A7%8C5519%EC%A3%BC%EB%8B%A4

- Original detailed link 9: https://www.numbers.co.kr/news/articleView.html?idxno=5294#:~:text=Image

- Original detailed link 10: https://comp.fnguide.com/SVO2/asp/SVD_Finance.asp?pGB=1&gicode=A179900&cID=&MenuYn=Y&ReportGB=&NewMenuID=103&stkGb=701#:~:text=%EB%B0%B0%EC%B6%9C%EA%B6%8C%20%EA%B8%B0%ED%83%80%EC%9C%A0%EB%8F%99%EC%9E%90%EC%82%B0%2036%2042%2047,173%20188%20106%20276%20%EB%A7%A4%EA%B0%81%EC%98%88%EC%A0%95%EB%B9%84%EC%9C%A0%EB%8F%99%EC%9E%90%EC%82%B0%EB%B0%8F%EC%B2%98%EB%B6%84%EC%9E%90%EC%82%B0%EC%A7%91%EB%8B%A8

- Original detailed link 11: https://comp.fnguide.com/SVO2/asp/SVD_Finance.asp?pGB=1&gicode=A179900&cID=&MenuYn=Y&ReportGB=&NewMenuID=103&stkGb=701#:~:text=%EC%9D%B4%EC%9E%90%EB%B9%84%EC%9A%A9%205%207%2016%2035,%EA%B3%B5%EC%A0%95%EA%B0%80%EC%B9%98%EC%B8%A1%EC%A0%95%C2%A0%EA%B8%88%EC%9C%B5%EC%9E%90%EC%82%B0%EA%B4%80%EB%A0%A8%EC%86%90%EC%8B%A4

- Original detailed link 12: http://www.dailyinvest.kr/news/articleView.html?idxno=48315#:~:text=%EC%B5%9C%20%EC%97%B0%EA%B5%AC%EC%9B%90%EC%9D%80%20%EB%82%B4%EB%85%84%EB%B6%80%ED%84%B0%20%EB%B3%B8%EA%B2%A9%EC%A0%81%EC%9D%B8%20%ED%88%AC%EC%9E%90,%EC%83%81%ED%96%A5%EB%90%A0%20%EC%88%98%20%EC%9E%88%EB%8B%A4%EB%8A%94%20%EC%9D%98%EB%AF%B8%E2%80%9D%EB%9D%BC%EA%B3%A0%20%EC%84%A4%EB%AA%85%ED%96%88%EB%8B%A4

- Original detailed link 13: http://www.dailyinvest.kr/news/articleView.html?idxno=48315#:~:text=%EC%B5%9C%20%EC%97%B0%EA%B5%AC%EC%9B%90%EC%9D%80%20%E2%80%9C2%EB%85%84%20%EC%9D%B4%EC%83%81%EC%97%90%20%EA%B1%B8%EC%B3%90,%EB%B0%B8%EB%A5%98%EC%97%90%EC%9D%B4%EC%85%98%20%ED%99%95%EC%9E%A5%20%EA%B5%AC%EA%B0%84%EC%97%90%20%EB%8F%8C%EC%9E%85%ED%96%88%EB%8B%A4%E2%80%9D%EA%B3%A0%20%EB%B6%84%EC%84%9D%ED%96%88%EB%8B%A4

- Original detailed link 14: https://www.ibtomato.com/Mobile/mView.aspx?no=12233&type=1#:~:text=,%EC%A7%93%EA%B3%A0%20%EC%9E%AC%EB%8F%84%EC%95%BD%EC%9D%98%20%EA%B8%B0%ED%9A%8C%EB%A1%9C%20%EC%82%BC%EC%9D%84%20%EB%B0%A9%EC%B9%A8%EC%9D%B4%EB%8B%A4

- Original detailed link 15: https://www.ibtomato.com/Mobile/mView.aspx?no=12233&type=1#:~:text=%EB%B0%98%EB%A9%B4%20%EC%9E%90%EB%B3%B8%EC%B4%9D%EA%B3%84%EB%8A%94%202021%EB%85%84%20607%EC%96%B5%EC%9B%90%2C%202022%EB%85%84,%EA%B9%8C%EC%A7%80%20%EC%BB%A4%EC%A1%8C%EB%8B%A4

- Original detailed link 16: https://www.ibtomato.com/Mobile/mView.aspx?no=12233&type=1#:~:text=%EC%97%AC%EA%B8%B0%EC%97%90%201%ED%9A%8C%EC%B0%A8%20CB%20%EA%B8%88%EC%95%A1%EC%9D%B8%20541%EC%96%B55000%EB%A7%8C%EC%9B%90%EC%9D%84,%EC%9D%B4%EC%97%90%20%EB%94%B0%EB%A5%B8

- Original detailed link 17: https://www.ibtomato.com/Mobile/mView.aspx?no=12233&type=1#:~:text=match%20at%20L82%20%EB%B6%80%EC%B1%84%EB%B9%84%EC%9C%A8%EC%9D%80%20800,%EC%9C%84%ED%97%98%20%EC%88%98%EC%A4%80%EC%9D%84%20%ED%9B%8C%EC%A9%8D%20%EB%84%98%EC%96%B4%EC%84%A0%20%EA%B2%83%EC%9D%B4%EB%8B%A4

- Original detailed link 18: https://www.ibtomato.com/Mobile/mView.aspx?no=12233&type=1#:~:text=%EB%B6%80%EC%B1%84%EB%B9%84%EC%9C%A8%EC%9D%80%20800,%EC%9C%84%ED%97%98%20%EC%88%98%EC%A4%80%EC%9D%84%20%ED%9B%8C%EC%A9%8D%20%EB%84%98%EC%96%B4%EC%84%A0%20%EA%B2%83%EC%9D%B4%EB%8B%A4

- Original detailed link 19: https://comp.fnguide.com/SVO2/asp/SVD_Finance.asp?pGB=1&gicode=A179900&cID=&MenuYn=Y&ReportGB=&NewMenuID=103&stkGb=701#:~:text=422%20622%20455%201%2C111%20%EC%9E%AC%EA%B3%A0%EC%9E%90%EC%82%B0,%ED%99%98%EB%B6%88%29%EC%9E%90%EC%82%B0%20%EB%B0%B0%EC%B6%9C%EA%B6%8C

- Original detailed link 20: https://comp.fnguide.com/SVO2/asp/SVD_Finance.asp?pGB=1&gicode=A179900&cID=&MenuYn=Y&ReportGB=&NewMenuID=103&stkGb=701#:~:text=%EC%9C%A0%EB%8F%99%EB%B6%80%EC%B1%84%EA%B3%84%EC%82%B0%EC%97%90%20%EC%B0%B8%EC%97%AC%ED%95%9C%20%EA%B3%84%EC%A0%95%20%ED%8E%BC%EC%B9%98%EA%B8%B0

- Original detailed link 21: https://comp.wisereport.co.kr/company/c1010001.aspx?cn=&cmp_cd=179900#:~:text=%EC%9C%A0%ED%8B%B0%EC%95%84%EC%9D%B4%20,%EC%9D%B8%EC%8B%9D%EB%90%9C%20%EC%9E%AC%EA%B3%A0%EC%9E%90%EC%82%B0%20%EA%B8%88%EC%95%A1%EC%9D%B4%20%EC%A6%9D%EA%B0%80

- Original detailed link 22: https://www.ibtomato.com/Mobile/mView.aspx?no=12233&type=1#:~:text=%EC%8B%A4%EC%A0%81%20%EB%B6%80%EC%A7%84%EC%97%90%20%EC%9E%90%EB%B3%B8%EC%9E%A0%EC%8B%9D%20%EC%9C%84%EA%B8%B0%C2%B7%EB%B6%80%EC%B1%84%EB%B9%84%EC%9C%A8%20%EA%B4%80%EB%A6%AC,%EC%9A%94%EB%A7%9D

- Original detailed link 23: https://www.ibtomato.com/Mobile/mView.aspx?no=12233&type=1#:~:text=%EC%9C%A0%ED%8B%B0%EC%95%84%EC%9D%B4%EB%8A%94%20%EC%A7%80%EB%82%9C%203%EB%85%84%EA%B0%84%20%EB%A7%A4%EC%B6%9C%EA%B3%BC%20%EC%88%98%EC%9D%B5%EC%84%B1,%EC%A0%9C%EA%B3%A0%EB%8A%94%20%ED%92%80%EC%96%B4%EC%95%BC%20%ED%95%A0%20%EA%B3%BC%EC%A0%9C%EB%A1%9C%20%EA%BC%BD%ED%9E%8C%EB%8B%A4