DEEP RESEARCH · LG Display / 8.6G Investment

LG Display's 8.6G OLED Investment — A Readiness Check via the Articles of Incorporation

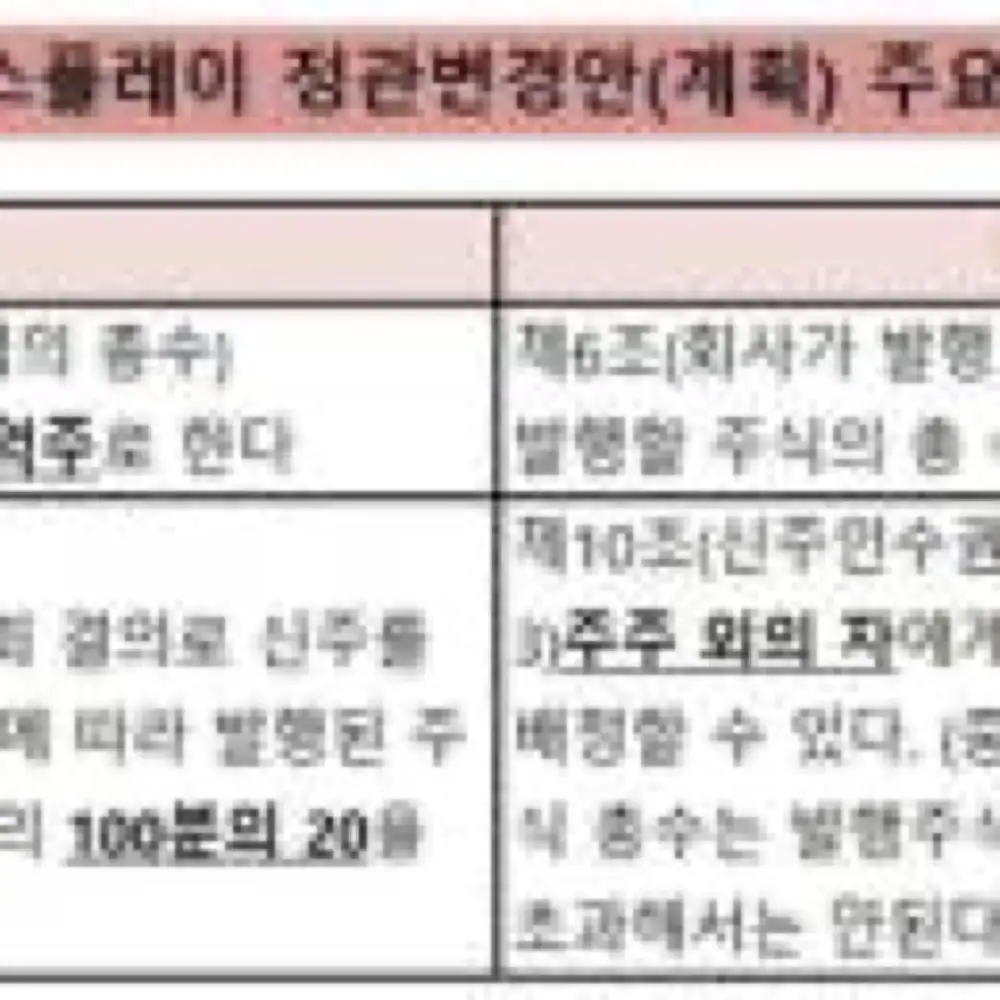

Authorized shares doubled (500m → 1bn), third-party allotment ceiling raised — the procedural runway before a real decision

0. Bottom line first

At the FY25 AGM (40th term), LG Display tabled motions to raise authorized shares from 500m to 1bn, and to lift the third-party allotment cap from 20% to 30%. This is best read not as a green light on 8.6G capex, but as finishing the procedural runway so that once the decision is made, capital raising can move quickly.

Interpretation: CEO Cheong Cheol-dong has declared a "J.U.M.P" strategy for 2025, but on the 8.6G timing he is sticking to "decide after watching the market." The Guangzhou LCD divestiture (~KRW 2 trn) is the core of the balance-sheet repair. Meanwhile KIPOST notes that targeting Apple's MacBook Air would force a decision by H1 this year.

1. Articles of Incorporation — the last 10 years

LG Display amends its charter only when needed. The standout change of the last decade sits in the capital clauses. A KRW 1.3 trn rights offering in late 2022 used up the existing 500m authorized-share ceiling, so the company tabled a motion at the FY25 AGM (40th term) to double authorized shares from 500m to 1bn.

Official fact: Companies routinely amend the charter ahead of new share issuance to leave runway for the authorized-share cap. LG Display has followed that pattern; past amendments have all passed by the special-resolution threshold.

Interpretation: So the amendment pattern has two axes — regulatory compliance (electronic securities, commercial code changes) and financial strategy (capital raising for investment). This year's amendment is clearly the second.

500m → 1bn

The 2022 KRW 1.3 trn rights offering exhausted the prior ceiling; the doubling preserves future funding capacity.

20% → 30%

Preparation for strategic investor entries or large capital raises; the cap calculation is also reset.

Guangzhou LCD ~KRW 2 trn

Shift focus to high-value OLED and repair the balance sheet.

2. 8.6G investment — official statements and strategy

Samsung Display announced a ~KRW 4.1 trn 8.6G IT-OLED investment in 2023, with mass production targeted for 2026 (equipment move-in begun). China's BOE has declared a roughly KRW 11.5 trn investment. LG Display, by contrast, has stayed conservative — "demand uncertainty remains and balance-sheet strength is the priority."

Official fact: LG Display kept 2023–2024 CAPEX in the low KRW 2 trn range and did not rush into 8G OLED capacity additions. CEO Cheong declared the "J.U.M.P" strategy for 2025 but, on 8.6G timing, says the decision will follow "what the market looks like."

Interpretation: Street estimates put the 8.6G investment at at least KRW 3 trn. The consensus is "no 8.6G commitment this year; next year at earliest, conditional on demand recovery and funding." But as KIPOST flagged, chasing Apple MacBook Air OLED would force a commitment by H1 this year.

3. What in the charter would block 8.6G? Nothing material.

- Business purpose: The charter already lists "manufacture and sale of TFT-LCD and OLED panels", so 8.6G OLED production is within scope. No purpose-clause amendment needed.

- Capital clauses: The FY25 AGM doubled authorized shares and lifted the 3rd-party allotment cap to 30% — board flexibility on new-share issuance and funding has expanded materially.

- Residual risk: If investment scope expands further (e.g. allotments above 30%, novel securities), additional amendments at an EGM are possible.

In short, the legal/charter runway for 8.6G is essentially complete. The remaining variables are the timing of the cycle recovery and the specific mix of funding (divestitures, equity issuance, debt).

4. Key insights

- Through the "charter-history" lens, LGD amends the articles at the intersection of regulatory changes and financial strategy.

- This amendment is a signal of capital-raising readiness for 8.6G.

- Once execution begins, capital raising and project mobilization can move quickly; further amendments, if any, would be tweaks for partnership structure or shareholder-rights protection rather than blockers.

Sources

- Original Naver Blog post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=223778717365

- Yonhap Infomax — "Why LG Display is doubling authorized shares from 500m to 1bn": https://news.einfomax.co.kr/news/articleView.html?idxno=4343968

- LG Display AGM resolutions and charter amendment disclosures, official press and IR materials.