DEEP RESEARCH · PHILOPTICS/GLASS SUBSTRATES

[Philoptics] SKC Report Notes

A Philoptics-relevant update from a Meritz Securities SKC report, focused on glass-substrate momentum

0. Bottom line first

The SKC report frames 2025 as a year of gradual turnaround: growth is expected to come from semiconductors and glass substrates, while profitability depends on copper-foil utilization recovering. The author saved it as a glass-substrate update.

1. 4Q24P results: why losses widened

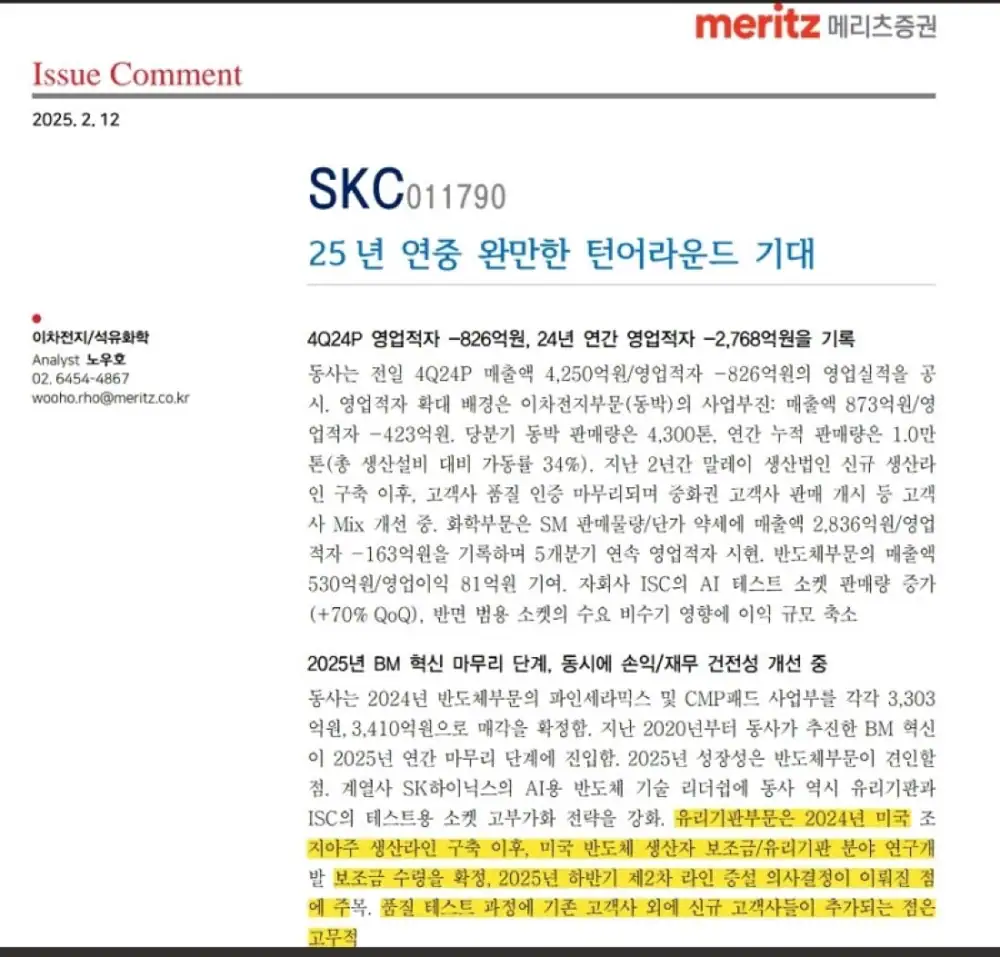

Official fact: The February 12, 2025 Meritz Securities report by Noh Woo-ho states that SKC posted 4Q24P revenue of KRW 425.0bn and an operating loss of KRW -82.6bn, with a full-year 2024 operating loss of KRW -276.8bn. The report URL is Meritz Securities SKC report PDF.

| Segment | 4Q24P key figure | Read-through |

|---|---|---|

| Battery materials/copper foil | Revenue KRW 87.3bn, operating loss KRW -42.3bn | Main reason operating losses widened |

| Chemicals | Revenue KRW 283.6bn, operating loss KRW -16.3bn | Weak SM volume/pricing; fifth straight quarterly loss |

| Semiconductors | Revenue KRW 53.0bn, operating profit KRW 8.1bn | ISC AI test-socket volume +70% QoQ, partly offset by general-purpose socket seasonality |

2. BM innovation and the semiconductor growth axis

Official fact: In 2024, SKC confirmed sales of its fine ceramics and CMP pad businesses in the semiconductor segment for KRW 330.3bn and KRW 341.0bn, respectively. The report says the BM innovation pursued since 2020 is entering its final stage in 2025.

Interpretation: The report’s growth case is centered on semiconductors, tied to SK Hynix’s AI semiconductor leadership and SKC’s higher-value strategy in glass substrates and ISC test sockets.

Non-core exit

Fine ceramics and CMP pads are being sold as BM innovation moves toward completion.

AI semiconductor link

Glass substrates and higher-value test sockets gain relevance alongside SK Hynix’s AI semiconductor leadership.

Liquidity

The report views cash liquidity as sound, helped by asset monetization and lower Capex from 2025.

3. Glass substrates: the update the author focused on

Official fact: After building a production line in Georgia, USA in 2024, the glass-substrate unit confirmed receipt of US semiconductor producer subsidies and glass-substrate R&D subsidies. The report highlights a possible second-line expansion decision in 2H25.

Interpretation: The addition of new customers, beyond existing ones, to the quality-test process is the key read-through that keeps the glass-substrate value chain interesting.

4. Copper-foil profitability: the condition for turnaround

Official fact: 4Q24 copper-foil sales volume was 4,300 tons, cumulative annual sales were 10,000 tons, and utilization was 34% of total capacity. Current capacity is 50,000 tons in Malaysia and 50,000 tons in Jeongeup, Korea.

- The Malaysia line is improving its customer mix as quality approvals are completed and sales to Chinese customers begin.

- The strategy is to gradually reduce the less cost-competitive Jeongeup footprint while maximizing customer sales from the lower-cost Malaysia line.

- The report expects utilization to rebound from the 4Q24 trough of 34% to above 70% by end-2025, with sales volume above 35,000 tons.

- The prior estimate is for the copper-foil segment to turn profitable in 3Q25E.

Sources

- Original Naver Blog post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=223757524737

- Meritz Securities SKC report PDF: https://home.imeritz.com/include/resource/research/WorkFlow/20250211173046807K_02.pdf