DEEP RESEARCH · ASSET ALLOCATION

[Asset Allocation] What High-Yield Spreads Say About Risk Appetite

A risk check combining tight high-yield spreads, Nasdaq volume, and Howard Marks' LME Wave

0. Bottom line first

A low high-yield spread suggests investors are insensitive to credit risk. Rather than leaving growth stocks entirely, I think this is a time to hedge with assets such as gold, U.S. Treasuries, and VIX, while watching whether market leaders print large bearish candles on heavy volume.

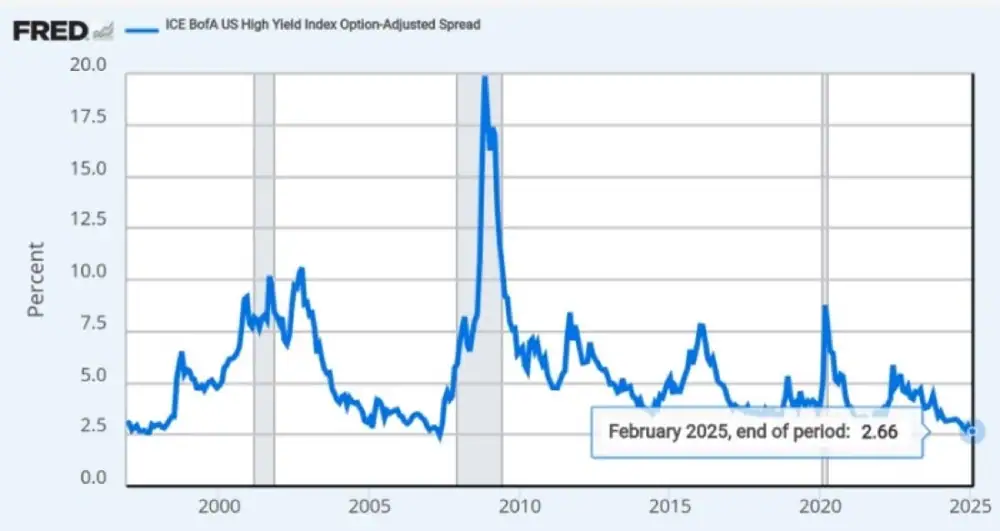

Official fact: The original post cites FRED's ICE BofA US High Yield Index Option-Adjusted Spread series: https://fred.stlouisfed.org/series/BAMLH0A0HYM2.

Interpretation: Tight spreads mean investors are receiving less compensation for credit risk. Asset allocation should account for the risk that Treasury yields fall or high-yield bond yields rise.

1. Current asset-allocation view

Tight high-yield spread

It may show that investors have become insensitive to credit risk.

Gold, Treasuries, VIX

These are typical diversification hedges, though timing and sizing require separate judgment.

Volume in leaders

Large bearish candles with heavy volume in leading stocks would be a warning sign.

I do not think investors need to exit U.S. equities too early. But allocation beyond U.S. stocks, including emerging-market equities and defensive assets, looks necessary. Because many growth companies may still emerge, the point is risk management rather than pure avoidance.

2. Warning signs in the Nasdaq chart

Interpretation: The Nasdaq chart looks like a broad transition toward weakness. Volume is heavier on declines from highs, lighter on rebounds, and the prior high has not been properly cleared. In that setup, even a breakout above the prior high should be questioned.

However, Chinese indices are moving in the opposite direction, so I would not call this a global risk event yet. The scariest shocks come when there is nowhere to hide, so regional asset flows also matter.

3. Reading Howard Marks' LME Wave

I referred to Howard Marks' latest memo, The LME Wave: The LME Wave.

Interpretation: In the original context, I read LME Wave as likely referring to debt-management strategies, such as convertible bonds or refinancing, that help companies avoid or delay default.

4. LME mechanics and risk

- Convertible bond issuance: It can reduce immediate repayment pressure and offer investors equity upside, but the debt remains if conversion does not happen.

- New bond issuance or maturity extension: This works better when rates are low or stable, but becomes harder when rates rise.

- Preparation for credit tightening: More LME activity can be read as companies rushing to restructure debt before liquidity shrinks.

In short, LME Wave may mean companies are postponing default, and it is a signal not to relax vigilance toward credit markets.

Sources

- Original post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=223754572126

- FRED High Yield Spread: https://fred.stlouisfed.org/series/BAMLH0A0HYM2

- Oaktree, The LME Wave: https://www.oaktreecapital.com/insights/insight-commentary/market-commentary/oaktree-credit-quarterly-4q2024-the-lme-wave