DEEP RESEARCH · PALANTIR

Palantir’s Nasdaq 100 Inclusion and the Essence of Investing

Thoughts on Palantir’s rapid rise after index-inclusion momentum and what it means to invest in an innovative company

0. Bottom line first

After inclusion in the S&P 500, Palantir also gained Nasdaq 100 inclusion momentum and rose quickly. It can look expensive on traditional valuation, but more precisely, the difficulty is that future earnings are hard to forecast, making it hard to judge whether it is cheap or expensive.

I started investing in the Nasdaq 100 inclusion theme this September after the S&P 500 inclusion, but it has risen too quickly in a short time. I want to find a timing to increase the position, but the stock is not giving me an opportunity. I may just increase my Korean company weight instead.

1. Rapid gains and the difficulty of increasing weight

Palantir is an impressive company, and it does seem to be at the center of innovation. But because the stock is rising so quickly, it is not giving investors an easy chance to increase exposure.

Interpretation: For a company rising this fast, the buying timing itself becomes difficult. That is why I also think about increasing exposure to Korean companies instead.

2. The essence of investing: sharing ideas and risk

If I met the CEO of this kind of company directly, and the company said the idea and business model were excellent but it needed money to realize them, would I invest? In fact, this might be the best kind of investment.

When a company with a strong idea and business model needs money to realize it, the investor provides capital and receives equity. I wonder if that is what capitalism is. Through equity, the investor shares the risk and also shares the reward.

Power of the business model

Investing in an innovative company means looking at the idea and execution potential, not only current earnings.

Money needed for growth

The company needs capital to realize the idea.

Sharing risk and reward

The investor shares risk and reward through ownership.

3. Limits of traditional valuation

Companies like this usually have low current profits, so they inevitably look expensive under traditional valuation. That creates the dilemma.

However, the more accurate expression may be that future earnings are hard to forecast, not simply that it is hard to decide whether the stock is cheap or expensive.

Interpretation: I think the core of growth-stock investing is not reaching a conclusion from one metric like current PER, but weighing the possibility of explosive future cash-flow growth together with the uncertainty around it.

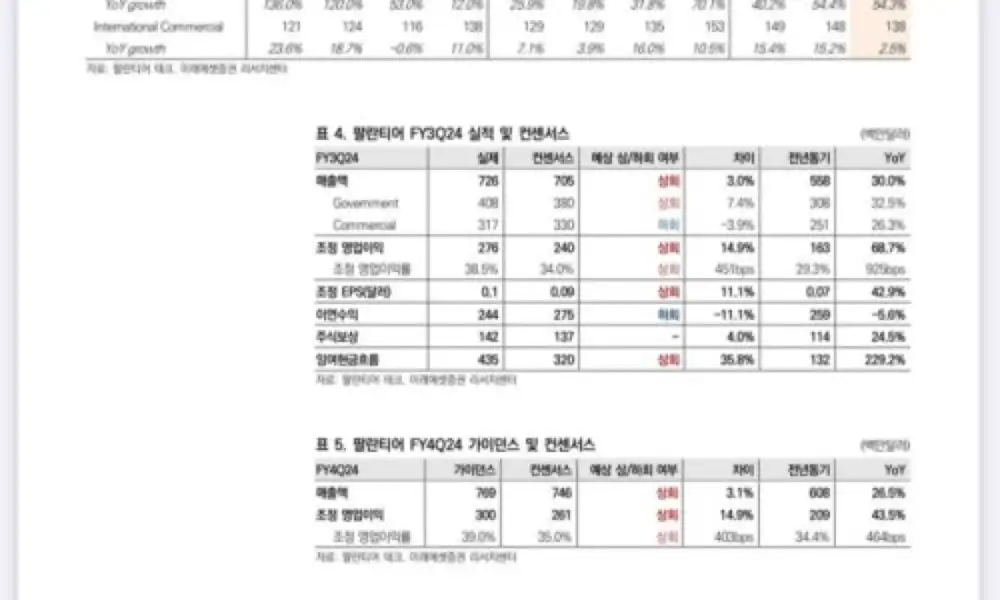

4. Previous Palantir posts

Below are previous posts I wrote about Palantir. All original links and preview images from the source are preserved.

[Palantir] A Candidate to Become a Leading Stock of This Era

[Palantir] FedRAMP High Authorization Obtained

[Palantir] 2024 Reagan National Defense Forum

Sources

- Original post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=223693164012

- Previous Palantir post: https://m.blog.naver.com/star_of_self/223624300892

- Palantir 3Q24 earnings: https://m.blog.naver.com/star_of_self/223648118386

- FedRAMP authorization post: https://m.blog.naver.com/star_of_self/223682729697

- Reagan National Defense Forum post: https://m.blog.naver.com/star_of_self/223688760141