DEEP RESEARCH · INBODY

InBody’s Stock Price and History: A Draft Review of Its Listed-Market Journey and Undervaluation Factors

A chart-based review of InBody’s key phases, growth expectations, and range-bound valuation factors

0. Bottom line first

InBody has grown for a long time on original products and global demand, but I think the central issues behind the current range-bound valuation are new growth drivers, ROE trends, and declining total asset turnover.

This post is a first draft summarizing InBody’s history and broad stock-price flow alongside charts. I plan to keep updating it as I gather more information.

1. Early listed period: 2000 to the early 2010s

Official fact: InBody listed on KOSDAQ in December 2000 with its original body composition analyzer product.

After listing, the stock gradually rose on stable revenue growth and technology. The 2004 low was KRW 717, after which the stock rose about 2,891%, recording a long-term upward trend.

In the early 2010s, global demand for body composition analyzers increased, and overseas subsidiaries in the United States, Japan, and other markets helped the stock continue rising.

2. 2012~2016: PAPS and wearable expectations

In 2012~2013, revenue surged and the stock rose as the company won government PAPS, or Physical Activity Promotion System, projects.

In 2015, InBody launched the wearable InBody Band and signed a large contract with Amway China. However, that revenue ended up being one-off.

| Period | Major event | Stock and valuation interpretation |

|---|---|---|

| 2012~2013 | PAPS project wins | Revenue surge and stock-price rise |

| 2015 | InBody Band launch and large Amway China contract | PER rose as high as 30x on new-product expectations |

| After 2Q 2016 | Earnings decline | Stock turned downward |

PER rose as high as 30x on expectations for the new product, but from 2Q 2016 earnings declined and the stock turned downward. Weakness in the wearable device then continued to push the stock toward its 2016 low.

3. 2016~2020: PER decline and the COVID-19 impact

During this period, operating profit was maintained, but new growth drivers were lacking. As a result, PER declined and the stock remained in a long-term range.

In 2020, COVID-19 caused a global economic slowdown, and revenue and operating profit fell. It was a rare period when the company’s upward earnings trend declined.

4. 2021~2023: Recovery and global expansion

In 2021, revenue increased along with post-pandemic healthcare industry growth, and the stock gradually recovered. Demand for professional InBody products in the U.S. market stood out in particular.

In 2023, revenue increased by about 6.5% year over year. However, the operating margin declined slightly due to higher costs. During this period, the stock has continued to move within a range.

Post-pandemic demand

Revenue recovered with growth in the healthcare industry.

Professional product demand

Demand for professional InBody products in the U.S. market stood out.

Revenue growth and costs

Revenue grew about 6.5%, but operating margin slipped slightly due to higher costs.

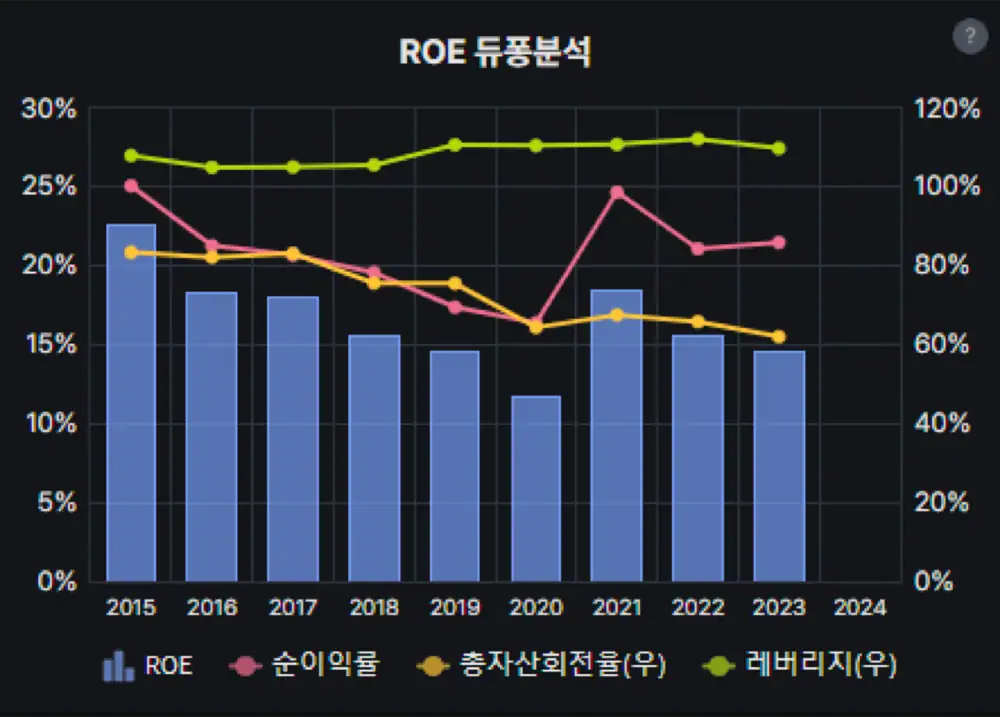

5. Core reasons for undervaluation and range-bound trading

I think the largest factor is that ROE appears to be trending downward due to lower total asset turnover. This trend may bottom and turn upward once new products begin contributing or SG&A expense growth slows to some degree.

Interpretation: The start of asset reduction through treasury-share cancellation is another point to watch. The company hired many employees this year, and I think the results may start appearing next year. I also want to keep expectations for the new product KOROT. I am rooting for the company.